- within Finance and Banking topic(s)

- in United States

- within Real Estate and Construction, Media, Telecoms, IT, Entertainment and Transport topic(s)

Summary

Due to tighter margins, variable profitability and reduced cash flow, many agricultural borrowers are seeking incremental credit expansions from Farm Credit lenders on their existing facilities, and we expect that trend to continue this year. Access to “Bulge” financing has become critical for agricultural borrowers in certain sectors to manage cash flow timing and may be sought with increasing frequency during the upcoming year. In this first edition of The Trough, we briefly provide insight into the agricultural credit landscape in 2026, describe bulge financing and its function during this turbulent time, and provide a case study example illustrating how lenders are deploying this tool in practice.

Agricultural Credit Landscape in 2026

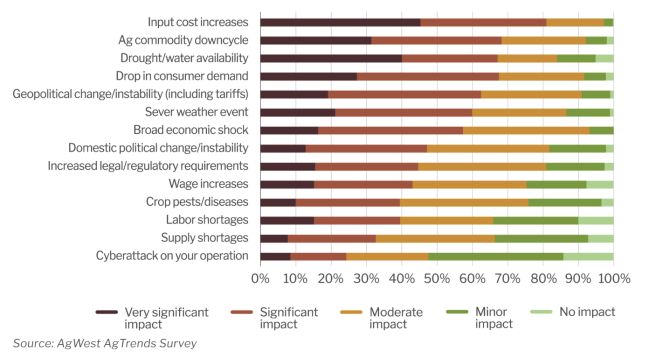

Current farmer sentiment reflects unease across the agricultural sector. Chief amongst the farmers’ concerns is supply outpacing demand within the broader agricultural economy, creating prolonged downward pressure on commodity prices. While many agricultural borrowers have enjoyed strong production and healthy yields in the last few years, input costs have risen due to high inflation, skyrocketing labor expenses (up 47% since 2020), volatile energy prices, increased interest rates and the additional burden of commodity hedges and margin calls. Further, tariffs and international conflicts are also contributing to the rise in input costs, most notably for items like fertilizers and parts for tractors and combines. Therefore, it is no surprise that the rise in input costs is viewed by Farm Credit lenders as one of the top threats to agricultural operations over the next 18 months.

These cost increases tighten farmers’ margins and consequentially raise the costs of goods for consumers. The surplus of crops, the rise in input costs and the reduction in households’ purchasing power have weakened farm incomes and reduced cash flows. It is projected that less than 50% of farm borrowers are expected to make a profit in 2026. Against this backdrop of compressed margins and constrained liquidity, incremental and short-term credit solutions have taken on heightened importance.

Top 10 Expected Threats to Agricultural Operations over the Next 18 Months (Jan. 2026)

Given the financial stress many agricultural borrowers are experiencing, they are becoming increasingly reliant on Farm Credit financing to manage cash flow and maintain flexibility. Thus, accordion and other incremental credit features are currently top of mind for Farm Credit lenders and their borrowers. Some Farm Credit lenders are turning to short-term seasonal or bridge credit, often referred to as “bulge financing” to help borrowers manage cyclical cash flow strain. Bulge financing is a temporary extension of credit, often 60 to 120 days, designed to address seasonal spikes or other defined, short-term liquidity needs. In many ways, a bulge facility functions like a bridge loan or short-term working capital facility in the broader commercial finance market. Importantly, bulge financing is generally structured to address timing mismatches and is expected to be repaid from a defined near-term liquidity event.

Accordion Facilities vs. Bulge Facilities: What’s the Difference?

A common question is, what is the difference between accordion facilities and bulge facilities? An accordion is typically uncommitted (from the lender perspective) and is built into the original loan documents and sits dormant until the borrower elects to increase the existing credit capacity, subject to approval by the committing lender(s) and agreed conditions and caps. A bulge facility, by contrast, is often a supplemental, temporary, committed tranche layered onto the existing structure via separate agreement (though it may be documented via an amendment to the existing credit agreement). Bulge financing can be viewed as a seasonal “subset” of the broader incremental flexibility universe. Although they are operationally similar (an extra or increased borrowing), the two types of flexible financing differ in their focus, timing, and repayment expectations. A key distinction is that a bulge facility is intended to solve a timing issue, rather than structural balance sheet concerns, and is not meant to permanently increase leverage. The table below illustrates some of the typical characteristics of accordion facilities and bulge facilities:

| Typical Characteristics | ||

|---|---|---|

| Accordion Facility | Bulge Facility | |

| Purpose | Long-term, “permanent” incremental capacity (growth, acquisitions, expansion) | Short-term, temporary liquidity bridge (seasonal spike, timing gap) |

| Origination | Typically built into original loan documents; exercised at borrower’s option | Provided when a specific, short-term need arises |

| Timing | Can take time to implement, given that each lender is typically invited to participate | Can typically be implemented very quickly, given the smaller subset of lenders that are involved |

| Provider | Participation typically offered to the entire bank group (with no obligation to opt in) | Offered solely by the lead lender or subset of bank group |

| Maturity | Terminates along with the existing facility maturity or longer (in the case of longer-tenor term loans) | Terminates typically within 60 to 120 days |

| Repayment Structure | Amortizes with existing facility or later; often structured with a longer weighted average life | Usually bullet maturity with mandatory take-out |

| Pricing | Same pricing as existing facility (subject to most favored nation provisions, if applicable) | May be same pricing as existing facility, or lender may charge premium pricing (higher margin, upfront fee, or short-term premium) |

| Collateral | Shares in existing collateral package | May share in existing collateral package, be secured by incremental collateral or be unsecured |

| Ranking | Pari passu with existing loans | Often pari passu, but may be structurally subordinated (e.g. if unsecured) or super-priority (depending on circumstances) |

| Covenant Treatment | Typically included in leverage ratios and other financial covenant calculations | May receive limited covenant relief or tailored treatment (structure-dependent) or may be included in financial covenants |

| Approval Mechanics | Usually requires consent from only administrative agent and increasing lenders; implemented via incremental amendment | May involve only participating lenders; Often documented as a separate tranche via agreement |

| Impact on Accordion Basket | Uses available incremental capacity | May sit outside accordion basket (depending on structure) |

When Bulge Financing Makes Sense

Bulge financing is most appropriate for Farm Credit lenders where their borrowers have a defined repayment source or anticipated cash event on the horizon. Some examples include situations where agricultural borrowers expect to receive harvest proceeds or government program payments within 60 to 90 days or where there is an imminent land closing or asset sale. If a borrower is facing a short-term liquidity crunch or harvest delay, a Farm Credit lender may find a limited bulge facility to be a more practical solution than enforcing a default or pursuing a restructuring, as the bulge facility can be implemented quickly and directly by the lead lender (or a subset of the bank group) without the requirement to market or offer the increase to each member of the bank group, as would typically be required for an accordion.

Bulge facilities also present the opportunity for lenders to (i) earn higher returns on incremental margins, upfront fees and short-term premiums, (ii) increase oversight with enhanced reporting and monitoring during the bulge period and (iii) adequately address the borrower’s issues without the cost and complexity of reopening the entire credit package and restructuring the facilities. Accordingly, bulge facilities can serve as a pragmatic risk-management tool, providing liquidity support while preserving the integrity of the broader capital structure.

Case Study – Use of Bulge Facility in Practice

In one case study, our firm assisted a Farm Credit lender with a few hundred million in bulge financing for an agricultural borrower with existing facilities in place. The aggregate amount of commitments under the existing credit package was substantial, and the loan documents included an accordion feature to the revolver and incremental term loan capacity.

Consistent with the broader market pressures described above, this borrower faced the increased costs of inputs. In order to proactively mitigate the impact of these rising costs and improve margins, the borrower planned to purchase discounted crop inputs before harvest and planting season. Therefore, this borrower sought bulge financing from its lead Farm Credit lender to fund a one-time, short-term purchase of discounted crop inputs.

In an effort to preserve the long-term flexibility of the accordion and more surgically address a temporary liquidity gap, our client agreed to provide bulge financing via an unsecured term loan rather than use existing accordion capacity. We then helped document a separate term loan tranche of bulge financing via a loan letter agreement, which incorporated the representations and warranties, covenants and pricing of the underlying credit agreement but required that the term loan be repaid in just 3 months. Had our client and the borrower come to different business terms, the loan letter agreement could have reflected different (or supplemental) representations and warranties, covenants and/or pricing with respect to the bulge facility.

The structure of the bulge facility allowed the borrower to capitalize on time-sensitive pricing opportunities without permanently increasing leverage under its existing facilities, while also providing the lender with enhanced visibility and a clearly defined repayment source tied to anticipated operating cash flows. The transaction illustrates how bulge financing can function as a helpful tool in a compressed-margin environment.

Given the financial stress that many agricultural borrowers will likely continue to experience in 2026, bulge facilities may emerge as a middle ground solution between “business as usual” and formal restructuring, allowing lenders to stabilize borrowers, avoid downside default scenarios and protect collateral, which is particularly important in agriculture where asset values can be sensitive to timing.

As illustrated above, when structured with a defined repayment source and aligned with seasonal or transactional cash flow events, bulge financing can provide meaningful flexibility without undermining long-term credit discipline. For Farm Credit lenders, thoughtful deployment of bulge facilities may not only support borrowers through cyclical volatility but also preserve relationships, enhance monitoring and maintain structural integrity within existing credit frameworks. In an environment marked by margin compression and liquidity pressure, such incremental tools are likely to remain an important component of the agricultural finance toolkit.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]