- in Canada

- within Wealth Management, Employment and HR and Technology topic(s)

- with Senior Company Executives, HR and Finance and Tax Executives

- with readers working within the Law Firm industries

This snapshot summarises the key developments and issues

which have arisen over the last 12 months and which UK-incorporated

listed companies should have on their radar when preparing their

annual report to be published in 2026 and for their 2026 annual

general meeting (AGM). It also considers the status of various

ongoing reform programmes relating to shareholder engagement and

corporate governance.

1. The annual report in 2026

For companies with a 31 December year-end, there are only minor changes which need to be reflected in the annual report and accounts (ARA) in 2026, notably the transition to reporting under the 2024 edition of the UK Corporate Governance Code (2024 Governance Code, or Code where any edition is being referred to) and the application of the increased financial thresholds for the classification of companies.

- The 2024 Governance Code

In January 2024, the Financial Reporting Council (FRC) published the 2024 Governance Code (see our snapshot here for a summary of the changes introduced by the FRC). The 2024 Governance Code applies to financial years beginning on or after 1 January 2025, with the exception of Provision 29 on internal controls reporting (which applies from financial years beginning on or after 1 January 2026). Accordingly, many companies will be reporting against the 2024 Governance Code for the first time in 2026.

For the most part, the changes introduced by the FRC in the 2024 Governance Code are not substantial and so there will be relatively few amendments needed to reflect the transition to the new edition of the Code. Close attention to detail will be needed to ensure however that the changes introduced are correctly reflected. For example, reference should be made to how the desired culture has been "embedded" in addition to how the board has assessed and monitored culture. Also, with the introduction of new Principle C, as an overarching approach the reporting should focus on the outcomes of board decisions in the context of the company's strategy and objectives.

The FRC's Audit Committee and the External Audit Minimum Standard (Minimum Standard), which was published in May 2023 and applied from that date to FTSE 350 companies, is now expressly referred to in the 2024 Governance Code and so applies to all companies applying the 2024 Governance Code. The Minimum Standard sets out certain disclosures on the work of the audit committee to be included in the annual report, in particular in relation to auditor independence and quality, and audit tenders, so companies should ensure that these disclosures are duly incorporated in their ARA.

As noted above, more substantial reporting changes will be needed in 2027 to reflect Provision 29 of the 2024 Governance Code, which requires boards to include more fulsome disclosures on the monitoring and effectiveness of the company's material controls. Companies may wish to signpost their progress in relation to readiness to comply with Provision 29 next year and ensure that they have in place the necessary processes and procedures in place to make the more fulsome disclosures in due course in their ARA to be published in 2027.

- FRC guidance

In November 2025, the FRC published its annual report of corporate governance reporting for 2025, which discusses the quality of reporting against the Code (see our blog post here). As noted above, the 2024 Governance Code applies to financial year beginning on or after 1 January 2025, so this report is the last in which the FRC will look at reporting against the 2018 edition of the Code. More than half the companies reviewed referred to the new Provision 29 in their annual report, with many including details on how they are preparing for it applying from financial years beginning on or after 1 January 2026.

In September 2025, the FRC published its annual review of wider corporate reporting (see our blog post here). The review observed a continued quality gap between reporting by FTSE 350 companies and other companies (see below on the FRC's thematic review on reporting by smaller listed companies). For the second year in a row, climate-related reporting issues appeared in the top ten most common issues on which the FRC asked companies substantive questions, requiring further information or explanations to understand disclosures in their annual report.

Other papers published by the FRC during 2025 include:

- a thematic review of reporting by smaller listed companies which focused on the four areas in relation to which substantive letters are most commonly sent to smaller listed companies - namely revenue, cash flow statements, impairment of non-financial assets and financial instruments (see our blog post here);

- a thematic review of climate-related disclosures by AIM and large private companies (ie those not within the UK Listing Rules (UKLRs) Task Force on Climate-related Financial Disclosures (TCFD) reporting regime) (see our blog post here);

- updated going concern guidance following the consultation it conducted on changes to the guidance in 2024 (see our blog post here); and

- a review of structured digital reporting, with recommendations

for companies on best practice (see our blog post

here). On a related note, companies should ensure that

any regulated information submitted for filing at the National

Storage Mechanism (NSM) complies with the

requirements introduced by the Financial Conduct Authority

(FCA) in November 2025 to enhance the NSM, for

example the need to include a company's LEI number on every RIS

announcement (see our blog post

here).

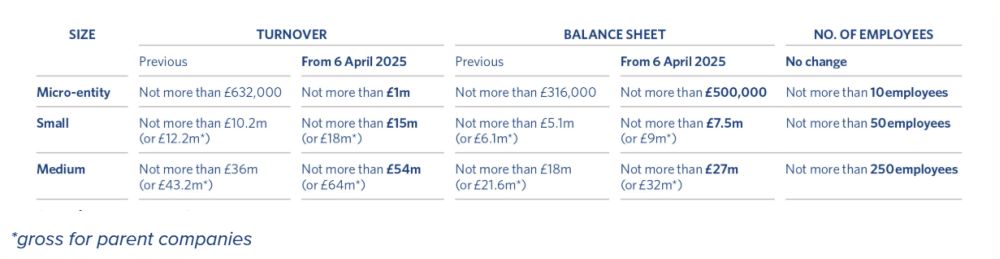

- Increased financial thresholds for company

classification

Under the Companies Act 2006 (CA 2006), whether companies need to include certain disclosures in their annual report will depend in part on whether they meet certain size thresholds set out in the CA 2006. There are three criteria used when assessing a company's size for the purposes of these thresholds - turnover, balance sheet and the number of employees - and four different size classifications – micro-entity, small, medium or large. If a company satisfies two or more of the three criteria for a particular classification, then it will qualify for that classification.

The financial criteria (ie, turnover and balance sheet) for each of the size classifications, other than "large", were increased with effect from 6 April 2025 and these revised thresholds apply when considering any previous financial year. The revised thresholds are summarised in the table below. As a result, companies may find that entities within their groups no longer fall within the remit of certain reporting requirements and should adjust the disclosures made accordingly.

2. The AGM in 2026

There are no new resolutions which need to be put to shareholders at the AGM in 2026, nor are there any major developments which will impact on the preparation for, or running of, the 2026 AGM. There are however some issues which those involved in the company's AGM should be aware of:

- Updated proxy voting guidelines: The

ISS, Pensions UK (formerly the PLSA) and Glass Lewis have all

published updates to their proxy voting guidelines (see our blog

posts

here,

here and

here). The updated guidelines all include expanded commentary

on virtual-only shareholder meetings, which should be kept in mind

when details of the government's proposals to clarify the

provisions of the CA 2006 relating to such meetings are published

(see further below), as well as other issues including board

diversity, board committee composition and cybersecurity.

- Pre-Emption Group Guidelines: the third

annual monitoring report on the use of the revised November 2022

Pre-Emption Group's Statement of Principles

(Principles) on the disapplication of pre-emption

rights was published in November 2025. The review covered the

adoption of the Principles by FTSE 100 and FTSE 250 companies at

meetings held between 1 August 2024 and 31 July 2025. The key

findings include:

- 77.6% of FTSE 350 companies that put forward resolutions to disapply pre-emption rights sought 'enhanced' disapplication authorities as permitted under the Principles (an increase from 67.1% in 2024 and 55.7% in 2023) – enhanced authority refers to a disapplication request where either the request for general corporate purposes, or the request for a specified capital investment, or both, exceeds the 5% authority previously allowed under the 2015 Statement of Principles; and

- 99.1% of the disapplication resolutions were passed, with 72.6%

of disapplication resolutions for general corporate purposes passed

with less than 5% of votes against.

The findings suggest that the market has adapted to, and accepted companies taking advantage of, the enhanced disapplication authorities permitted under the Principles, though see the box below on the impact of the reforms to the UK prospectus regime with effect from 19 January 2026.

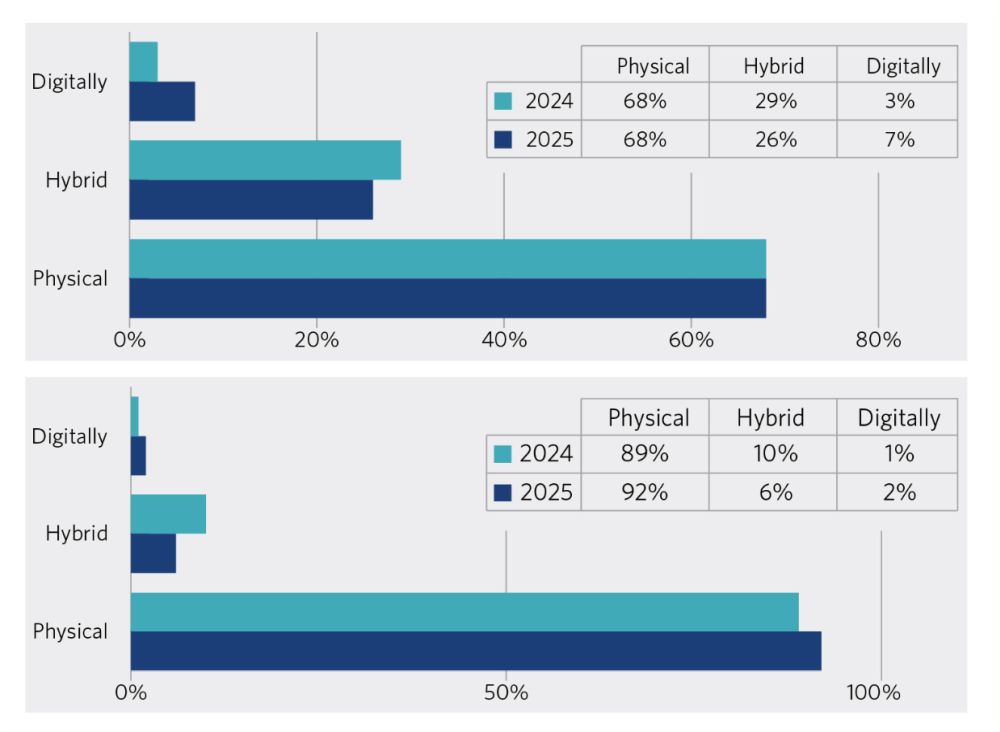

- Meeting format: As illustrated by the

charts below, the format adopted by FTSE 100 and FTSE 250 companies

for their AGMs remained broadly the same in 2025 as in previous

years, though there was a small increase in digitally-enabled

AGMs.

Following the government's commitment in October 2024 to look at the legality of virtual-only shareholder meetings, it is not surprising that there has been increased attention and debate surrounding this type of meeting format. As noted above, the ISS, Glass Lewis and Pensions UK have all expressed their views on the appropriateness of virtual-only meetings and in December 2025, the GC100 published guidance for companies on this meeting format. It remains to be seen however what the government will propose, and what companies may need to do in order to take advantage of any changes made by the government. As a result, we would recommend that companies wait before proposing any amendments to their articles of association or making any changes to their AGM format.

- Removal of the Investment Association (IA) Public Register: In October 2025, the government announced that it had asked the IA to discontinue its online public register of significant votes (20% or more) cast against the resolutions of listed companies. There has however been no change to the 2024 Governance Code and companies will therefore still need to make the announcements required by Provision 4 of the 2024 Governance Code in the event that any board recommended resolution receives significant votes against.

Impact of the reform of the UK prospectus regime

On 19 January 2026, the new UK prospectus regime will come into force introducing the biggest change to the UK capital markets regime since 2005 (see our blog post here for more details on the new regime).

The most significant change for existing listed companies will be that for further issuances of securities, the threshold for triggering the requirement for a prospectus will increase from 20% to 75% of issued share capital. With such a high threshold triggering the need for a prospectus and so with the cost and time concerns relating to the production of a prospectus no longer acting as an obstacle to further issuances, the level of share capital authorities sought by listed companies each year at their AGM will in practice be the effective limit on undertaking further issuances without additional shareholder approvals. While there have been no changes to the existing guidelines issued by the investor bodies, in particular to the IA's Share Capital Management Guidelines (last reviewed in 2023), and while we are not advocating that companies make any changes to the level of authorities they seek at the 2026 AGM purely because of the prospectus regime changes, this is an area on which to keep a watching brief as the market adapts to the new regime.

It should also be noted that as part of the implementation of the new regime, from 19 January 2026, the previous further issuance and block listing application processes are no longer be required (the relevant rules have been deleted from the UKLRs). Under the new regime, the application to the FCA at the time of initial listing of a class of securities covers the listing of all securities of the class, including future issuances of securities of that class. Issuers still need to apply directly to the London Stock Exchange (or other relevant recognised investment exchange) to admit their listed securities to trading.

3. Future developments

Disclosures to be included in future annual reports

Following developments during 2025, there are a number of changes which will need to be reflected in future annual reports. The commencement date for all of these, other than the UK SRS-related disclosures, have already been confirmed and for companies with a 31 December year-end, will impact the annual report they publish in 2027.

- Provision 29 of the 2024 Governance Code: boards will be required to include more detailed disclosures in relation to internal controls in the ARA (see our snapshot here for a summary of these disclosures);

- Changes to the directors' report: Under the regulations made in December 2024, with effect from financial years beginning on or after 6 April 2025, certain disclosures will no longer be required in the directors' report, including important events affecting the companies since financial year-end and policies in relation to the employment of disabled persons. It should be noted however that there are overlapping requirements in DTR 4.1.11 which will mean that unless the FCA amends its disclosure requirements, listed companies will still need to include some of the disclosures removed by the regulations (see also the Future reform proposals box below for further proposals in relation to the directors' report);

- Removal of certain directors' remuneration reporting requirements: Under regulations made in March 2025, for financial years beginning on or after 11 May 2025, a number of disclosures which were introduced in 2019 to implement parts of the revised EU Shareholders' Rights Directive have been removed. The deletions include the comparison of each director's annual pay change with the average pay change for employees over the same period (see our blog post here for more details);

- Payment practices reporting: In addition to the reporting regime already in place outside of the annual report in relation to payment practices, regulations were made in October 2025 which will require large companies to include certain summary information on their payment practices covering the whole of the financial year in their directors' report for financial years beginning on or after 1 January 2026. Where a consolidated directors' report is prepared, the disclosures need to cover all in-scope subsidiaries (that is all companies within the group which are classified as large) (see our snapshot here for further details on these changes and the wider payment practices reporting regime).

- Sustainability-related reporting: Following the adoption by the International Sustainability Standards Board (ISSB) of its first two sustainability reporting standards (SRSs) in June 2023, the government launched a consultation in June 2025 on proposed new UK SRSs, based on the ISSB SRSs. The government's response, and endorsement of these new standards, is expected imminently. The FCA is also expected to consult on changing the UKLRs to replace the existing TCFD-aligned reporting requirements with a requirement to report against the new UK SRSs, including publishing transition plans on a comply or explain basis. The timing for the developments is not yet known.

Future reform proposals

The following proposals currently being considered by the government, if and when implemented, would impact UK-incorporated listed companies and their groups, and would require some preparatory steps to be taken ahead of their implementation. Intended timings for these proposals are however, at the time of writing, unclear and so companies should wait before taking any preparatory steps.

- Reform of corporate reporting

requirements: Having undertaken to consult on

simplifying and modernising the UK's non-financial reporting

(NFR) framework in October 2024, in October 2025

the government announced changes to reduce the NFR burden, as part

of its Regulation Action Plan. The changes will

- exempt most medium-sized private companies from the requirement to produce a strategic report as part of their ARA;

- exempt wholly-owned subsidiaries from the requirement to produce their own strategic report as part of their ARA where they are included in the reporting of their parent company; and

- remove the requirement to produce a directors' report as

part of an ARA for all companies, although some of the disclosures

currently required in the directors' report which are viewed as

being useful (including on energy consumption and emissions, and

presumably the new disclosures which have been introduced in

relation to payment practices) will be relocated to another part of

the ARA.

The government intends to legislate for these changes as quickly as possible, though there has not been a clearer indication of timing, nor commencement dates for these changes.

Also, the government has announced that it will be launching a wider than expected consultation on corporate reporting in 2026. Following the October 2024 announcement, the review had been expected to look at measures to modernise the UK's NFR framework but the announcement in October 2025 made it clear that this review will look at the whole ARA. Timing for the launch of this review is also not yet clear.

- Clarification of law in relation to virtual-only shareholder meetings: Also in the October 2024 announcement, the government stated that it would clarify the legal position in relation to virtual AGMs. The uncertainty stems from the wording of section 311 CA 2006 which provides that the notice of meeting must state the "place" of the meeting. There is a debate as to what this means and whether section 311 can only be complied with if a physical location is identified in the notice as being the "place" of the meeting. Once clarified, and depending on what requirements are introduced by the government to take advantage of this clarification, companies will have the flexibility to adopt the most appropriate format for their shareholder meetings, taking into account the views of their investors.

- Audit and governance reform: A draft Bill on audit and corporate governance reform was included in the July 2024 King's Speech but it became clear that a draft Bill would not be introduced into Parliament during the session - instead the government was expected to consult on its reform proposals during 2026. In January 2026 however, the government confirmed that it would not be proceeding with this consultation, citing concerns in increasing costs on business and the progress on audit quality made since the collapse of Carillion in 2018 (which was one of the drivers for reform). The FRC will still be put on a "proper statutory footing" but the timing for this remains unclear, given the pressures on parliamentary time.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]