- within Tax topic(s)

- in South America

- within Litigation, Mediation & Arbitration, Technology and Real Estate and Construction topic(s)

Summary

The Macau Special Administrative Region of the People's Republic of China ("Macau SAR") government officially issued the "Implementation Rules for Transfer Pricing" (Administrative Regulation No. 11/2025) on August 25, 2025 (hereinafter referred to as "the Implementation Rules"). The rules further refine Macau SAR's transfer pricing regulations, aiming to improve transparency and align local tax laws with international anti-tax avoidance standards. The Implementation Rules directly affect transfer pricing arrangements between Macau SAR taxpayers and their related parties. They took effect on 1 January 2026 and apply to all controlled related-party transactions from that date.

Background

On December 16, 2024, the Macau SAR government introduced a transfer pricing regime through the passage of the "Approval of the Tax Code" bill (hereinafter referred to as "the Tax Code"), clarifying the concept of transfer pricing and the principle of related-party transactions, and requiring that transactions between taxpayers in Macau SAR and their related parties in other tax jurisdictions should comply with the arm's length principle.

To implement the provisions on transfer pricing in the Tax Code and the Supplementary Tax Regulations, the Macau SAR government published the Implementation Rules in the form of an administrative regulation on August 25, 2025. These rules provide detailed and specific guidelines on the application of the arm's length principle, methods for transfer pricing adjustments, requirements for the retention of controlled transaction documentation (i.e., transfer pricing compliance documents), and Advance Pricing Arrangement (hereinafter referred to as "APA"). The issuance of the Implementation Rules is significant for guiding the Macau SAR Finance Bureau and taxpayers in implementing transfer pricing administration, including compliance reporting of related party transactions, application of transfer pricing methods, assessment and adjustment of controlled transactions, and the application, negotiation and supervision over APAs.

Key focus

I. Types of controlled transactions and definitions of related party relationships

The Implementation Rules further clarify the application scope of Macau SAR's transfer pricing regulations, including the categories of related party transactions and the definition of related party relationships.

- Types of controlled transactions - Based on Article 43-A of the Complementary Tax Regulations, the transfer pricing regulations apply to commercial or financial transactions between taxpayers in Macau SAR and related parties in other tax jurisdictions. These include: 1) commercial transactions involving tangible or intangible assets, rights, or services; 2) financial transactions (including loans, centralized fund management, hedge funds, guarantees, insurance, etc.); 3) Business reorganizations or restructuring transactions (including asset transfers or compensations). Transactions between associated taxpayers within Macau SAR are not subject to transfer pricing regulations.

- Related party relationships - Based on Article 43-B of the Complementary Tax Regulations, the Implementation Rules define eight scenarios that constitute related party relationships, including entities or individuals with direct or indirect ownership or voting rights of 50% or more, appointments of directors or administrative management members, spousal or direct bloodline relationships, and other substantial control relationships. These definitions provide clearer guidance for practical operations (Detailed categories of related-party relationships can be referenced in the appendix).

II. Transfer Pricing Methods and analysis procedures

In accordance with the "arm's length principle", the Implementation Rules supplement the principles for analyzing controlled transactions and the application details of transfer pricing methods. It clearly defines the requirements for comparable transactions and comparability analysis, as well as relevant necessary adjustments. Additionally, the Implementation Rules explicitly state that the Finance Bureau should use comparability analysis procedures to assess the reasonableness of controlled transactions by taxpayers, providing detailed guidance for the Finance Bureau to adjust taxpayers' taxable base using an "indirect assessment method." The Implementation Rules also address how to resolve double taxation issues arising from cross-border controlled transactions and relevant application processes.

- Principles for analyzing controlled transactions - Each controlled transaction must be analyzed individually under the arm's length principle. The combined analysis of two or more related-party transactions only applies to situations where 1) related-party transactions are highly integrated and separate analysis of them will result in the loss of commercial function and value, 2) involve high costs, and 3) there are no comparable transactions, and it is difficult to determine the transaction value.

- Definition of comparable transactions - When comparing non-controlled comparable transactions with controlled transactions, the conditions include: 1) the transactions are substantially similar in economic characteristics; 2) differences between the transactions or the entities involved do not significantly affect the terms and conditions that would be reached, accepted, and implemented in normal market conditions (even if they do, such differences can be effectively adjusted to eliminate their impact). Taxpayers need to analyze the facts and circumstances of each transaction to determine the substantive impact of economic characteristic differences on comparability indicators and the adjustments needed to eliminate such impacts.

- Comparability analysis and comparability factors - Before determining the applicable transfer pricing method, taxpayers must conduct a comparability analysis, including accurately defining the controlled transaction, identifying and comparing the terms, conditions, and relevant economic characteristics of the controlled transaction and non-related comparable transactions, and ensuring that the comparability analysis is based on the actual execution terms and conditions of the controlled transaction. The Implementation Rules list key factors to consider in comparability analysis, including: 1) the characteristics of the assets, rights, or services involved in the transaction that may potentially affect the transaction price; 2) the functions performed, risks assumed, and assets used by the entities involved in the transaction; 3) contractual terms and conditions explicitly or implicitly setting out the responsibilities, risks, and profit allocation among the parties; 4) the economic environment of the markets in which the parties operate; 5) operational strategies that may affect normal business behavior and operations; and 6) other relevant important features, such as the influence of public policy decisions, the existence of regional or synergistic advantages, etc. The Implementation Rules require taxpayers to make comparability adjustments according to the rules to eliminate substantial differences between controlled and non-controlled transactions, enhancing the reliability of comparability analysis.

- Comparability analysis procedures and most appropriate Transfer Pricing Methods - Comparability analysis procedures should broadly analyse the business background of the transacting parties, including the transaction period, business context, functions, risks, and asset situations undertaken by the parties, and select the most appropriate transfer pricing method and indicators, making comparability adjustments when appropriate. Regarding the transfer pricing methods listed in Article 43-E of the Complementary Tax Regulations, the Implementation Rules provide detailed specifications of the specific application conditions, calculation formulas, and financial indicators for various methods, including the Comparable Uncontrolled Price Method, Resale Price Method, Cost Plus Method, Transaction Profit Split Method or Transaction Net Margin Method, and other methods that better reflect the alignment between profits and the jurisdictions where economic activities and value creation occurred. At the same time, the Implementation Rules specify that the most appropriate transfer pricing method should provide the best and most reliable estimation of the terms and conditions that would be agreed under an arm's length situation, providing the highest quality and quantity of comparable data in comparisons, and involving the least amount of comparability adjustments. The Macau SAR Finance Bureau will verify whether the controlled transactions between taxpayers and their related parties comply with the arm's length principle through comparability analysis procedures. If non-compliance is discovered, the Finance Bureau may adjust the taxpayer's taxable base according to Article 43-C, Paragraph 1 of the Complementary Tax Regulations, using the aforementioned transfer pricing methods and an "indirect assessment method".

The Finance Bureau's transfer pricing adjustment of the taxable base will follow two key rules:

- Use of Quartile Statistical Method and Median Value Standard: Based on the average range of comparable transaction prices or profits over the past three years, the median value is selected using the quartile statistical method. If the controlled transaction price or profit is below the median value, it needs to be adjusted to at least the median level to ensure that the transaction price is consistent with the comparable level of independent third-party transactions.

- Adjustment period attribution: The results of the taxable base adjustment should be attributed to one or more tax years affected by the controlled transaction to avoid confusion across tax years.

To address potential double taxation issues arising from cross-border controlled transactions, the Implementation Rules propose two resolution paths and related application procedures for taxpayers:

- Corresponding adjustment mechanism: If the Macau SAR has signed an agreement or treaty to avoid double taxation with another tax jurisdiction, the Finance Bureau may assess the actual transaction details and decide whether to make corresponding adjustments to the taxpayer's taxable base in light of adjustments made by the related party's tax jurisdiction.

- Mutual agreement procedure application: If a foreign tax authority has already adjusted the related party's taxable base or decided to initiate an audit procedure, the taxpayer may submit a written application to the Macau SAR Finance Bureau to start the mutual agreement procedure. The application must include complete identification information of the taxpayer entity and its related parties, a description of the transaction details, the involved tax period, relevant legal provisions, and measures taken to resolve disputes. The Finance Bureau will complete an initial analysis within 30 days of receiving the written application and work in tandem with the foreign tax authority.

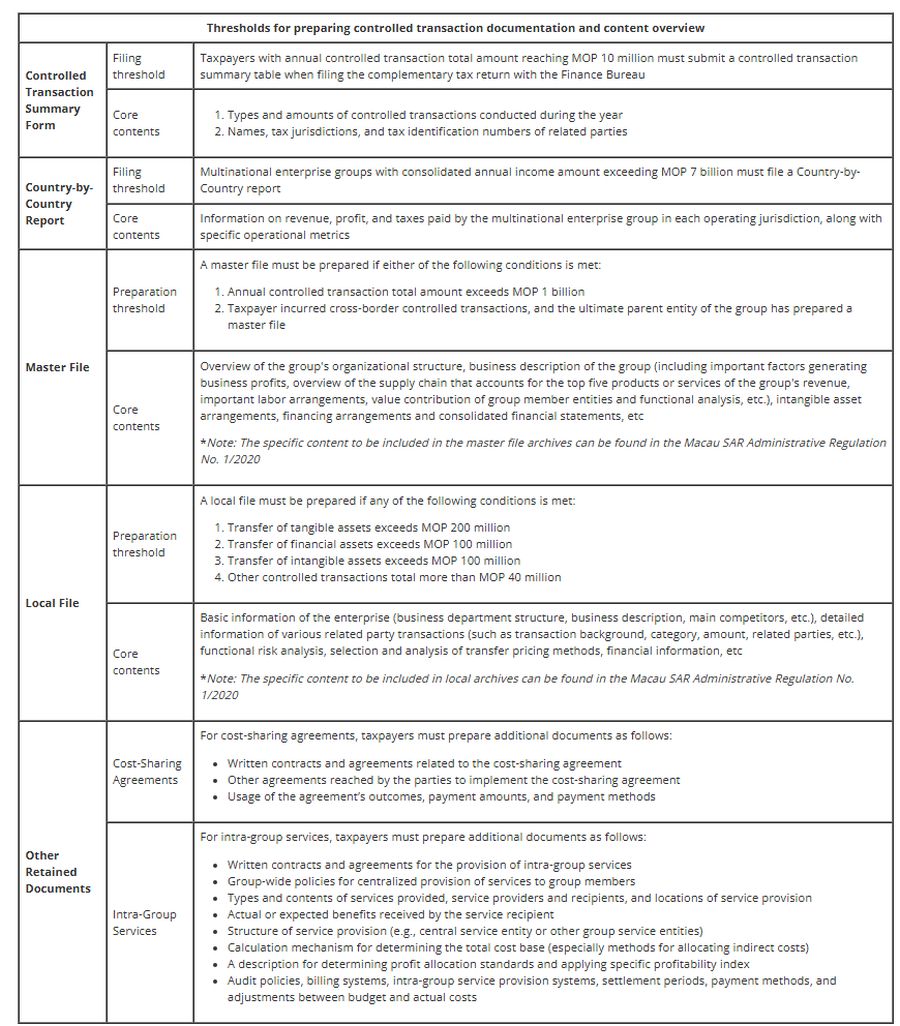

III. Compliance reporting and documentation requirements for controlled transactions

According to Article 43-D of the Complementary Tax Regulations, the Implementation Rules establish a structured framework for the preparation, maintenance, and submission of annual controlled transaction documentation, organized in a tiered manner. They specify retention periods and submission requirements, including detailed guidelines for taxpayers. Based on the annual transaction volume and type, taxpayers must organize and prepare the required documentation accordingly. Additionally, taxpayers may be exempt from certain retention obligations if specific thresholds are not exceeded.

1. Thresholds for preparing controlled transaction documentation

2. Preservation periods and submission requirements

- Preparation deadline and language requirements: Taxpayers should retain all important documents related to transfer pricing within 9 months after the end of each fiscal year. If the submitted documents are not in any of the official languages (Chinese or Portuguese), a translation must be provided unless the Finance Bureau confirms that the original language content can be directly understood. If the Finance Bureau requests the provision of controlled transaction documentation, it should be submitted within 15 days.

- Preservation period: All controlled transaction documentation must be retained for 7 years from the end of the fiscal year and must be complete and traceable during this period. In cases of mergers or spin-offs, the responsibility for retention will be assumed by the entity resulting from the merger or spin-off.

- Consequences of Non-compliance: Failure to properly retain or submit the required documentation may result in fines ranging from MOP 10,000 to MOP 100,000. For intentional non-compliance, fines can be increased to MOP 100,000 to MOP 200,000.

IV. Advance Pricing Arrangements (APAs)

The Macau SAR introduced the APA mechanism for the first time in the Complementary Tax Regulations. Taxpayers with annual controlled transaction amounts exceeding MOP 40 million can apply to the Finance Bureau for APAs covering future controlled transactions. The Implementation Rules further detail the application and execution procedures for unilateral APAs, allowing taxpayers to obtain future tax certainty by entering into APAs with the Finance Bureau and thereby reducing the risk of future transfer pricing adjustments.

1. Scope and duration of APAs

- Applicable transactions: APAs apply to transactions between taxpayers and the Finance Bureau. The Finance Bureau retains the right to adjust and monitor controlled transactions that fall outside the scope of the APA.

- Duration: The maximum validity period for an APA is 5 years. Taxpayers may request retroactive application to up to 2 previous tax years prior to the signing of the arrangement, provided that the tax basis for those years has not yet been determined.

2. Application process and fees

- The application process for APAs consists of three

stages:

- Application stage: Taxpayers must submit an application to the Finance Bureau along with relevant documentation, including the proposed APA period, details of related parties and controlled transactions, organizational and management structures of the taxpayer and its group, recent five-year business operation descriptions, financial accounting and audit reports, descriptions of functions and risks of taxpayer and its related parties, proposed transfer pricing methods, value chain analyses, market situation explanations, projected scale of operations and revenues for the APA applied years, industry-related laws and regulations both domestically and internationally, etc.

- Analysis and evaluation stage: The Finance Bureau will analyze the function and risk profiles of the controlled transactions covered by the APA, comparable and controlled transactions data, pricing and calculation methods, value chain contributions, price or profit standards, assumptions, and intentions for retroactive application to past years.

- Negotiation and signing stage: The content of the APA will be formulated based on the consensus reached between the Finance Bureau and the taxpayer during the negotiation process. The text should clearly define the taxpayer and related parties covered by the APA, the applicable years, pricing and calculation methods, definitions of terms related to method applicability and calculation basis, notification obligations for changes in assumptions, annual report submission obligations, terms and conditions for fulfilling the APA, duration of the APA, circumstances leading to its modification or termination, etc.

- If a taxpayer has been fined for tax violations in the past three years, failed to maintain necessary transaction records, or if the application does not comply with the arm's length principle, the Finance Bureau has the authority to reject the application. If a taxpayer or its related party fails to provide necessary data for evaluating the APA, provides false or incomplete data, or otherwise fails to cooperate, the Finance Bureau may suspend or terminate the APA negotiation process. If a taxpayer requests suspension or termination of the APA negotiation process, they must submit a written application and explanation to the Finance Bureau.

- Fees: The application fee for each APA is calculated at 2% of the transaction amount, capped at a maximum of MOP 200,000. If the Finance Bureau confirms that the taxpayer's APA application complies with the arm's length principle, the taxpayer will be notified to pay the fee within 60 days. Once paid, the fee is non-refundable.

3. Execution and supervision of APAs

- Annual reporting obligation: If a taxpayer signs an APA, they are exempt from preparing the local file for the involved controlled transactions covered by the APA. However, the taxpayer must submit an annual report to the Finance Bureau within seven months after the end of each tax year, detailing the taxpayer's actual business operations, the validity of assumptions, and compliance with the APA terms. If there are substantial changes affecting the APA (such as changes in transaction models or significant shifts in market conditions), the taxpayer must submit a written report to the Finance Bureau within 30 days of the change.

- Termination and renewal: An APA automatically expires upon the expiration of its term. A taxpayer may apply for renewal 90 days before the expiration date, submitting the latest implementation report and future annual transaction forecasts. If a taxpayer submits false information or fails to comply with the APA terms, the Finance Bureau has the authority to revoke the APA and recalculate the tax base according to transfer pricing adjustment

V. Special considerations for certain specific transactions

The Implementation Rules provide special considerations and guidelines for cost-sharing agreements, intra-group service arrangements, intangible asset transactions, business restructurings, and financial financing transactions. These provisions align with the fundamental principles of the OECD Transfer Pricing Guidelines. Below are key points regarding commonly occurring intra-group service transactions and intangible asset transactions:

1. Intra-Group Services

- Intra-group services provided by related parties (including administrative, technical, financial, or commercial activities) shall comply with the arm's length principle. The taxpayer must ensure that the related-party services are beneficial, and that the payment or receipt complies with the arm's length principle. The Implementation Rules also specify three scenarios where services are considered non-beneficial, including: 1) shareholder services, 2) repetitive services, and 3) services that only benefit the entity by virtue of being part of the group.

- The value of benefits generated by related-party services can be determined using the Comparable Uncontrolled Price Method or the Cost Plus Method. The profit margin for the service provider should consider factors such as economic alternatives available to the service recipient, the nature of the service activity, efficiency and quality, the importance of the service activity to the group, and the advantages it confers. If the service provider acts solely as a pass-through agent for the group in obtaining services from third parties, the service fee paid to the service provider may exclude a profit margin.

- When determining service prices, direct methods should be used, i.e., setting specific price for each type of service contract given that it could be separately identified and quantified. If direct methods cannot be applied, indirect methods should be used, allocating costs based on appropriate allocation key corresponding to the value of services received by each member. Allocation key should reasonably reflect the nature and use of the services, particularly considering sales volume, gross margin, personnel expenses, production and sales expenses.

2. Intangible asset transactions

- Definition of intangible assets - The Implementing Regulations specify that intangible assets involved in controlled transactions are non-tangible forms that can be held or controlled for use in an activity. These provisions apply to non-financial assets that would require compensation if transactions were to occur between non-related parties.

- Alignment of economic activities and value contributions - The independent transaction price for controlled transactions involving intangible assets should be determined based on the contribution created by the functions performed, assets used, and risks borne by related parties in the development, enhancement, maintenance, protection, and exploitation (DEMPE) of the intangible assets.

- Identification of contractual terms - Identify legal conditions and terms related to the statutory holder of the intangible asset and contractual terms specifying the rights, obligations, and risk allocations among the parties. Assess whether the terms of the contract align with the behavior of the entities involved, especially whether the entity bearing significant economic risks controls and has the financial capacity to bear related risks of DEMPE activities.

- Limited remuneration for related parties only providing financing funds - For related parties (including intangible asset legal rights holders) who do not assume any significant economic risks related to the transaction and only provide financing funds, the reasonable cost of funding remuneration obtained by them shall not exceed the risk-free interest rate (in the absence of financial capability or control of significant economic risks related to financing) or the adjusted interest rate according to the risk it bears (in the case of having financial capability and controlling significant economic risks related to financing).

KPMG Observations and Recommendations

Building upon the Tax Code enacted at the end of last year, the Implementation Rules provide more detailed and systematic requirements for transfer pricing regulations in Macau SAR. KPMG particularly reminds multinational enterprise groups currently operating or planning to operate in Macau SAR to pay close attention to the following transfer pricing-related matters:

- Enterprises should promptly conduct a comprehensive review of transfer pricing arrangements involving subsidiaries or branches in Macau SAR, identify any potential risks in light of the latest regulations, and take appropriate steps to address and optimize these arrangements to ensure ongoing tax compliance under the new rules.

- Enterprises should pay close attention to the declaration and document preparation requirements for controlled related-party transactions in Macau SAR, especially the new declaration requirements for the Controlled Transaction Summary Form in the Implementation Rules, and the detailed provisions for the preparation threshold of master file and local file. If the amount of controlled transactions in 2026 and subsequent years reaches the preparation threshold, the enterprise shall complete the filing and document preparation of related-party transactions on time according to regulations.

- The transfer pricing regulations of the Macau SAR generally refer to the relevant regulations and requirements of mainland China, Hong Kong SAR, and OECD transfer pricing guidelines. Among them, the Implementation Rules have made more detailed provisions on the evaluation methods and compliance requirements for transfer pricing comparability analysis, service transaction within the group, intangible asset transactions, etc. Enterprises with relevant arrangements for controlled transactions in the Macau SAR should comply with the detailed considerations and requirements in the regulations regarding the authenticity, profitability, and reasonableness of service transactions within the group, as well as the pricing scheme for intangible asset transactions, taking into account each party's profit return and functional profile of DEMPE (Development, Enhancement, Maintenance, Protection, and Exploitation) activities.

- Enterprises with large-scale cross-border related transactions and stable transaction models can explore the feasibility of applying for and negotiating APAs with the Macau SAR Finance Bureau to achieve certainty in future tax arrangements. Although the Implementation Rules currently only introduce unilateral APA negotiation mechanisms, KPMG will continue to monitor whether bilateral APA mechanisms may be introduced in Macau SAR in the future.

In summary, the issuance of the Implementation Rules marks a new stage in the development of Macau SAR's transfer pricing system. These rules not only clarify the specific requirements of the transfer pricing rules in the Tax Code but also achieve alignment with international tax systems. They also demonstrate Macau SAR's commitment to creating a more favorable investment business environment and standardized, transparent tax regulatory environment. We note that the Macau SAR Finance Bureau maintains close communication and cooperation with tax authorities in Mainland China and Hong Kong SAR in tax administration practices. The revision and improvement of Macau SAR's transfer pricing system fully absorb the experience and implementation of transfer pricing regulations and policies in Mainland China and Hong Kong SAR, showcasing Macau SAR's proactive attitude in integrating into the national-level major strategy of building the Guangdong-Hong Kong-Macau SAR Greater Bay Area in terms of tax system construction and tax cooperation.

If you need to further understand or explore the transfer pricing regulations and practical requirements of the Macau SAR, please feel free to contact KPMG professionals or institutions at any time. We are committed to providing you with comprehensive professional support.

Appendix: Detailed categories of related-party relationships of the Implementation Rules

| Category | Related-party relationship |

| 1 | One entity or its shareholder, or the spouse or lineal relative of such shareholder, directly or indirectly holds at least 50% of the equity interest or voting rights in another entity |

| 2 | Multiple entities have the same equity holder, and such equity holder, their spouse, or lineal relatives directly or indirectly jointly hold at least 50% of the equity interest or voting rights in another entity |

| 3 | More than half of the administrative management members, directors, or managers of one entity are appointed or assigned by another entity, or more than half of the administrative management members, directors, or managers of both entities are appointed or assigned by the same third-party entity |

| 4 | If personnel of one entity have a marital relationship or lineal kinship with the administrative management members, directors, or managers of another entity, and both entities have substantial control over their respective entities, such personnel shall be deemed to have the same status as the appointed individuals |

| 5 | One entity's business operations requiring a franchise granted by another entity to operate normally, provided that the two entities have any of the relationships referred to above mentioned (1) or (2), even if the equity interest or voting rights are below 50% |

| 6 | One entity's acquisition and sale of property or provision and receipt of services being controlled by another entity, which has the authority to determine the financial and operational policies of the former and derive benefits from its operations |

| 7 | The controlling shareholder of one entity holding a majority stake in the company's capital alone, or together with other companies where they are also controlling shareholders, or through agreements resembling company agreements, or holding more than 50% of the voting rights, or having the right to elect a majority of the administrative management body members, whether as a natural person or legal entity |

| 8 | Other circumstances where one entity is directly or indirectly influenced by another entity, resulting in terms and conditions agreed upon, accepted, and implemented in transactions between the two entities differing from those that would be adopted in comparable transactions between non-associated parties |

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]