- within International Law topic(s)

- with readers working within the Advertising & Public Relations and Aerospace & Defence industries

Freight Market Rebalancing: Accelerated Supply Correction Shifts Leverage from Shippers to Carriers

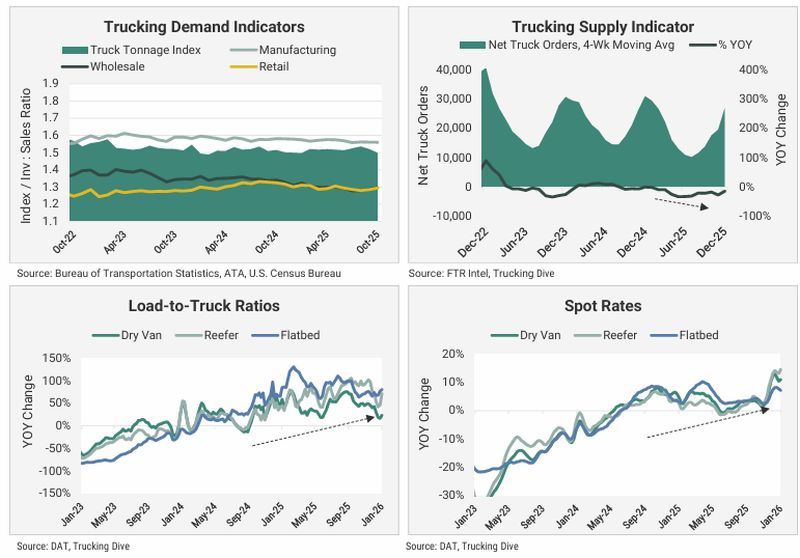

The Great Freight Recession reached a critical pivot point in 2025 as the market moved toward a structural rebalance. While shipping demand remained stagnant, the industry realized a supply correction as carrier exits accelerated. Depressed new truck orders — stifled by Trump administration tariffs, equipment inflation, and sustained low demand — have triggered a meaningful erosion in overcapacity. Consequently, load-to truck ratios climbed throughout 2025, signaling a transition in market leverage back to carriers and driving a steady increase in spot rates.

Policy Shifts and AI Adoption Will Guide a Continued Market Rebalancing in 2026

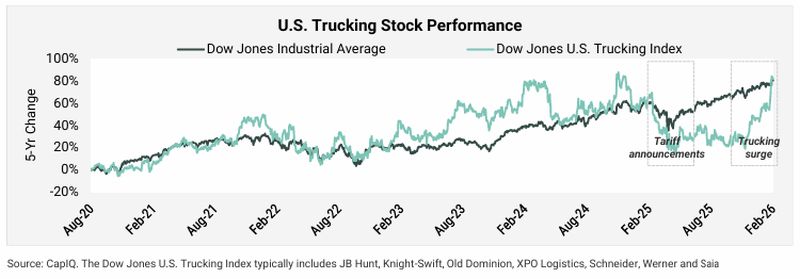

The Dow Jones U.S. Trucking Index surged in the end of 2025, signaling that equity markets are pricing in a fundamental change in freight conditions. While shipping volumes remain depressed, investors are looking past current stagnation — anticipating a market reversal as a convergence of market-led attrition and Trump administration policy shocks erodes the longstanding capacity surplus. As carriers regain market leverage, the era of uncertainty-driven low rates is ending. Shippers must now proactively manage these fundamental drivers of capacity contraction:

- CAPACITY AND LABOR CONTRACTION: Supply rebalancing is being driven by small fleet exits, coupled with federal policy shifts. Stricter English proficiency standards and increased Commercial Driver's License (CDL) restrictions for non-citizen drivers are projected to shrink the national driver pool by 5% to 12% through 2028. As these are regulatory, not market-driven exits, this creates a permanent capacity reduction that will be difficult to replace.

- EQUIPMENT COST INFLATION: Tariffs of up to 25% on medium- and heavy-duty trucks and trucking parts have spiked equipment replacement and maintenance costs. This will slow fleet modernization and may force marginal carriers to exit as maintenance becomes cost-prohibitive.

- ACCELERATED DEPRECIATION: In contrast to increased initial costs, provisions of the One Big Beautiful Bill Act generally allow deduction of 100% of the costs of a new power unit or major repair and overhaul parts in the first year. It is unclear whether this will completely offset tariff increases.

- AI-DRIVEN EFFICIENCY: To combat rising equipment and labor costs, larger carriers are deploying generative AI for route optimization and back-office automation. These tools allow advanced fleets to protect margins even as operating costs rise. This creates a growing gap between tech-enabled carriers and smaller operators who cannot afford to invest in AI.

- REGULATORY VOLATILITY: The current regulatory environment impedes long term planning. Federal rollbacks of electric vehicle (EV) mandates clash with California's stricter enforcement, preventing carriers from flexibly deploying equipment across state lines without risking non-compliance fines. In addition, an imminent Supreme Court tariff ruling may sustain current levels or trigger sudden rate adjustments and refunds.

Freight's Bargain Era is Over and Shippers Must Prepare for Rate Escalations in 2026

As the capacity surplus ends, shippers should take the following steps to stabilize supply chains:

- AUDIT REGIONAL COMPLIANCE: Review carriers on West Coast lanes to ensure equipment meets California's strict mandates, avoiding service gaps at the state border.

- PRIORITIZE LABOR STABILITY: Shift volume toward carriers with domestic recruitment programs to hedge against federal restrictions on non-citizen drivers.

- LEVERAGE TECH-ENABLED FLEETS: Partner with carriers using AI for route optimization to capture efficiency gains that offset rising operational costs.

- SECURE CONTRACTUAL PROTECTIONS: Negotiate long-term contracts before rates rise, and secure economic change provisions to mitigate volatility as the current administration pivots across evolving statutory authorities to enforce tariffs, following the Supreme Court ruling.

- REVIEW INDEX-LINKED PRICING: Transition consistent lanes to index-based contracts to preserve carrier relationships and prevent service failures during inflationary spikes.

- REDUCE OPERATIONAL FRICTION: Minimize site inefficiencies and administrative burdens to remain "shipper of choice" as leverage shifts.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]