- within Corporate/Commercial Law topic(s)

- with Finance and Tax Executives

- in United Kingdom

- in United Kingdom

- within Wealth Management, Employment and HR and Technology topic(s)

- with Senior Company Executives, HR and Finance and Tax Executives

- with readers working within the Law Firm industries

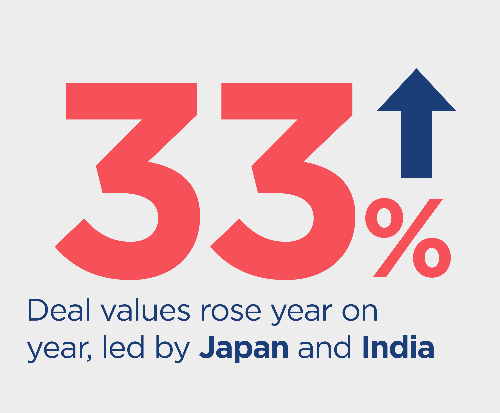

M&A activity across the Asia region was mixed in 2025, with strong pockets of deal activity in certain areas offsetting global uncertainty.

However, there were reasons for optimism, as deal values rose by one third compared to 2024, with Japan and India being key drivers of this growth.

Despite geopolitical and economic headwinds, investor appetite remained strong, particularly in the digital infrastructure, financial services, energy transition, industrials and healthcare sectors, which provides cautious optimism as we begin 2026.

Southeast Asia

Southeast Asia made a significant contribution to overall deal activity across Asia – albeit with fewer mega-deals and more small or mid-sized deals leading the way.

Overall, the region's diversity, strategic location and openness to innovation provided a solid foundation for dealmaking and growth.

There was also an uptick in interest from European and US-based investors seeking exposure to the region's growth story, particularly targeting consumer and technology, media and telecommunications businesses.

Singapore

In 2025, Singapore maintained its role as a regional hub for cross-border transactions. The continued popularity of Singapore holding vehicles, the rise in prominence of Singapore as a governing law, and the increasing number of regional (and sometimes global) deal and legal teams basing themselves in the city-state is contributing to this status. 2025 investment banking advisory fees from completed M&A deals were reported to be significantly higher than in 2024, signalling a healthy M&A environment as we head into 2026.

There were fewer mega-deals but a significant number of mid-size deals, with the energy and power, digital infrastructure, technology, healthcare, and logistics sectors continuing to attract significant interest.

Sovereign wealth funds and private capital played a major role in driving both inbound and outbound deal activity.

Indonesia

Indonesia maintained its status as an important M&A market in Asia despite a backdrop of geopolitical and domestic political uncertainties.

Nationwide protests over political misconduct in September 2025 temporarily slowed deal activity, but the government's policy response generally supported economic stability and sustained investor confidence.

Compared to the previous year, dealmakers were more cautious in 2025, with more intensive and prolonged due diligence processes, more extensive conditions to closing, and increased reticence in taking on Indonesia-related regulatory risks.

Transactions tended to concentrate on more mature businesses while early-stage and seed investments slowed as Indonesian startups entered later growth phases.

Investor interest from private equity and strategic buyers remains strong, particularly in the consumer, logistics, digital infrastructure and healthcare sectors, although the pool of available high-quality targets is limited.

Demand for nickel and gold remained robust despite tougher regulatory requirements in the mining sector. The government's drive for rapid expansion of Indonesia's electric vehicle (EV) industry has further fuelled demand for critical minerals, leading to increased transaction activity in related sectors.

In the energy sector, there has been a noticeable increase in upstream oil and gas activity, with growing momentum in renewable energy projects. However, public infrastructure activity slowed, particularly in the early part of 2025, but has shown signs of recovery.

Financial services and fintech also remain active, and bank and insurer consolidation persists due to higher capital requirements being imposed by regulators.

Significantly, Indonesia's new sovereign wealth fund, Danantara, was established in 2025 with the aim of consolidating control over, and driving consolidation and efficiency in, key state-owned enterprises and investment in strategic sectors, including renewable energy, minerals, digital infrastructure and public infrastructure.

Danantara's actual impact on dealmaking remains uncertain, as does its potential overlap with the Indonesia Investment Authority (INA), the existing sovereign wealth fund.

The INA, has however recently announced that it will now pivot towards investing in strategic private sector deals, leveraging its role as a co-investor alongside global partners. The authority plans to double down on investments in data centres, healthcare, renewable energy and advanced minerals such as rare earths in 2026, sectors viewed as foundational to Indonesia's long-term economic growth.

In terms of regulation, the government introduced new investment regulations in 2025 to provide greater clarity on licensing requirements, timelines for investments, and a reduction in the minimum paid-up capital for foreign investors.

The government is expected to revise the Investment List in 2026, and investors should monitor these changes closely.

In early 2026, global fund managers expressed growing concerns over the lack of transparency in public company ownership disclosure, even threatening country market status downgrade, which has led to the resignation of several senior regulators.

The government has announced that public company shareholder disclosure rules will be tightened and free-float requirements will be increased materially. These changes are expected to impact the structuring of Indonesian public company M&A transactions.

Thailand

2025 was a relatively muted year for Thailand's economic growth, especially in the first half, with a slight uptick from the third quarter onwards.

While activity in the energy and digital infrastructure sectors remained strong, policy uncertainties from trade tensions, constant political shifts and lagging service industries dampened dealmaking.

There was a regulatory crackdown on nominee structures designed to avoid foreign ownership restrictions, particularly in the tourism, hospitality, food, e-commerce, logistics and warehouses, agricultural, and real estate and construction sectors. Almost 50,000 companies were recently investigated and the regulator and law enforcement have established a working team to investigate existing entities.

The Trade Competition Commission (TCCT) is implementing changes to the Trade Competition Act, which would allow the commission to better capture cross-border conduct and transactions. The TCCT has also increased scrutiny on the e-commerce and logistics sectors, especially in terms of merger control.

Nonetheless, foreign direct investment (FDI) into Thailand continued to surge, with the first three quarters of 2025 showing a 94% increase year on year compared to 2024.

Recognising this trend, the Cabinet approved in-principle amendments to the Foreign Business Act B.E. 2542 in April 2025 to relax foreign ownership restrictions.

This was driven by the idea that the current law is overly protective of Thai investors and amendments were needed to align with current economic conditions and to enhance national competitiveness. The proposed changes place significant emphasis on the startup sector. The Ministry of Commerce has been tasked with the amendments. However, this policy may be subject to change under the new Thai government which is expected to be established in early 2026.

Similarly, we are seeing many bright spots in various policy-led sectors. Board of Investment incentives for data centres and EVs are catalysing pipelines in digital infrastructure and EV value chains. This has helped push forward large-scale data centre development projects in Thailand. As a result, we are seeing a surge in demand for land, power diligence and procurement in the region. We are optimistic that this will bolster economic growth in 2026.

Southeast Asia made a significant contribution to overall deal activity across Asia – albeit with fewer mega-deals and more small or mid-sized deals leading the way.

Other Southeast Asia regions

The Philippines, Malaysia and Vietnam also contributed to deal activity in 2025, with strong interest across their infrastructure, digital infrastructure and energy sectors.

The healthcare sector in these countries also continued to be an attractive area for investment, driven by demographic shifts and rising demand for quality medical services.

We are seeing a significant number of joint ventures and minority investments in these countries, particularly for foreign investors and for new entrants looking to partner with local strategics.

Mainland China and Hong Kong

Mainland China and Hong Kong experienced significant economic recovery in 2025, driven primarily by the IPO market, with Hong Kong recording a record year for IPOs.

There was also an increase in investors from other markets such as the Middle East and Southeast Asia which was unprecedented. Deal activity in mainland China and Hong Kong is expected to remain strong in 2026.

The resurgence in the IPO market in Hong Kong has primarily been driven by private capital investors in China and Asia seeking an alternate exit pathway. We expect to see increasing venture capital and buyout activity in the coming months, especially with investors increasingly seeking to diversify their investments geographically.

Despite the ongoing uncertainties around US tariffs imposed on China, M&A in China has remained buoyant and Chinese exports increased in 2025. This can be attributed to increased demand from Africa, Southeast Asia, the European Union and Latin America.

Chinese companies have also remained active in outbound deals, with direct outbound investment increasing 6% over 2024 levels. Investments concentrated on sectors such as technology, AI, green energy, EVs and batteries, advanced manufacturing, and infrastructure.

Top outbound investment destinations shifted toward emerging markets, especially Southeast Asia, Africa and the Middle East, while Europe and North America saw declines except for niche sectors such as EVs and tech in Central and Eastern Europe.

The Belt and Road Initiative (BRI) remained a major driver, with BRI countries accounting for 26% of non-financial outbound direct investment. These investments were strategically driven by technology acquisition, green energy transition, supply chain resilience and geopolitical positioning, supported by national policy priorities.

Japan

2025 was a standout year for Japanese M&A, with significant surges in both inbound and outbound transactions, and the market is well positioned for continued growth in 2026.

Structural reforms, favourable macroeconomic conditions and evolving corporate strategies drove momentum.

The Tokyo Stock Exchange's initiative requiring listed companies to operate with greater awareness of capital costs and share prices accelerated corporate governance reforms, enhancing capital efficiency and transparency.

This in turn stimulated M&A activity, with inbound acquisitions and take-private transactions - such as those by NTT and Toyota - reaching record highs.

Persistently low interest rates also supported acquisition financing, making Japanese assets attractive to global investors while simultaneously fuelling outbound investments.

Despite headwinds from a weakening yen, outbound M&A remained robust, driven by Japan's ageing population and cash-rich corporates seeking growth abroad - not only in Asia Pacific, but also in Europe and the US - and we expect this trend to continue long term. Japanese investors are also showing a renewed interest in India, with Mitsubishi UFJ Financial Group's planned investment in Shriram Finance as an example.

Technology remains a focal point, with sustained investments in AI and data centres. SoftBank's US$40 billion funding commitment to OpenAI highlighted Japanese companies' ambition to lead in innovation. Inbound interest in consumer assets and real estate remain strong, alongside heightened activity in the healthcare and industrial sectors - both offering long-term growth potential.

Japan's new prime minister, Takaichi Sanae, recently approved a record defence budget aligned with global trends which is expected to accelerate M&A and joint ventures in the sector.

Meanwhile, Japanese trading houses, historically cautious, are streamlining internal processes and competing more effectively in auctions, particularly for small and mid-market deals. Enhanced global due diligence standards have narrowed the gap between Japanese and international bidders, supporting competitive dynamics.

Click below to read our chapters on India and South Korea.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.