- with readers working within the Environment & Waste Management industries

- within Consumer Protection and Real Estate and Construction topic(s)

- in European Union

Welcome to Edition 41 of P2N0 covering the drive to avoid, reduce and remove greenhouse gas (GHG) emissions to progress to net-zero GHG emissions (NZE).

P2N0 covers significant news items globally, reporting on them in short form, focusing on policy settings and legal and regulatory, and project developments and trends. P2N0 does not cover news items about M&A activity or that are negative.

This Edition 41 covers significant news items from January 1, 2026, to January 31, 2026.

KEY ITEMS ARISING FROM JANUARY 1, 2026, TO JANUARY 31, 2026

The following are the key news headlines during January 2026:

- 2025 third hottest year on record: As the

facts and statistics flowed following the end of calendar year

2025, the World Meteorological Organisation (WMO)

stated that 2025 continued the three-year trend of

"extraordinary global temperatures" with surface air

temperatures averaging 1.48°C above preindustrial levels. If

this trend continues, global average temperatures will reach

1.5°C by 20301. There would appear to be a growing

consensus that the 1.5°C objective will be overshot, and given

this, that we need to consider how best to mitigate and to adapt to

the consequences of the overshoot.

On January 26, 2026, nature (at https://www.nature.com, under As we breach 1.5°C, we must replace temperature limits with clean-energy targets) published an article that makes the telling point that "actionable goals are needed to guide the world towards what needs to happen most quickly: shifting economies to clean energy sources".

While the development and deployment of renewable electrical energy and nuclear energy is occurring at a pace, allowing some countries to progress to net-zero, if one accepts the facts and statistics and the science, the rate of development and deployment needs to increase across all countries.

As noted previously, what needs to be done is known. The challenge, as pointed out by Bill Gates a little before COP-30 is balancing the cost of what needs to be done with other calls on finite funding. - Coal-fired generation falls in China and India

year-on-year: For the first time since 1973, there was a

fall in the electrical energy generated from coal-fired sources

year-on-year: less electrical energy was generated from coal-fired

power plants in 2025 than in 2024. Carbon Brief reported that

electrical energy generated from coal fired power plants in China

fell by 1.6% and in India by 3%.

China and India continue to make progress to net zero. In 2025, China installed around 435 GW of renewable energy capacity, 315 GW of PV solar and 119 GW of wind power2. India installed around 35 GW of PV solar and 6 GW of wind power, and 3.5 GW of hydroelectric power. While coal-fired power generation fell year-on-year, nevertheless China installed 95 GW of capacity.

It is hoped that China and India have now reached peak use of coal-fired power plants to generate electrical energy. - EU continues energy transition: On January 22, 2026, Ember reported that "2025 was another Record- breaking year for EU energy transition", with photovoltaic solar and wind overtaking "fossil fuels in the EU energy mix" across the EU. In 14 out of the 27 Member States, photovoltaic solar and wind exceeded dispatch of electrical energy of fossil fuels in the electrical energy generation mix.

- BloombergNEF: Energy Transition Investment

Trends: During January 2026, BloombergNEF published its Energy Transition Investment Trends –

Tracking global investment in low-carbon transition, in both

long-form and abridged form. The headline from the publication is

that during 2025 there was USD 2.3 trillion of global energy

transition investment.

As is often the case, it is worth reading beyond the headline of the USD 2.3 trillion: -

- "USD 893 billion spent to purchase electric vehicles ... and developing infrastructure in 2025, up 21% [from 2024]";

- USD 690 billion committed to the development of new renewable energy generation capacity and related infrastructure, USD 84 billion committed to electrified heat, USD 71 billion committed to energy storage, USD 36 billion and USD 34 billon committed to clean industry, in total USD 915 billion; and

- USD 438 billion committed to the development of electrical energy grids.

- These are the key areas of investment, and they are related. In comparison, the amounts committed to CCS at USD 6.6 billion and Hydrogen at USD 7.3 billion, tend to indicate the assessment that renewable energy development and complementary investment offers the best investment as things stood during 2025.

- AI Energy Consumption: One of the themes of

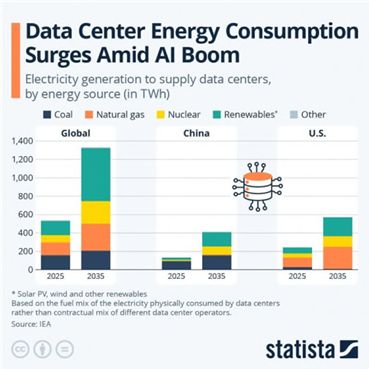

the last 18 to 24 months has been the increased demand for

electrical energy to power data centers in the context of the

ever-increasing need for processing and storage of data.

Statista, borrowing from the International Energy Agency (IEA), have published the following bar chart to provide a sense of the demand for electrical energy for data centers in 2025, and the estimated demand in 2035. The bar chart covers global, China and US demand.

- EIA AI idea: On January 21, 2026, the US Energy Information Administration (EIA) released an article entitled Air power: Tallying electricity generating potential from retired military aircraft. The EIA article estimates that turbine-based engines (other than turbojets) on retired military aircraft have the capacity to generate up to 40 GW: it is important to note that this is a theoretical estimate, not a state of immediately available capacity.

- AI regulation: AI is giving rise to increased

electrical energy demand. Also, the use of AI is getting increased

attention from government to regulate the use of AI (including

content arising from it).

On January 22, 2026, an AI law came into effect in South Korea. While the EU adopted regulation on AI in 2024 that regulation will not come into full effect until As such, South Korea is the first country globally to have introduced legislation to regulate AI through its AI Basic Act. The AI Basic Act is intended "to establish a safe and trust-based environment to support AI innovation". - Carbon Border Adjustment Mechanism (CBAM) came into

effect on January 1, 2026:

During 2025, there was considerable coverage of the introduction on CBAM (positive and negative), and this continued throughout January What follows is a brief summary of CBAM. -

- Origin of CBAM: The European Union (EU) has

long sought to avoid, reduce, and remove GHG emissions, with

considerable success. One of the key reasons for this success is

that the EU placed a price on carbon through the introduction of

the EU Emissions Trading Scheme (ETS)3. The EU ETS,

directly and indirectly, has promoted the adoption of lower, low

and no GHG emission

The EU is concerned that the success that it has had is undermined by carbon leakage4; carbon leakage will lead to an increase in total global GHG emissions, and as such undermine the objective so the Paris Agreement5.

To address the EU's concerns (and as one of the climate change policies under "Fit for 55"), the EU introduced CBAM; the essence of CBAM is to ensure that there is equivalent carbon pricing for imports into the EU and domestic products produced within the EU. Implicit in the policy thinking informing the introduction of CBAM is that countries from which products are imported into the EU do not have equivalent carbon pricing. - Application of CBAM: CBAM applies to the import of prescribed products, being aluminium, cement, electricity, fertilisers, hydrogen, and iron and steel. For the time being, fertilisers are exempt from the application of CBAM. If a production process gives rise to CO2 that is captured and stored permanently, the captured and stored CO2 emissions will not count for the purposes of reporting on the actual GHG emissions arising on the production of that product.

- Achieving equivalent cost of carbon: The importer of prescribed products must acquire CBAM Certificates, i.e., equivalent to the acquisition of emissions permits for liable entities under the EU Each CBAM Certificate represents one metric tonne of CO2-e of embedded GHG emissions in the applicable prescribed product, arising from the production of that product.

- Origin of CBAM: The European Union (EU) has

long sought to avoid, reduce, and remove GHG emissions, with

considerable success. One of the key reasons for this success is

that the EU placed a price on carbon through the introduction of

the EU Emissions Trading Scheme (ETS)3. The EU ETS,

directly and indirectly, has promoted the adoption of lower, low

and no GHG emission

- The EU CBAM is the first Border

Adjustment Mechanism to come into effect.

On January 9, 2026, Halina Yermolenko published an article entitled 2025 for carbon markets: new launches and plans (at https://gmk.center/en/infographic/) that considers the initiatives around the world to place on a price on carbon domestically and on imported products. - Incentivising use of Biofuels and Methanol: From January 1, 2026, the Yokohama Port and Harbor Bureau is waiving port entry fees to the Port for vessels powered and propelled by biofuels and methanol. This is part of a broader plan to decarbonize activities at Yokohama Port, which itself is part of the initiatives to decarbonize Japanese society by 2050.

- Adoption of ISSB standards continuing and CSRD and CSD settled: As noted below, on January 5, 2026, China implemented International Standard Board (ISSB) IFRS S2. China is not alone, with a further 18 countries having adopted standards6. There is a further 21 countries moving towards adoption of the standards. This marks continued progress.

- P2N0 reported on the Corporate Sustainability Reporting Directive (CSRD) and Corporate Sustainability Due Diligence Directive (CSDDD or CSD3) throughout 2025.

-

- On December 9, 2025, the Council and the European Parliament reached agreement at a political level om the Omnibus Simplification Package (Omnibus I) in respect of CSRD and CSD3

- On December 16, 2025, the European Parliament voted in favor of scaling back sustainability reporting and due diligence requirements (428 votes in favor, 218 against, with 17 abstentions).

- Omnibus I, through the CSRD, contemplates the revision of the European Sustainability Reporting Standards (ESRS). On December 3, 2025, the EFRAG published its revised technical advice (see Draft Simplified ESRS/EFRAG). The EC is able to adopt the ESRS as a delegated act having consulted, among others7, with Member States. Subject to this consultation, and the outcome of it, it is expected that the EC will make a decision around adoption by the end of Q1 of 2026.

- Offshore wind field industry alive and well after

AR7: One of the second-tier themes that has emerged over

the last two years or so has been the challenges faced by the

offshore wind industry

On January 14, 2026, the Department for Energy Security and Net Zero (DESNZ) announced the results of allocation round seven (AR7): -

- 2 GW of fixed-bottom offshore wind capacity was awarded, with:

-

- 6,885 GW at £91.20 MW/h around England and Wales;

- 1,380 GW at and £89.49 MW/h around Scotland; and

- 5 MW of floating offshore wind at test and demonstration sites – Erebus (100 MW) and Pentland (92.5 MW).

- The fixed-bottom wind field

developments are:

The UK Government is to provide support of up to £1.8 billion. This is double the £900 million of support earmarked for AR6.Awel y Mor – 775 MW – RWE Berwick Bank – 1380 MW – SSE Dogger Bank South East - 1500 MW – RWE and Masdar Dogger Bank South West – 1500 MW – RWE and Masdar Norfolk Vanguard East – 1545 MW – RWE Norfolk Vanguard West – 1545 MW – RWE

Ahead of the results, PA Consulting published UK Offshore Wind: CfD AR7 Analysis. The publication provides helpful factual and historical context of AR7. - The 2026 Energy Security Scenarios – Challenges

to the transition: During January 2026 Shell published The 2026 Energy Security Scenarios –

Challenges to the transition. The publication takes stock of

the last 20 years (including The Energy Security Scenarios published by it

in March 2023), pausing to reflect at the end of 2025, and looks

forward 15 and 20-years to 2040 and 2045.

In the context of pausing to reflect at the end of 2025, the publication reflects on, and author has picked out the key forward looking matter identified: -

- Geopolitics, society, and technology: Over the next 25 years about one third of the world's increasing population (about three billion people) will embrace higher income lifestyles, including taking their first flight and buying their first motor vehicle. Demand for energy will continue to increase as the world's population becomes increasingly urbanised and living standards rise. The generation of electrical energy will become less centralised and concentrated as the adoption of photovoltaic solar, wind, energy storage, and heat pumps technologies increases;

- Energy demand: By 2050 the demand for primary energy could increase by up to a quarter compared to 2025. Demand for oil is likely to increase by 3 to 5 million barrels a day into the early 2030s, with a long slow decline after that time. Demand for natural gas will continue to increase, reaching 4,500 billion cm3 a year by 2040, of which up to 700 million metric tonnes will be LNG;

- The energy mix: Electrification is set to increase across all sectors and all economies, and by the second half of the century will dominate the energy supply side, with natural gas and LNG remaining as an important industrial fuel, and oil required for petrochemical applications. By 2060, in the northern latitudes, at least two thirds of the demand for electrical energy will be matched by the supply of renewable electrical energy; and

- Carbon management: Carbon capture and storage will become a multibillion tonne a year industry during the 21st The challenge is the need for a concerted effort to reduce the GHG emissions arising from agricultural, forestry and other land use.

- Innovation Landscape for Sustainable Development Powered by Renewables: On January 10, 2026, the International Renewable Energy Agency (IRENA) published Innovation Landscape for Sustainable Development Powered by Renewables. The publication notes that the technologies exist to decarbonize the generation of electrical energy and to provide universal access to electrical energy. While the publication in its entirety is well-worth a read, the executive summary is excellent, in particular the examples of innovations reshaping the supply of electrical energy across energy markets, with a focus on African markets.

- China energy finance in emerging and developing

economies: On December 22, 2026, the International Energy

Agency (IEA) published China's Official Energy Finance in Emerging

and Developing Economies – Evolving Institutions, instruments

and implications for clean energy transactions. The publication

sets the scene as follows: capital flows remain uneven. Emerging

market and developing economies (EMDE) outside China attracted just

27% of total energy investment and 18% of clean energy spending ...

."

The publication outlines the trends in the provision of finance by the official financing sector8 to fund the development of energy projects outside the country, providing case studies on projects in Uzbekistan, Peru, the Kingdom of Saudi Arabia, South Africa, Guyana, and Indonesia.

Americas

- Microsoft obtains Data Center approvals: On January 26, 2026, it was reported widely that Microsoft had obtained approvals for the development of 15 buildings to house new data center capacity, covering 1,148,000 square feet. The new data center capacity will be located close to Microsoft's existing Data Center campus in Mount Pleasant, Wisconsin. As reported, the development of the new data center capacity has a value of USD 13 billion.

- Microsoft commits to soil carbon credits: On

January 15, 2026, it was reported widely that Microsoft had agreed

to acquire 2.85 million carbon credits (over a 12-year period) from

Indigo Carbon. As reported, the carbon credits will arise from the

effects of regenerative agriculture in the US and have been priced

within a range of USD 60 to 80 a carbon credit.

By way of reminder: Microsoft is committed to being a negative GHG emissions corporation by 2030. With the agreements with Indigo Carbon, and an earlier agreement with Agoro Carbon (for 2.6 million carbon credits), Microsoft remains in pole position as the buyer of most carbon credits. - Meta signs agreements for the provision of nuclear energy: On January 9, 2026, world nuclear news (at world-nuclear-news.org, under Meta announces 'landmark' agreements for new nuclear) reported that Meta had:

-

- signed power purchase agreements with Vistra Corp for 2,176 MW of nuclear energy from existing plants, Perry and Davis-Besse, in the US State of Ohio;

- signed funding support agreements with TerraPower to support the development of up to eight Natrium sodium fast reactors, 690 MW to be delivered by 2032 and options in respect of the offtake of up to 2.1 GW of nuclear energy by 2035; and

- signed an agreement to pre-pay for energy so as to provide support to develop a 1.2 GW power campus in Pike County, in the US State of Ohio.

- US to withdraw from United Nations Framework Convention

on Climate Change (UNFCCC): On January 7, 2026, the

President of the US, by Presidential Memorandum, indicated that the US

would withdraw from a number of United Nations' agencies and

organizations, and conventions and treaties, including from the

UNFCCC. Withdrawal from the UNFCCC requires notice of a year.

The announcement of the withdrawal of the US was accompanied the news that during 2025, year- on-year, GHG emissions in the US had increased: the increase is reported as around 140 million metric tonnes (or a 2.5%) increase from 2024. As reported, a fair proportion of this increase has resulted from increased demand for electrical energy to power data centers and cold - McDermitt Caldera attracts attention: On

January 6, 2026, earth.com (under earth.com, under Lithium deposit valued at $1.5 trillion has been

discovered in the US) reported on the McDermitt Caldera lithium

resource in the US State of Oregon close to the border with the US

State of Nevada. While P2N0 has covered the

McDermitt Caldera resource, the reporting from earth.com provides

us with a reminder of the scale of the resource – between 20

and 40 million metric tonnes of lithium. It is understood that the

resource is a claystone deposit.

By way of reminder: Edition 29 of P2N0, under McDermitt Caldera contains World's Largest Lithium Deposit reported that: "On April 7, 2025, indiandefencereview (at indiandefencereview.com, under Geologists Uncover the World's "Largest Lithium Deposit" Under American Supervolcano Worth 413 Billion Euros) reported on an article published in the journal Science Advances identifying lithium (and other) resources in the McDermitt Caldera. As reported, the McDermitt Caldera has "lithium-bearing clay minerals, including smectite and illite", with an exceptional concentration of lithium found in the illite layer". - Samsung breaks ground on Wabash Low-Carbon Ammonia Plant: On January 6, 2026, it was reported that Samsung E&A had commenced construction work on the development of Wabash Valley Resources' Wabash Low-Carbon Ammonia Project in Terre Haute, in the US State of Indiana. The Project involves the use of a coal-fired plant to produce 500,000 metric tonnes blue ammonia annually, using coal as the feedstock to produce hydrogen, and then to combine that hydrogen with The CO2 emissions arising will be captured and stored. Completion of construction is scheduled for 2029. The Project has received funding support from both U.S. and Korean governments.

- Illinois proceeds quietly: On January 7, 2026, the Governor of the US State of Illinois signed the Public Act 104-0458 (referred to commonly as that Clean and Reliable Grid Affordability Act).

- Beaumont Ammonia project commissioning: On January 2, 2026, Woodside Energy Limited announced that commissioning had commenced at its USD 2.35 billion Beaumont blue ammonia project in the US State of Texas, and that blue ammonia is being produced during commissioning.

- Chile 2050 Energy Transition Roadmap: During January 2026, the International Energy Agency (IEA) published Chile 2050 Energy Transition Roadmap. As with other country orientated publications from the IEA, this publication is fascinating, providing a clear understanding of the demand for energy, energy consumption, and the power sector. For those interested in Chile, this is a must read.

- Singapore carbon tax to increase: During January 2026 it was reported widely that the carbon tax in Singapore is to increase from SD$25 a metric tonne of CO2-e to SGD$45.

Africa

- US 1 billon investment in CDR projects: On January 30, 2026, the carbonherald (at https://carbonherald.com, under The Miombo Restoration Alliance, Backed By Trafigura, To Invest Over $1B In Four CDR Projects) reported that the Miombo Restoration Alliance has picked the first four African carbon dioxide removal (CDR) projects to receive funding. As reported, the projects have a 40-year timeline, and USD 1 billion will be invested over that timeline.

- Natural gas and LNG: On January 27, 2026, the International Gas Union published a piece on LinkedIn analysing the increasing role that the production of natural gas and LNG may play domestically and globally. The article reminded us of the Gas for African Report 2025 published on November 24, 2025, which was published as COP-30 was still grabbing the headlines. Both the article and the report are well worth a read.

- Germany and South Africa progressing retirement of coal-fired capacity: On January 23, 2026, Business Insider Africa (at https://africa.businessinsider.com, under Germany to back Africa's richest country with €720 million move away from coal) reported that Germany and South Africa are in discussions which may lead to Germany providing up to €720 million in additional concessional funding support under the Just Energy Transition Partnership (JETP). This additional concessional funding would increase the funding provided by Germany under JETP to €2.68 million.

- Egypt continues to commit to renewable energy:

On January 11, 2025, it was reported widely that a number of

agreements had been signed to allow the continued develop of

renewable energy capacity across Egypt, including with Scatec for

the development 7 GW of PV solar capacity and with Sungrow for the

development of a battery manufacturing facility.

By way of context: Egypt intends to generate 42% of its electrical energy needs from renewable sources by 2030. - Egypt and Israel hone-in on natural gas deal: On January 9, 2026, mees (at https://www.mees.com, under Israel-Egypt Gas Deal: Not Over the Line Yet) provided an interesting perspective on the approval of the expansion of the Leviathan Gas Project. The finalization of the gas sale and purchase agreement is essential for a positive final investment decision (FID) to expand production capacity from around 1.45 billion cubic feet a day to 2.1 billion cubic feet a day.

Europe and the UK

- Federal Germany Government to provide €349 million for e-SAF facility: On January 29, 2026, hydrogeninsight (at https://www.hydrogeninsight.com, under Germany grants €349 of public funding to green hydrogen-based e-SAF project) reported that the Federal German Government had agreed to provide funding for the development of an e-SAF facility to be located in Schwedt. As reported, the funding will cover around 70% of the total development cost of the e-SAF facility, with the facility to produce up to 30,000 metric tonnes of e-SAF a year.

- EU Taxonomy came into effect on January 28, 2026: Having been published in the Official Journal on January 8, 2026, on January 28, 2026, the EU Taxonomy entered into The EU Taxonomy provides the basis for reporting on economic activities in a clear and consistent way across the EU9. While the EU Taxonomy came into effect on January 28, 2026, financial undertakings may opt out of its use from January 1, 2026, to December 31, 2027. As a general statement, the EU Taxonomy may be regarded making reporting proportionate and simpler.

- Heat arising from data center is uses to heat technological campus heating demand in Dublin: On January 27, 2026, cnbc (at cnbc.com, under This university campus is heated by an AI data center. Your home could be next) reported that since 2023 the Technological University on Tallaght Campus, Dublin, Republic of Ireland, that is heated by waste heat from the nearby Amazon Web Services data center.

- Air Liquide commissions cracking plant: During the final week of January 2026, it was reported widely that Air Liquide had commissioned its ammonia to hydrogen cracking plant at the Port of Antwerp- Bruges, Belgium. It is understood that this is a world first: the cracking plant will allow ammonia imported into Europe, as a hydrogen carrier, to be cracked to derived hydrogen.

- The European Hydrogen policy landscape – Extensive update to January 2025 report was published on January 28, As the title suggests, the publication is an update of a report from 2025. For those interested in a light-touch analysis of policy settings across the EU, the publication is well-worth a read.

- EU finalizes arrangements for six successful bidders in

the second EHB10 auction: On January 19, 2026,

the EU approved the contracts for the six successful bidders in the

second EHB auction. Together, the six successful bidders will

receive around €271 million in funding In parallel, Austria,

Lithuania and Spain allocated up to €836 million of

funding.

The six successful bidders (in the second EHB auction) that have signed grant documentation are: -

Successful Bidders Project Developer Country Quantity bid GHG avoided Bid price Bid capacity Krostinestad PtX Koppo Energia Oy Finland 258,000 tonnes 1,763,000 tonnes €0.33 per kg 200 MWe H2CRI Green Devco Energy Spain 30,000 tonnes 204,000 tonnes 0.44 per kg 30 MWe NOON Iberdrola Clientes Spain 161,000 tonnes 1,104,000 tonnes 0.84 per kg 120 MWe GH2Move-VLC Diverxia Infrastructure Spain 2,000 tonnes 15,000 tonnes 0.85 per kg 5 MWe RjukanH2 Norwegian Hydrogen Norway 29,000 tonnes 201,000 tonnes 0.45 per kg 18.75 MWe HammerfestH2 Green H AS Norway 12,000 tonnes 80,000 tonnes 1.88 per kg 7.5 MWe - Germany gets green light to provide funding support for H2Global tender with Canada: On January 15, 2026, it was reported widely that the European Commission had approved up to €200 million in State Aid from the Federal German Government. The funding is one half of the €400 million of funding, half from the Federal German Government (through H2Global) and half from the Canadian As reported, the funding will provide funding to support the development of up to 300 MW of renewable hydrogen production capacity in Canada. The development of the capacity in Canada represents a further step in the role of H2Global in the procurement of renewable hydrogen, a renewable fuel of non-biological origin (RFNBO).

- Germany gets green light to provide funding support for new hydrogen ready gas-fired generating capacity: On January 14, 2026, the EU approved, in principle, the provision of State Aid by the Federal German Government to progress the development of up to 12 GW of hydrogen-ready gas fired generating capacity.

- RED III RFNBO: On January 9, 2026, Spain published revised draft legislation to provide for the use of renewable hydrogen (and fuels and feedstock derived from it) in the transport sector. The draft legislation mandates RFNBO usage targets to apply from 2028 to 2040 and in so doing provide demand side development.

- UK Corporate Power Purchase Agreements call for evidence: On January 9, 2026, the UK Government (Department for Business and Trade and Department for Energy Security & Net Zero) published an Open call for evidence, Corporate Power Purchase Agreements. The main thrust of the Open call for evidence is to consult and to understand how the market for Corporate Power Purchase Agreements can be developed to reduce the costs of electrical energy of industry across England, Scotland and Wales. The purpose of the Open call for evidence is welcome.

- Capital Clean Energy Carriers (CCEC) takes delivery of

world's largest CO2 carrier:On January 6,

2026, announced that it had taken delivery of the 22,000 m3 new

ship build from HD Hyundai Mipo.

By way of reminder: Edition 30 of P2N0 reported that: "On April 16, 2025, it was reported widely that the world's largest liquid carbon dioxide (LCO2) carrier had been launched. As reported, the LCO2 carrier has the capacity to carry 22,000 m3 of LCO2. The LCO2 carrier is the first of four LCO2 carriers (with a total cost of USD 756 million) ordered by the Greek shipping company, Capital Clean Energy Carriers, from South Korean shipbuilder, HD Hyundai Mipo. - Price of carbon scaling heights: During January 2026 the price of carbon in the EU (including CBAM Certificates) and the UK touched €90 and £70 respectively. It is expected, at least in the short term, that there will be volatility around pricing in the EU ETS and the UK ETS secondary markets.

- Germany completes first 400km of pressurized hydrogen

pipeline: On January 12, 2025, it was reported widely that

construction of the first 400km of the hydrogen backbone for the

transmission of hydrogen across Germany had been completed. While

P2N0 does not cover negative news items, we

should note that there has been considerable comment about the fact

that, as yet, the 400km of hydrogen backbone infrastructure does

not have any meaningful supply and offtake

On January 30, 2026, Energinet commenced its marketing process to sell capacity in the Danish Hydrogen Backbone 1 (DHB1). DHB1 will allow the transportation of hydrogen by pipeline from Denmark into Germany. It is understood that the marketing process will continue through 2026 on a first-come- first-served basis. - Natural gas and LNG supply within the EU: During 2025 the EU imported 7 billion m3 of natural gas, comprising natural gas hauled by pipeline (169.9 billion m3) and LNG (143.1 billion m3). Imports from Norway were 97.1 billion m3 and from the US 82.9 billion m3. As the EU moves to ceasing to take natural gas from Russia, it is to be expected that the EU will increase the import of LNG from the US.

- Renewables take the lead in Germany: On January 1, 2026, Fraunhofer ICE (at https://www.ise.fraunhofer.de, under German Public Electricity Generation in 2025: Wind and Solar Power Take the Lead For the First Time) reported that renewable electrical energy generation in Germany amounted to 9% the net demand for electrical energy by the public across the country.

Middle East, Central Asia, and South Asia

- Joint EU-India Comprehensive Strategic Agenda: On January 27, 2026, the European Commission issued a statement - Towards 2030: A Joint European Union-India Comprehensive Agenda. The statement provides a high-level summary of initiatives relating to the Strengthening supply chains and economic security and Advancing the clean transition and In addition, there are more general agreements around cooperation to implement the Paris Agreement and to work towards the Kunming-Montreal Global Diversity Framework.

- World Bank approves Regional Market Interconnectivity and Trade (REMIT) Program: On January 22, 2026, the Board of Executive Directors of the World Bank approved REMIT will be implemented in three phases over a 10-year period and will achieve electrical energy connectivity across Central Asia.

- Roadmaps for Aluminium and Cement Sector Decarbonisation: During January 2026, the Government of India, NITI Aayog, published:

-

- a Roadmap for Aluminium Sector The publication is timely, with the production of aluminium in India giving rise to up to 100 million metric tonnes of CO2-e GHG emissions annually around 75% of these GHG emissions arise from the use of electrical energy (at smelters) generated from coal-fired power stations. As such, the key issue for the aluminium sector is increasing the use of electrical energy generated from renewable sources and nuclear power. The publication provides a roadmap for this; and

- a Roadmap for Cement Sector The publication places cement production in India in a global context – India is the world's second-largest cement producer and contributes around 7% of the GHG emissions arising in India. As those familiar with the cement sector will know, around 55% of GHG emissions in cement production arises from the calcination of limestone (one metric tonne of cement giving rise to one metric tonne of CO2), 33% from the use of fossil fuels to provide high-heat, and 12% arise from the use of fossil fuels to generate electrical energy. The roadmap outlines the use of refuse-derived fuel (derived from municipal solid waste), replacing limestone as a feedstock, and CCS. The effective implementation of the roadmap is estimated as likely to reduce GHG emissions by up to 85%.

- The Cost of Green Hydrogen in Saudi Arabia and Germany: During January 2026, Kapsarc (at https://apps.kapsarc.org) published an analysis of the cost of green hydrogen production in Saudia Arabia for export to Germany. The publication covers photovoltaic and concentrated solar and wind and BESS, production technologies (including electrolyser types) and transport and export dynamics. The publication is well-worth reviewing, if only for the model.

- AM Green Group and Uniper sign long-term offtake agreements for GNH3 and breaks ground:

-

- On January 12, 2026, it was announced that AM Green Ammonia India Private Limited (AM Green Ammonia) had signed a long-term contract for the supply of 500,000 metric tonnes of green ammonia a year to Uniper Global Commodities SE (Uniper). The green ammonia will be certified as a Renewable Fuel of Non-Biological Origin (RFNBO). As announced, the green ammonia will be sourced from green ammonia projects within the AM Green Group, with the first cargo expected as early as 2028 from the AM Green Ammonia 1 million metric tonnes a year plant located in Kakinada, in the Indian State of Andhra Pradesh.

- On January 19, 2026, it was announced that AM Green had broken ground on its 1.5 million metric tonnes a year at Kakinada, with first production of 500,000 metric tonnes expected by mid-2027.

- By way of reminder: Uniper has been active across the US, Canada, Norway, and Oman in seeking to contract for green ammonia, with memoranda of understanding to offtake green ammonia. The agreement between AM Green and Uniper places it in the top 10 of ammonia offtake agreements (blue and green ammonia) signed to date.

APAC

- CNPC injects 1 million tonnes of CO2 into Xinjiang Oilfield:On January 29, 2026, the globaltimes (at https://www.globaltimes.cn, under China's CNPC reports first one-million ton CO2 injection oilfield in Xinjiang region) reported that China National Petroleum Corp (CNPC) has injected more than 1 million metric tonnes of CO2 into the Xinjiang Oilfield during 2025. As reported, more than two million tonnes of CO2 have been injected into the Xinjiang Oilfield since 2022. It is key to note that petroleum operations have continued at the same time as injection of CO2 has taken place, i.e., this is not a standalone CCS project.

- Digital Edge scopes data centre campus in Indonesia: On January 28, 2025, The Business Times (at businesstimes.com.sg, under Singapore-based Digital Edge to build US$4.5 billion data centre campus in Indonesia) reported that Digital Edge (backed by Stonepeak Partners) intends to invest USD4.5 billion to develop one of the largest data centres in Indonesia, the CGJ Campus, Bekasi. As reported that data centre will provide 500 MW of capacity for an AI-ready hyperscale facility.

- Construction of Xuwei Nuclear Heating and Power Plant commences: On January 17, 2026, interesting engineering (at interestingengineering.com under China starts building world's first hybrid nuclear plant for 33-million-ton industrial steam) reported that first concrete had been poured to develop the Xuwei Nuclear Heating and Power Plant in Jiangsu As reported, the Xuwei Nuclear Heating and Power Plant is the world's first large-scale facility to couple the generation of electrical energy and heat using nuclear technology to produce petrochemicals. The facility is being developed by the China National Nuclear Corporation (CNNC).

- Indonesia reclaims more than 4 million hectares: On January 14, 2026, Mongabay (at mongabay.com, under Indonesia says 4 million hectares of plantation mining land reclaimed in crackdown) reported that the Government of Indonesia has reclaimed more than 4 million hectares (or 9.9 million acres) of land that were being used unlawfully for mining and plantation activities, including mining activities without approval for activities in forest-areas, palm oil plantation activities without forest-area permits, and unlawful gold mining. The reclamation and enforcement have been undertaken under the authority provided by Presidential Decree No.5 2025, issued on January 21, 2025.

- Thailand bamboo solution: On January 14, 2026, click petroleoegas (at en.clickpetroleogas.com, under Thailand installs kilometres of bamboo barriers, reduces waves by up to 70% and recreates mangrove forests to hold back the advancing sea and recover coastal areas) reported that Thailand uses bamboo barriers that reduce waves by up to 70% and in so doing allow the recreation of mangrove forests, curbing coastal erosion with a simple, inexpensive, and ecologically sound solution.

- Australia to establish strategic reserve for critical

mineral supply: On January 12, 2026, the Federal

Government of Australia announced that it would establish an AUD

1.2 billion Critical Minerals Strategic Reserve The Reserve is

intended to ensure that Australia has sufficient reserves of

CM311 and REE12 to benefit the

economy of Australia and to ensure national security: the Reserve

will be funded to purchase CM3 and REE, which will be stockpiled,

and then sold as needed. It is understood that among the first CM3s

to be purchased and stockpiled will be antimony, gallium and

REE.

On Monday January 19, 2025, the Federal Treasurer of Australia, Mr Jim Chalmers, attended a meeting of G7 finance ministers to discuss international cooperation in developing reliable supply chains for CM3 and REE.

In addition to Australia, India attended the G7 finance ministers meeting. The development of BESS projects in India to the scale planned (208 GWh of BESS capacity by 2030), provides a sense of the need to continue to develop, and to expand and to diversify, reliable supply chains.

To provide context to this activity, the World Economic Forum, working with Kearney, published From Minerals to Megawatts: Building Resilient Supply Chains. The publication considers the sources and uses of 19 CM3 and REEs, and the risks that arise across three CM3 and REEs intensive value chains, Data Centres, EVs and Power Grids.

Finally, on January 27, 2026, the IEA published Designing an effective strategic stockpiling system for critical minerals. The publication provides a helpful overview of the drivers for the establishment of stockpiling of CM3 and REE. - China activates first 1 GWh supercapacitor-energy storage project: On January 9, 2026, pv magazine (at https://www.pv-magazine.com, under China's switches on world's first GWh-scale supercapacitor energy storage) reported that the China National Nuclear Corporation's (CNNC) supercapacitor- based hybrid energy storage system (SBHESS), known as the Jiayuguan NingShang 500 MW / 1 GWh project, had connected to the transmission grid in northwest China on December 30, As reported, the SBHESS, has a hybrid configuration combining 475 MW / 1 GWh of lithium iron phosphate batteries with a 25 MW supercapacitor system capable of discharge within 60 seconds.

- SMR completes non-nuclear steam start up in China: On January 8, 2026, world nuclear news (at world-nuclear-news.org, under Chinese SMR completes non-nuclear steam start up test) reported that a small nuclear reactor (SMR), an ACP100 SMR, has passed its non-nuclear turbine test run at the first attempt. The ACP100 SMR is part of a demonstration project in Hainan province. CNNC announced: "As the world's first commercial land-based small modular reactor ... the trial achieved stable operation across all systems, with the steam turbine generator unit meeting all designated parameters."

- Australia records record renewable energy dispatch: Over January 7, 8 and 9, 2026, dispatch of electrical energy from renewable energy generation reached the 1st, 2nd, and 4th highest demand peaks across the National Electricity Market (NEM). On each of these days, renewable electrical energy dispatch matched over 60% of peak demand across the NEM.

- KHI to build largest LH2 carrier:On January 6, 2026, it was reported widely that Kawasaki Heavy Industries (KHI) had agreed with Japan Suiso Energy (JSE) to build the world's largest liquefied hydrogen (LH2) The LH2 carrier will be able to carry 40,000 m3 of LH2. KHI built the Suiso Frontier (able to carry 1,250 m3 of LH2) which carried liquified brown hydrogen from Australia to Japan in early 2022 and developed a design for a 40,000 m3 containment system. Funding support for the development of the LH2 carrier is to be provide by the Green Innovation Fund.

- Japan to incentivise use of clean power: On January 5, 2026, carbon credits (at https://carboncredits.com, under Japan to Invest US$1.34B on Clean Power to Spur Energy Transition) reported that the Government of Japan will provide subsidies to corporations that commit to the use of clean As reported, to be eligible corporations must commit to use 100% decarbonized electrical energy, and the subsidies may cover up to 50% of capital costs incurred by corporations. The funding for the incentivisation will come from the Green Transformation (GX) 2040 Vision initiative.

- Baosteel integrates DRI facility with its Zhanjiang steel mill: On January 5, 2025, it was announced that the Baosteel Zhanjiang Iron & Steel had integrated its direct reduced iron (DRI) plant into the rest of its Zhanjiang steel mill in Guangdong The DRI plant was developed during 2024, using Energiron Zero Reformer technology developed by Danieli and Tenova. As described, the technology reduces CO2 emissions using hydrogen to capture carbon, and as such will provide a "near-zero carbon" production line.

- China Corporate Climate Reporting Standard: On January 5, 2026, China implemented International Standard Board IFRS

HELPFUL PUBLICATIONS AND DATA BASES

In addition to publications covered by this edition of P2N0, the most noteworthy publications read by the author during the period from January 1, 2026, to January 31, 2026, are:

- During January 2026, the Massachusetts Institute of Technology (MIT) published its 2025 Global Change Outlook. The publication provides a stark analysis of the current and projected climate change

- During January 2026, the International Renewable Energy Agency (IRENA) published:

-

- Renewable Energy Auctions – Design Risk Allocation, which outlines the IRENA renewable energy auction design framework;

- Fostering A Just Energy Transition – A framework for policy design, which provides the perspective of IRENA as to that which is required for a just energy transition, which informs the framework propounded for effective policy design;

- Innovation Landscape for Sustainable Development Powered by Renewables, which provides guidance (in the form of toolkits) in respect of innovation to modernise grids, including to improve resilience and how to decentralise grid resilience, and how to accelerate access to grids for renewable electrical energy, and how to deploy local resources for these

- The Role of Gas in Powering AI-Driven Energy Demand: On January 15, 2026, the IGU (at https://www.igu.org, under The Role of Gas in Powering AI-Driven Energy Demand) published its assessment of the role of natural gas in generating electrical energy for data centres as the artificial intelligence (AI) economy The publication provides a balanced and clear-eyed perspective.

- The Value of Demand Flexibility: On December 23, 2025, the International Energy Agency (IEA) published The Value of Demand Flexibility. The publication provides a clear guide to the value of demand side management to ensure the efficient operation of electrical energy transmission and distribution systems.

- During January 2026, Carbon Market Watch published Carbon Pricing Done Right – Key elements for fair and effective emission trading systems that work for people and climate. The publication provides a helpful summary of the benefits and the means of implementing a price on carbon.

Footnotes

1. By way of reminder, Article 2.1(a) of the Paris Agreement provides for "Holding the increase in the global average temperatures to well below 2OC above pre-industrial levels and pursuing efforts to limit the temperature increase to 1.5OC ...".

2. With capacity to generate demand for electrical energy in the US State of Texas.

3. The EU ETS requires each liable entity to surrender in respect of each year a number of emissions permits equal to the GHG emissions arising from activities of that liable entity during that year. Emissions permits are acquired either through the primary market under which emissions permits are auctioned or through the secondary market on which emissions permits are traded.

4. Carbon leakage occurs if (for reasons of costs and expenses related to climate change policies), businesses transfer production to other countries or import from other countries that do not have climate change policies consistent with those of the EU, critically, a price on carbon.

5. By way of reminder, Article 2.1(a) of the Paris Agreement provides for "Holding the increase in the global average temperatures to well below 2OC above pre-industrial levels and pursuing efforts to limit the temperature increase to 1.5OC ...".

6. Australia, Bangladesh, Brazil, Chile, Ghana, Hong Kong SAR, Jordan, Kenya, Malaysia, Mexico, Nigeria, Pakistan, Sri Lanka, Chinese Taipei (Taiwan), Tanzania, Türkiye, the UK, and Zambia.

7. Including the Accounting Regulatory Committee, and eight EU agencies and bodies, including the ECB, EBA and ESMA.

8. The official financing sector is a reference to state-owned or state-directed institutions that provide financing or investment outside China in support of national economic, industrial and diplomatic objectives of China, being in public ownership and having policy alignment.

9. From a policy perspective the EU Taxonomy is intended to guide investment to economic activities most needed for decarbonization and the energy transition.

10. The European Hydrogen Bank (EHB) is a means to develop a hydrogen value chain. The EHB is intended to provide support to the private sector as a result of which renewable hydrogen will be produced sooner than might otherwise have been the case.

11. CM3 are: 1. Bauxite, High Purity Alumina, and Aluminum; 2. Antimony; 3. Beryllium; 4. Bismuth; 5. Cobalt; 6. Copper; 7. Gallium; 8. Germanium; 9. Graphite; 10. Indium; 11. Lithium; 12. Magnesium; 13. Manganese; 14. Nickel; 15. Niobium; 16. Platinum metals; 17. Rare Earths Elements (REEs); 18. Silicon and Silicon metals; 19. Tantalum; 20. Titanium and Titanium metal; 21. Tungsten; 22. Uranium; and, 23. Vanadium.

12. REEs are: 1. Cerium (Ce); 2. Dysprosium (Dy); 3. Erbium (Er); 4. Europium (Eu); 5. Gadolinium (Gd); 6. Holmium (Ho); 7. Lanthanum (La); 8. Lutetium (Lu); 9. Neodymium (Nd); 10. Praseodymium (Pr); 11. Promethium (Pm); 12. Samarium (Sm); 13. Scandium (Sc); 14. Terbium (Tb); 15. Thulium (Tm); 16. Ytterbium (Yb); and 17. Yttrium (Y).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.