- with readers working within the Construction & Engineering industries

U.S. truckload spot freight rates are at levels not seen since 2022. Will these increases stick, or is this just another disruption anomaly?

Many are citing winter storms across the U.S. as the main driver behind the recent increase in spot trucking rates. However, just as those storms blew over, additional volatility from U.S. tariff developments in February 2026 has added a new wrinkle to the potential recovery from the freight recession. These developments further underscore the need for shippers and carriers alike to thoughtfully navigate the current environment.

How did we get here?

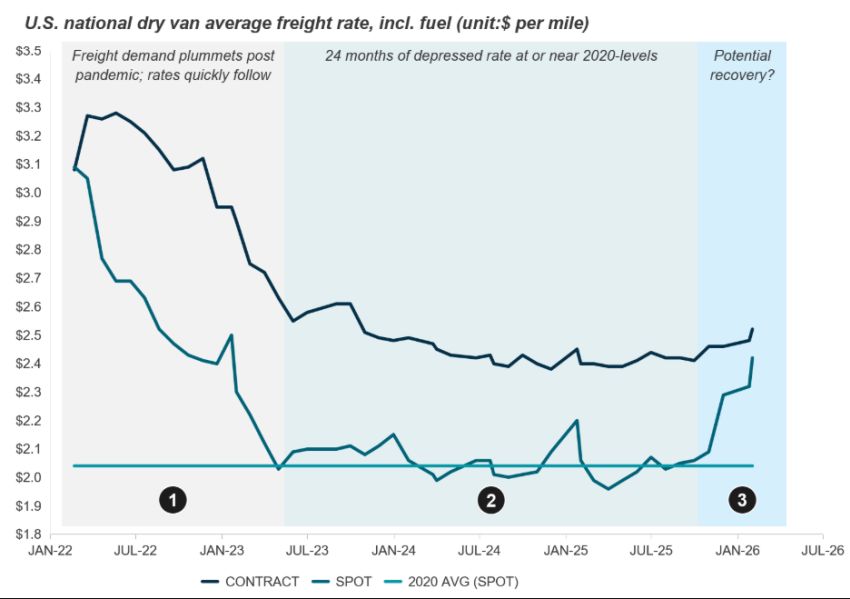

The U.S. trucking industry has been in a prolonged freight recession for nearly three years. Figure 1 below helps bring this story to life:

- Following the pandemic-induced freight market boom in the early 2020s, freight rates quickly corrected as demand fell.

- Rates have remained depressed, with spot rates hovering around 2020 levels for the last 24 months. Throughout this period, carriers have steadily removed capacity; however, rates remained depressed.

- In late 2025/early 2026, slow signs of a revival in the U.S. truckload market have begun to emerge. Spot rates are rising and approaching the contract rate. While this does not yet signal a full recovery, it may indicate that the market is nearing an inflection point.

Figure 1

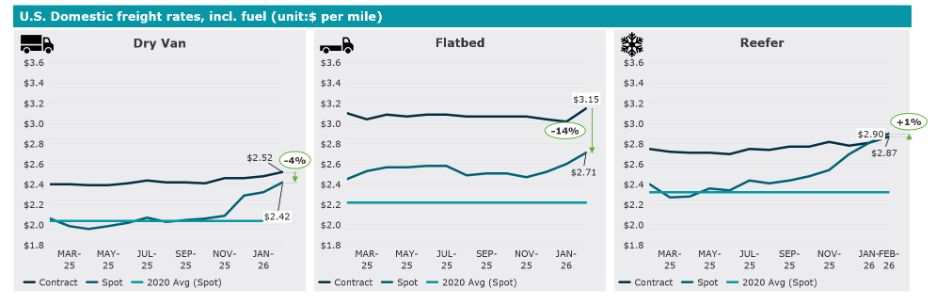

As seen in Figure 2 below, this upward movement is particularly notable because it has been broad-based rather than isolated to a single mode or geography. As spot rates begin to converge toward contract pricing (and exceed contract pricing in the case of reefer equipment), it provides carriers with the hope that enough capacity has finally exited the market to sustain much-needed price increases for the carriers. Historically, sustained spot rate recovery has often preceded broader pricing normalization, making this a key indicator to watch closely.

Figure 2

Capacity has slowly been driven out

A critical driver behind the improving rate environment is continued capacity rationalization. Over the past several years, trucking companies have reduced fleet sizes, delayed new truck purchases, or exited the market entirely. This trend has not slowed meaningfully in recent months. Most recently, another carrier, Quickway, declared bankruptcy, further underscoring the financial strain still facing parts of the industry. These exits, while painful, have played a necessary role in rebalancing supply and demand.

Beyond market-driven exits, regulatory changes are also contributing to reduced capacity. The U.S. Department of Transportation has recently stopped issuing Commercial Driver's Licenses to certain non-citizens and non-permanent residents. While the full impact of this policy shift is still unfolding, it is likely to further constrain the available driver pool, particularly in regions and fleets that historically relied on these workers. Over time, this could reinforce structural capacity tightening even if demand remains stable.

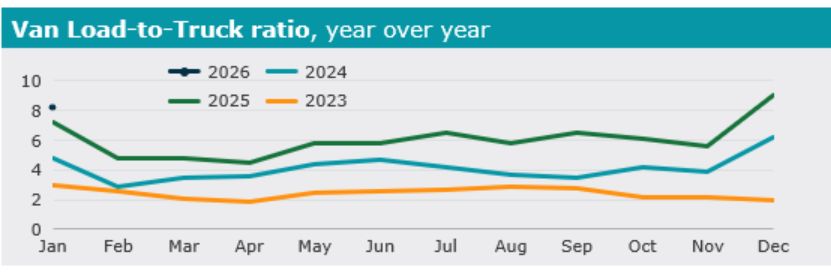

As capacity continues to tighten, the van load-to-truck ratio as seen in Figure 3 has been steadily climbing since 2023. This metric, which reflects the balance between freight demand and available trucks, suggests that carrier leverage could be improved. A rising ratio typically indicates a healthier market for carriers and often precedes further rate increases if sustained.

Figure 3

A leading indicator?

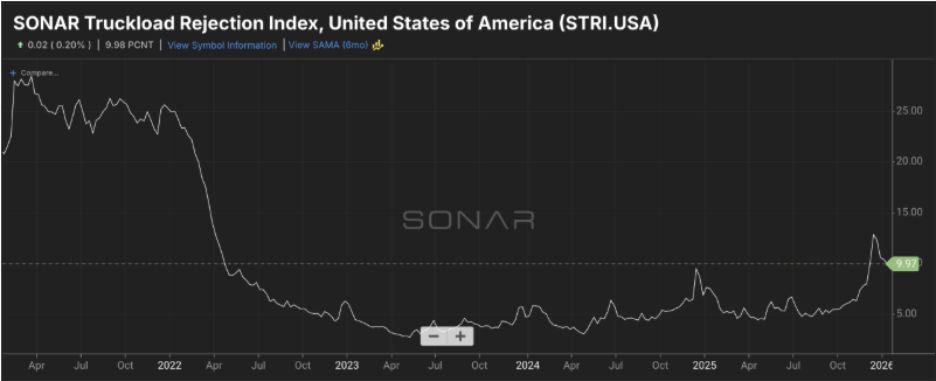

Load rejection rates have been elevated relative to prior years of the downturn, with industry indices showing rejection rates near 10% — one of the highest levels seen during the current cycle — suggesting carriers are becoming more selective or capacity is tightening. Some regional data has shown even higher rejection spikes following severe winter weather. While short-term week-to-week fluctuations can occur, the broader elevated rejection environment aligns with other tightening indicators such as rising load-to-truck ratios and stronger spot rate movements.

Figure 4

Some of the recent market tightening may be partially attributed to severe winter weather across large portions of the country, which temporarily disrupted transportation networks and reduced effective capacity. Weather-driven volatility is not unusual and can distort short-term indicators. The key question now is whether the recent improvements represent temporary weather-driven increases or the early stages of a more durable recovery. The next weeks will be critical in determining whether momentum persists as weather conditions normalize.

More disruption

New U.S. tariff uncertainty could further confuse the U.S. trucking market as shippers begin navigating the most recent changes. While the market may see short-term volatility due to frontloading, it is unlikely that the most recent developments will cause a material shift in durable demand for trucking in the U.S.

What can shippers do?

If the freight recession is truly nearing its end, shippers should begin preparing for a shifting market environment. Recommended actions include:

- Reassessing contract exposure and renewal timing – monitor tender rejection rates and what shipments are being covered by the spot board.

- Strengthening strategic carrier relationships – strong relationships include proactive notification and creative contracts, such as index-based rates

- Monitoring lane-level volatility rather than relying solely on national averages – while the national average tells an interesting story, specific markets may be more or less affected

While the market is not entering a boom phase, the balance of power may be slowly recalibrating.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.