- within Corporate/Commercial Law topic(s)

- with readers working within the Law Firm industries

- within Real Estate and Construction, International Law, Media, Telecoms, IT and Entertainment topic(s)

Investors of Mergers and Acquisitions (“M&A”) transactions in Indonesia should be mindful of key considerations that require close monitoring. In practice, M&A deals are risky due to regulatory and compliance requirements, particularly when they affect the licensing, reporting, corporate governance, and control structure of target companies. This legal insight aims to assist business actors in identifying the key risks in M&A transactions, and understanding the practical implications across the transaction lifecycle.

A. Key Risks and Considerations in Investment and Due Diligence for Risk Mitigation

Investors in acquisitions of existing Indonesian companies need to be aware of jurisdictional risks by understanding Indonesia’s current condition. They should adapt their business and transaction strategies to support their onward operation in Indonesia.

1. Key Risks and Consideration in Indonesia M&A Transaction

(a) Political Risk

The current administration, led by President Prabowo Subianto, uses exaggerated nationalism narrations, and accuses oppositions or criticism toward his administration to be driven by foreign powers. But they claim Indonesia is an active, free, non-aligned country in international relations. They are keen to prioritize protection of natural resources as promulgated under Article 33 paragraph 3 of the 1945 Constitution, based on which, the country’s earth, water, and natural resources are controlled by the state and used for the prosperity of the people. This article provides the basis of protectionist policy towards the management, cultivation, and commercialization of natural resources in Indonesia. With the recent natural disaster having severe impacts on North Sumatra, West Sumatra, and Aceh provinces, the government is reviewing, and possibly revoking the licenses of some mining and plantation companies. This move has alerted foreign investors on the stability of their operation in the country.

Corruption, collusion, and nepotism practices surrounding legal enforcement in the public sector are common risks in Indonesia, despite efforts to digitalize the licensing system and bureaucracies. Investors should conduct the due diligence on target companies to minimize risks of incompliance with the anti-bribery and corruption regulations, and ensure the companies’ compliance with the good corporate governance.

(b) Economic Risk

Indonesia’s Stock Price Index had an exceptional selling pressure late in January 2026, weakening the local and foreign investors’ trust in the market. Morgan Stanley Capital International initially released their assessment and decided to temporarily freeze all index changes in the Indonesian market. MSCI concluded that Indonesia has a serious transparency problem in terms of shareholders’ information disclosure, which is not in accordance with the international standard and practice. Further, MSCI is worried that the coordinated trading behaviour within Indonesia’s investment market has distorted the mechanism making the prices do not reflect fair valuations. These circumstances are crucial for investors, planning to invest in Indonesia, to determine their next steps.

Depreciation of Rupiah has created a situation where the confidence in Indonesia’s economy is declining. The stock market and currency have come under stress, with investors becoming more cautious due to policy uncertainty, and having concerns over the rising government spending. Capital outflows grow, while confidence weakens, highlighting Indonesia’s increasing exposure to global economic challenges and domestic policy risks.

(c) Social Risk

Although social communities in Indonesia are generally in peaceful state, social risks with contributing factors, such as growing issues in economic disparities are still concerning to major investors. Social unrests or local/horizontal conflicts would potentially disrupt business activities.

The increase of Regional Minimum Wage (Upah Minimum Regional or “UMR”) put investors in a difficult position. They are required to adjust their employees’ salaries to accommodate the new UMR provisions. With Indonesia’s Manpower Law heavily leaning towards employees’ protection, investors of labour-intensive industries may face risks of mass protests due to disputes over remuneration and unfulfilled UMR increases.

(d) Environmental and Ecological Risk

Major projects in Indonesia, particularly those in mining, agriculture, and infrastructure, face severe environmental and ecological risks due to deforestation, biodiversity loss, water pollution, and soil degradation. Meanwhile, poor waste management and reclamation practices often lead to flooding, erosion, and landslides. These impacts also create social tensions, involving local and indigenous communities.

Investors of mining, agriculture, and infrastructure projects need to ensure that their projects are in compliance with the prevailing regulations, and have minimized impacts on the surrounding environment.

(e) Regulatory and Legal Risks

Significant policy uncertainty due to frequent regulatory changes and overlapping rules involving ministries, also the central and regional governments, has led to legal ambiguity, higher compliance costs, and unexpected approach in operational requirements to businesses. It is difficult to predict how policies will be enforced, as regulations constantly change. As a result, many investors remain cautious, and wait for a more stable and predictable regulatory environment before committing to long-term investments.

Foreign investors have concerns over the legal certainty and reputation of the Indonesian courts in presiding over disputes involving foreign parties, and whether the court judgments are enforceable. Despite the uncertainties, a Client can have alternative dispute resolution of arbitration through BANI (Badan Arbitrase Nasional Indonesia), incorporated into the contracts with the Indonesian parties.

2. Key Due Diligence for Risk Mitigation in an M&A Transaction

Business actors should consider several matters through an LDD process before conducting an M&A transaction to ensure that the target company has complied with the applicable laws and regulations. Relevant documents and areas examined typically include:

(a) The Primary Corporate Documents

- Deed of Establishment (“DoE”), Articles of Association (“AoA”), and their amendments stipulating the historical changes of AoA, management compositions, and share ownership;

- all acknowledgements and/or approvals issued by the Minister of Law (“MoL”) for the DoE, AoA, and their amendments;

- share certificates and shareholder registers;

- the annual general meetings of shareholders and other extraordinary general meetings of shareholders; and

- all documents on the beneficial

(b) General and Sector Specific Business Licenses

Before completing an M&A transaction, the investor should ensure that the target company’s licenses have been obtained and remain valid. They include all relevant licenses of the primary and secondary business activities. The investor should also conduct a due diligence on the environmental aspects, and ensure that all the required environmental licences, permits, and reporting obligations are fully compliant.

(c) Ongoing Compliance and Reporting Obligations

The due diligence also covers a review over the target company’s compliance with the reporting obligations associated with their licenses and business activities. The documents include the:

- Investment Activity Report (Laporan Kegiatan Penanaman Modal or “LKPM”)

- Mandatory Company Manpower Report (Wajib Lapor Ketenagakerjaan Perusahaan or “WLKP”)

- Annual Income Tax Return (Surat Pemberitahuan Tahunan)

- Other Sector Specific Reporting Obligations (if applicable). Companies holding specific licenses with business activities in financial services, payment system operator, mining, or construction are subject to specific reporting obligations. Target companies should comply with these obligations to avoid administrative sanctions for incompliance.

(d) Assets, Loans, and Securities

The due diligence of a target company’s risks and obligations should identify the assets, active loans, and securities in respect of the assets. If the company has properties, the investor is recommended to conduct a proper review of the land documentation and ownership status, including any encumbrances over such properties by making enquiries to the relevant government agencies, such as the Local Land Office (Badan Pertanahan Nasional).

If the target company has any third-party financing, the investor needs to check if the current agreement has restrictions triggering a change of control or negative covenants.

(e) Insurance

Subject to business activities of the target company, the investor should review the company’s insurance policies on its assets and premise, also professional indemnity insurance for the key leadership personnel or Board of Directors.

(f) Intellectual Property

It is important to identify all intellectual properties registered by the target company, including those on its products and registered marks.

(g) Personal Data Protection Policy

All companies processing personal data should comply with the personal data protection laws in Indonesia. Therefore, the due diligence should cover the target company’s data protection policies and procedures to make sure they are in order. To limit any potential exposure to the liabilities, the investor should check if the company’s personal data processing meets the standard and requirements under the prevailing laws.

(h) Employment

The associated risks on manpower law are relatively high, so the due diligence should cover the

- existing employment contracts, including the indefinite and definite term employment contracts;

- company regulation and/or collective labour agreement;

- social security program for the employees including the payment contributions;

- WLKP;

- Foreign Manpower Utilization Plan (if any); and

- other employment-related

(i) Litigation

An investor is recommended to carry out a litigation search on the target company’s shareholders, Board of Directors, and Board of Commissioners to the relevant courts and arbitration bodies having the jurisdiction to confirm any ongoing litigation..

After completing the due diligence, having the satisfactory result, and identifying the potential risks, the investor can proceed to effecting the transaction. An investor can request the target company to rectify unresolved issues, or leverage representatives and warranties to limit their potential liability.

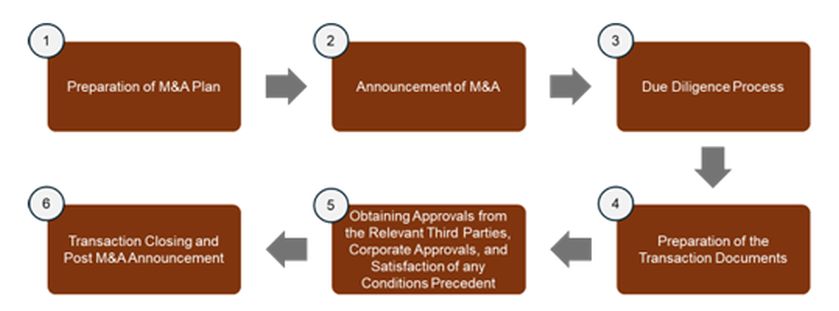

B. General Overview of the Step–by–Step Procedure in Effecting M&A Transactions

As a general guideline, an M&A transaction causing a change of control of the target company shall go through the following procedure:

In effecting the transaction, the investor needs to structure their share ownership. It requires proper legal structuring to avoid violations. The prohibitions are:

(a) Prohibition on Cross Shareholding

Under Article 36(1) of the Company Law, a company is prohibited from issuing shares to be held by itself. The company is also prohibited from directly or indirectly (cross) holding shares issued by another company.

Article 36(2) of the Company Law further provides that this restriction does not apply if the shares are acquired through a transfer by operation of law, gift, or inheritance. These shares must be transferred to other parties not prohibited from owning such shares, within one year after the acquisition.

(b) Nominee Arrangement

Pursuant to Article 33(1) of Law No. 25 of 2007 on Investment, as amended by Law No. 6 of 2023 on Enactment of Government Regulation in Lieu of Law No. 2 of 2022 on Job Creation into Law (“Investment Law”), investors of limited liability companies are prohibited from entering into any agreement and/or making any statement confirming the shares ownership for and on behalf of another person. In practice, this is commonly referred as a nominee arrangement.

Article 33(2) of the Investment Law provides that such agreement and/or statement shall be null and void by operation of law.

After completing the M&A transaction, the company must provide a newspaper announcement to notify creditors, employees, shareholders, and other interested parties.

The target company is required to report the completed transaction to the Indonesian Competition Commission (Komisi Pengawas Persaingan Usaha or “KPPU”), if the transaction meets the criteria under KPPU Regulation No. 3 of 2023 on Assessment of Mergers, Consolidations, or Acquisitions of Shares and/or Assets that may Result in Monopolistic Practices and/or Unfair Competition (“KPPU Reg. 3/2023”).

Under KPPU Reg. 3/2023, a transaction must be reported if it cumulatively meets the relevant requirements, including:

- meeting the asset and/or sales thresholds;

- involving a change of control;

- not a transaction between affiliated business actors; and

- involving business actors with assets and/or operations in

Antitrust clearance and timely reporting are important to avoid sanctions and ensure that the transaction does not create monopolistic practices or unfair competition.

C. Closing Remarks and Recommendation

In Indonesia, investment requiring acquisition of an existing operating company can be exposed to various risks. But if it is managed properly with a thorough understanding of the status and issues of the target company, such risks can be mitigated to ensure profitability and commercial success.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.