- within Corporate/Commercial Law topic(s)

- in United States

- with readers working within the Media & Information industries

Mayer Brown analyzed 34 insider trading policies to understand how large financial institutions address the heightened insider trading risks they face relative to other public companies. We analyzed the insider trading policies of 24 publicly traded investment banks, nine publicly traded private equity sponsors and one publicly traded financial institution with substantial operations in both investment banking and private equity management (which institution we include in both the investment bank and private equity sponsor statistics herein). Since the nature of their business necessarily creates both frequent opportunity for insider trading (especially in other companies' securities, including through "shadow trading") and a large universe of employees with access to material non-public information ("MNPI"), a survey of how these types of large financial institutions generally address such risks in their insider trading policies can be informative to financial institutions reviewing their existing policies.

Our analysis focuses on the following areas:

- Parameters for quarterly and ad hoc blackouts for trading in an institution's own securities;

- Pre-clearance and account supervisory requirements for personal securities trading and related restrictions (e.g., restricted lists and minimum holding periods);

- Restrictions on hedging, pledging and gifting of securities;

- Applicability to other companies' securities;

- Prohibitions on tipping; and

- Applicability to former employees and directors.

While we believe our analysis considers a representative sample of investment banks and private equity sponsors, we note that there are limitations inherent in sampling, notably that our review is limited to only policies filed with the U.S. Securities and Exchange Commission (the "SEC") on EDGAR by publicly traded financial institutions in response to Form 10-K or 20-F requirements to file such policies.

We are not commenting on the differences in blackouts for equity securities, equity-linked securities and fixed income securities of an institution.

Blackout Periods

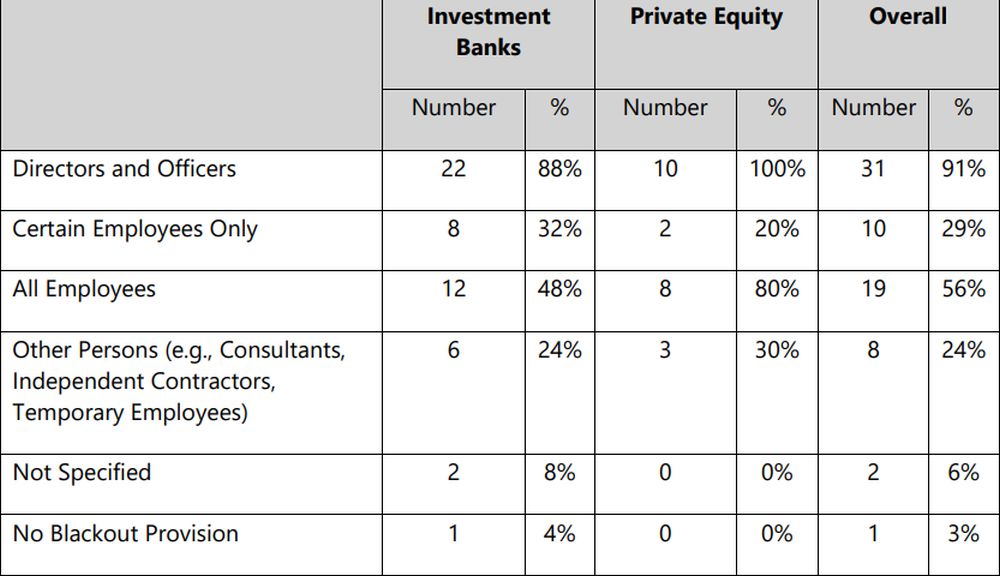

Which insiders are subject to blackout periods?*

* The categories represented by the first four rows in this table are not mutually exclusive, except that Certain Employees Only and All Employees are mutually exclusive of one another. A financial institution may be counted in more than one row; e.g., an investment bank that imposes blackout restrictions on all of its directors, officers and employees would be counted in the Directors and Officers and All Employees rows. For this reason, the percentage columns do not sum to 100%.

One investment bank's policy uses a "downstreaming" requirement to determine which insiders are subject to blackout periods, i.e., the policy only explicitly applies blackout requirements to directors and certain officers but requires those officers to designate and notify other employees to whom the blackout restrictions will also apply.1

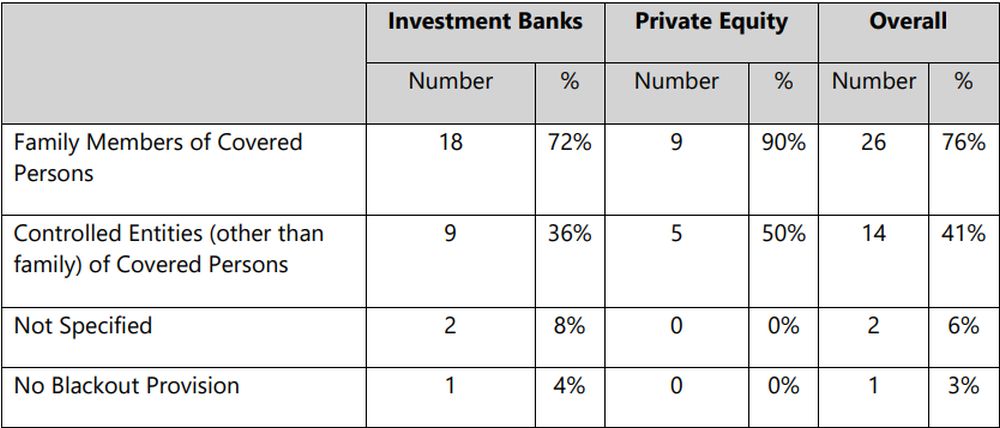

Which persons and entities related to covered insiders are also subject to blackout periods?*

* The categories represented by the first two rows in this table are not mutually exclusive. A financial institution may be counted in both of the first two rows if it imposes blackout restrictions on both family members and controlled entities of covered persons. For this reason, the percentage columns do not sum to 100%.

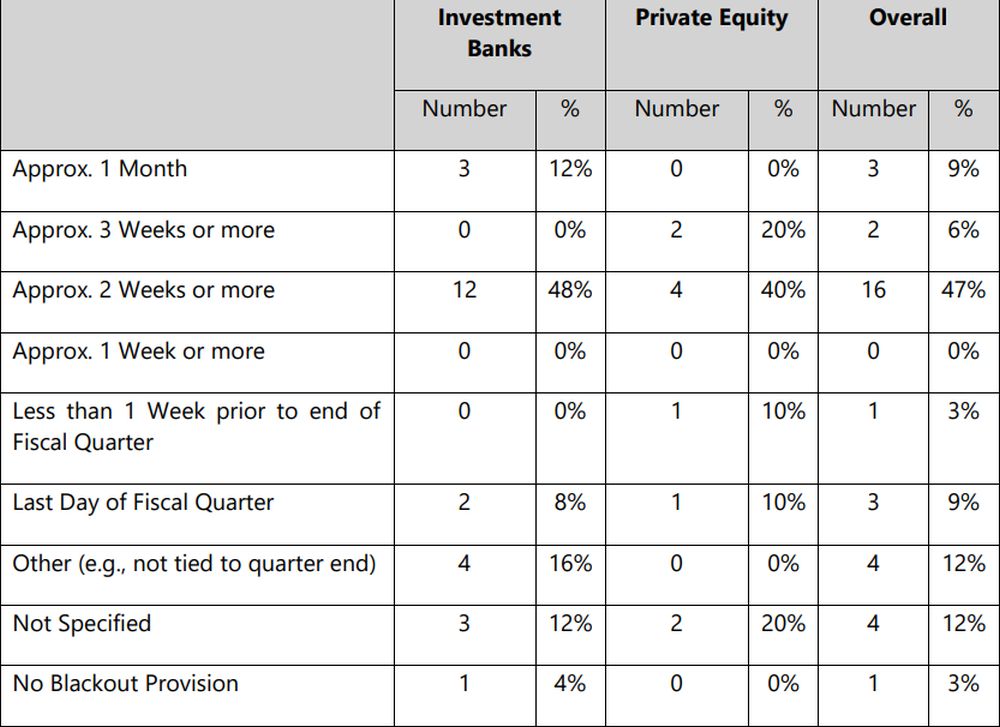

How long before the end of the fiscal quarter do quarterly blackout periods begin?

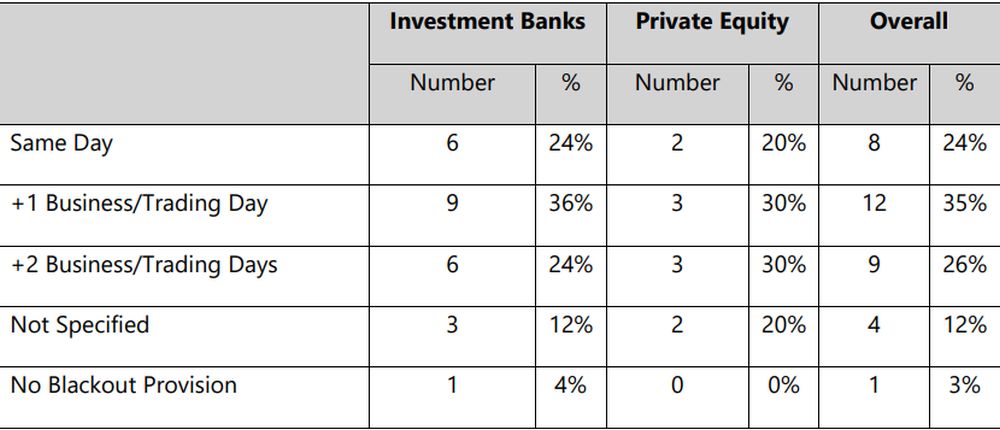

When do quarterly blackout periods end following the financial institution's publication of its earnings release (i.e., when is the last day of the blackout period)?

Two investment banks' policies impose longer blackout periods (i.e., shorter trading windows) on directors and executive officers than on other insiders.2

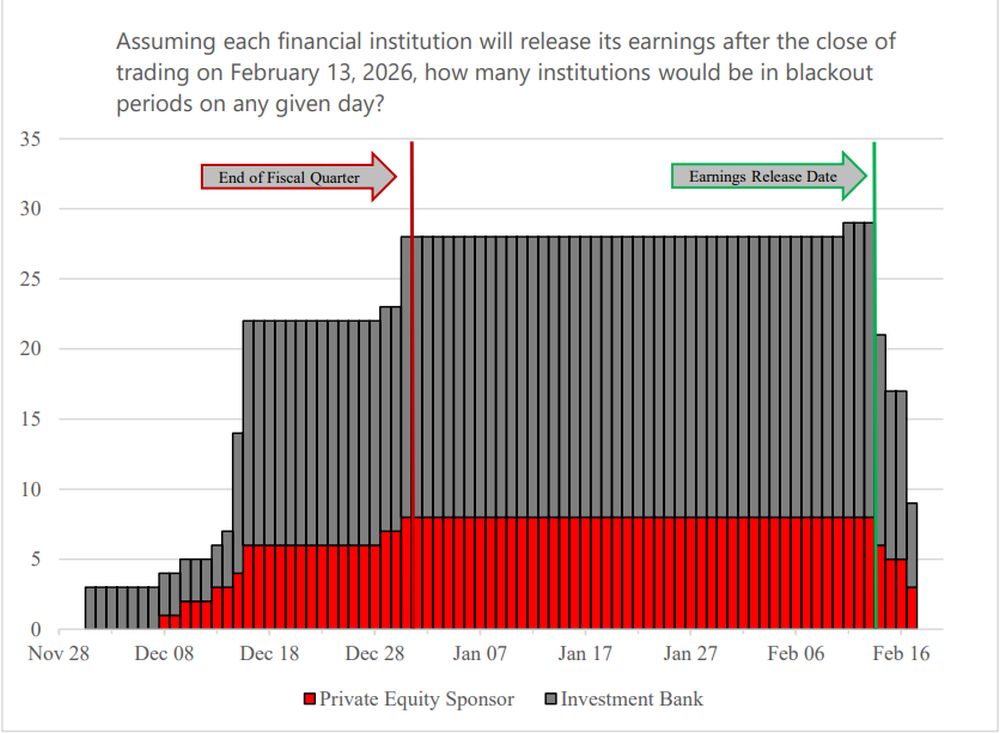

To visualize this data, the chart below represents the blackout periods each of the surveyed insider trading policies would impose prior to the publication of fourth quarter earnings assuming that (a) third quarter earnings were released on November 14, (b) the fourth quarter ends on December 31 and (c) fourth quarter earnings will be published after the close of trading on February 13.3

Based on such assumptions, blackout periods would range in length from just five calendar days to as long as 78 calendar days, with the median blackout period lasting 60 days. A blackout period of 60 days would mean insiders would be blacked out from trading their employer's securities for approximately two-thirds of a fiscal quarter due solely to regular quarterly blackouts.

In addition, 82% of the policies we surveyed contemplate the imposition of additional, distinct blackout periods, often called ad hoc or "event-driven" blackouts. Ad hoc blackouts can apply to some or all of the insiders generally subject to quarterly blackouts, and are generally imposed when insiders may have MNPI about specific events, such as M&A activity, significant litigation or major announcements. If an insider is subject to a quarterly blackout followed by an ad hoc blackout, an insider may be prohibited from trading in their employer's securities for most or all of any given quarter (noting that ad hoc blackouts are generally not enacted in every quarter).

To view the full article, click here.

Footnotes

1. This investment bank is counted in the Directors and Officers, Certain Employees Only and Other Persons rows in the "Which insiders are subject to blackout periods?" table.

2. The tables and chart in this section represent these investment banks based on the generally applicable blackout period, not the longer blackout periods imposed on directors and executive officers.

3. This chart does not represent the five financial institutions that either impose blackout periods without specified date ranges or do not impose blackout periods.

Visit us at mayerbrown.com

Mayer Brown is a global services provider comprising associated legal practices that are separate entities, including Mayer Brown LLP (Illinois, USA), Mayer Brown International LLP (England & Wales), Mayer Brown (a Hong Kong partnership) and Tauil & Chequer Advogados (a Brazilian law partnership) and non-legal service providers, which provide consultancy services (collectively, the "Mayer Brown Practices"). The Mayer Brown Practices are established in various jurisdictions and may be a legal person or a partnership. PK Wong & Nair LLC ("PKWN") is the constituent Singapore law practice of our licensed joint law venture in Singapore, Mayer Brown PK Wong & Nair Pte. Ltd. Details of the individual Mayer Brown Practices and PKWN can be found in the Legal Notices section of our website. "Mayer Brown" and the Mayer Brown logo are the trademarks of Mayer Brown.

© Copyright 2026. The Mayer Brown Practices. All rights reserved.

This Mayer Brown article provides information and comments on legal issues and developments of interest. The foregoing is not a comprehensive treatment of the subject matter covered and is not intended to provide legal advice. Readers should seek specific legal advice before taking any action with respect to the matters discussed herein.

[View Source]