This article from Eurofast is most popular:

- within Tax topic(s)

- in European Union

Eurofast ’s articles from Eurofast are most popular:

- within Tax topic(s)

- in European Union

- in European Union

- in European Union

- in European Union

- in European Union

- in European Union

Eurofast are most popular:

- within Insurance and Law Practice Management topic(s)

1. Individuals

1.1 Personal Income Tax

Personal income tax applies to all incomes obtained by Romanian residents from sources within or outside Romania. Non-residents are taxable on their income derived from Romania.

1.1.1 Rates

| Standard Tax Rate |

10% |

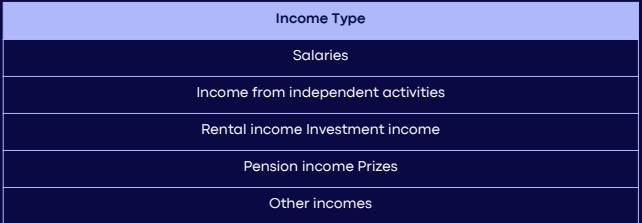

1.1.2 Taxable Income

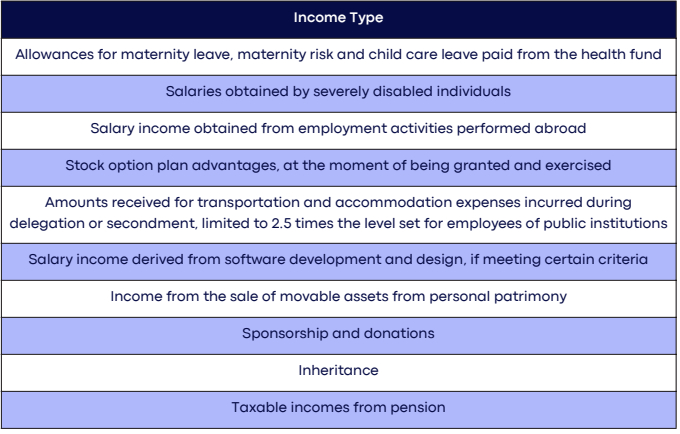

1.1.3 Exempt Income

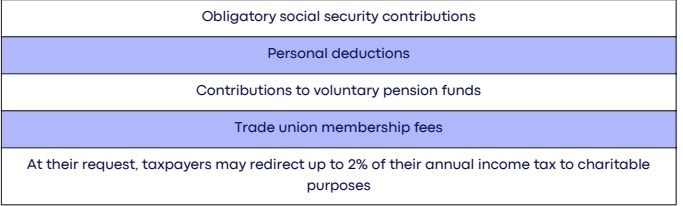

1.1.4 Deductible Expenses/Allowances

1.2 Social Security Contributions (SIC)

1.2.1 Taxpayers

- Resident and non-resident individuals that are employed in Romania, self-employed individuals, freelancers and others;

- Retired persons with retirement allowances above RON 2.000;

- Employers (including public entities).

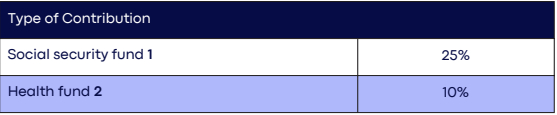

1.2.2 SIC Rates

1.2.3 SIC Rates for Self-Employed Persons

Notes:

1 If the obtained incomes are over 48.600 / 97,200 LEI per year.

2 Minimum ceiling – 24.300 LEI, Maximum ceiling 291.600 LEI.

To view the full article clickhere

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.