The Washington Department of Revenue (Department) has announced a temporary penalty relief program for businesses that did not collect or remit retail sales or use tax on certain services that became taxable on Oct. 1, 2025, under Engrossed Substitute Senate Bill 5814 (ESSB 5814).

The Department acknowledged the challenges associated with the transition to ESSB 5814 and will consider waiving certain penalties related to uncollected retail sales tax and unpaid use tax attributable to the statutory changes. The relief applies to reporting periods from Oct. 1, 2025, through Dec. 31, 2026.

Background – Expansion of Retail Sales Tax to Certain Services

During the 2025 legislative session, the Washington Legislature enacted ESSB 5814, which expanded the retail sales and use tax to include certain services that were previously not taxable. The legislation also repealed several exclusions related to digital automated services.

Because the standard rulemaking process was not completed prior to the Oct. 1, 2025, effective date, the Department issued interim guidance addressing the scope and application of the new services. The following table summarizes the seven categories of services that became subject to tax as of Oct. 1, 2025, along with inclusions and exclusions summarized by the Department.

|

Service Category |

Inclusions |

Exclusions |

|

Advertising Services |

Ad design, ad placement, campaign planning, lead generation, and acquisition of internet advertising space. |

Web hosting, domain registration, certain newspaper/in-print advertising, radio/TV ads, fixed signage, and out-of-home ads. |

|

Information Technology (IT) |

Help desk services, network support, training, IT consulting, data processing, and data entry. |

Web hosting, domain registration, and payment processing. |

|

Custom Website Development |

Website design, development, and technical support. |

Web hosting and domain registration services. |

|

Live Presentations |

In-person or internet-based workshops, webinars, and courses featuring real-time interaction. |

Preschool, K-12/higher education as part of their accreditation, performances, sports events, and tutoring. |

|

Security & Investigation |

Security guards, background checks, armored car services, investigation, and security systems services. |

Locksmith services. |

|

Temporary Staffing |

Supplying workers to businesses under contract or for short-term assignments. |

Hospital staffing, direct hires, independent contractors, paymaster services, and third-party outsourcing services. |

|

Custom Software |

Access to and use of custom software; customization of prewritten software. |

Unmodified “off-the-shelf” software. |

Digital Automated Services

ESSB 5814 also modified the tax treatment of digital automated services. The legislation removed prior exclusions for advertising, live presentations, and data processing services. In addition, the exclusion for services provided primarily through human effort was repealed.

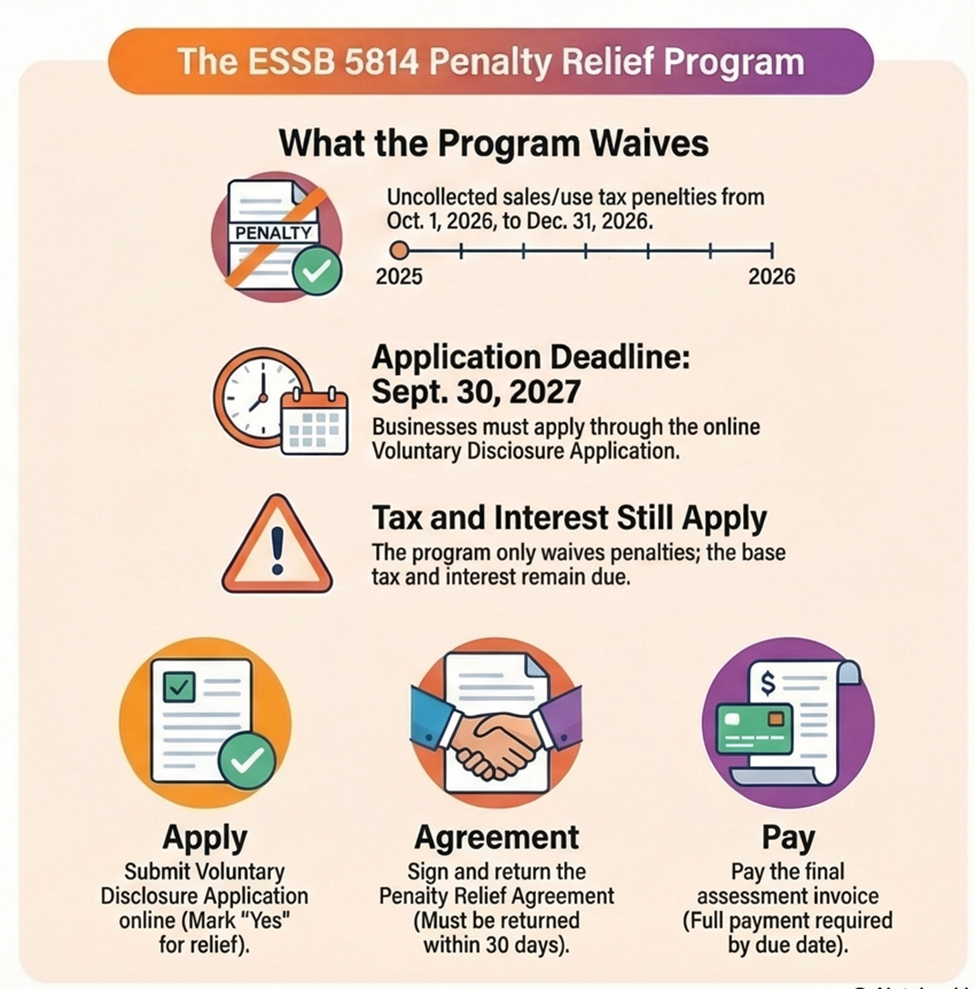

The Penalty Relief Program—Scope and Eligibility

Under the 5814 Penalty Relief Program, the Department will consider waiving certain penalties for businesses that voluntarily report and pay retail sales and use taxes for these services that became taxable under ESSB 5814 changes.

Key Program Parameters

- Eligible Reporting Periods: Transactions occurring from Oct. 1, 2025, through Dec. 31, 2026.

- Applicable Taxes: Relief applies only to uncollected retail sales tax and unpaid use tax resulting from ESSB 5814 changes.

- Penalties Only: The program waives penalties only. The underlying tax and all accrued interest remain due.

- Application Deadline: Applications are due by Sept. 30, 2027, and application are reviewed in the order received.

- Agreement Requirement: Approved applicants receive a Penalty Relief Agreement that must be signed and returned within 30 days.

Additional Eligibility Considerations

- Unregistered businesses: The Department has indicated that unregistered businesses should review eligibility under the separate Voluntary Disclosure Program before applying for penalty relief under this program.

- Good Faith Errors: The program applies to good-faith compliance errors. Penalties related to evasion, negligence, or tax avoidance are expressly excluded.

- Preexisting Contract Nuance: For contracts that qualified for temporary preexisting contract relief, the penalty relief period begins only when the contract no longer qualifies or on April 1, 2026, whichever occurs first, and runs through Dec. 31, 2026.1

Application Process

Penalty relief applications are submitted through the Department’s online Voluntary Disclosure Application. The process generally includes the following steps:

- Submission: Completion of the Department’s online Voluntary Disclosure Application, including entry of a UBI number of Account ID if available.

- Program Designation: Selection of “Yes” in response to the question: “Are you applying for penalty relief related to sales tax changes in ESSB 5814 (2025)?”

- Penalty Relief Agreement: If the application is approved, the Department issues a Penalty Relief Agreement for signature.

- Return Deadline: The signed agreement is due within 30 days of issuance. Agreements not returned within this timeframe are not approved.

- Examination: Following countersignature by the Department, an examiner may request additional information to determine the tax liability.

- Draft Assessment: The Department prepares a draft assessment reflecting tax, interest, and any penalties not eligible for waiver. The applicant has an opportunity to review this draft before finalization.

- Final Invoice: A final invoice is posted to the applicant’s My DOR account.

- Full payment: Payment is due by the date listed on the invoice. Additional interest and late penalties may accrue if payment is not made by that date.

The Department has stated that information submitted as part of the application and any executed Penalty Relief Agreement is treated as confidential in accordance with RCW 82.32.330.

Additional Relief for International Remote Sellers

The Department is also administering a temporary International Remote Seller Voluntary Disclosure Program. This program began on Feb. 1, 2026, and runs through May 31, 2026. It provides certain foreign businesses with shortened lookback periods and penalty relief. International businesses may evaluate participation in this program before the amnesty period concludes. For additional information on the amnesty program see our November 2025 GT Alert.

Footnote

1 The Department’s interim guidance provided transitional relief for certain contracts signed and executed before Oct. 1, 2025. Under this guidance, certain contracts may continue under pre-ESSB 5814 treatment through March 31, 2026. Any material change to an existing contract after Oct. 1, 2025 (scope, price, extension, substitution) removes the contract from this relief. Wash. Dep’t of Revenue, Interim Guidance Regarding Contracts Existing Prior to October 1, 2025 (last visited March 16, 2026).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]