- in United States

- with readers working within the Retail & Leisure industries

AlixPartners' annual Global Consumer Outlook provides insight into how companies can take advantage of changing behaviors expected to drive the U.S. travel market in 2026.

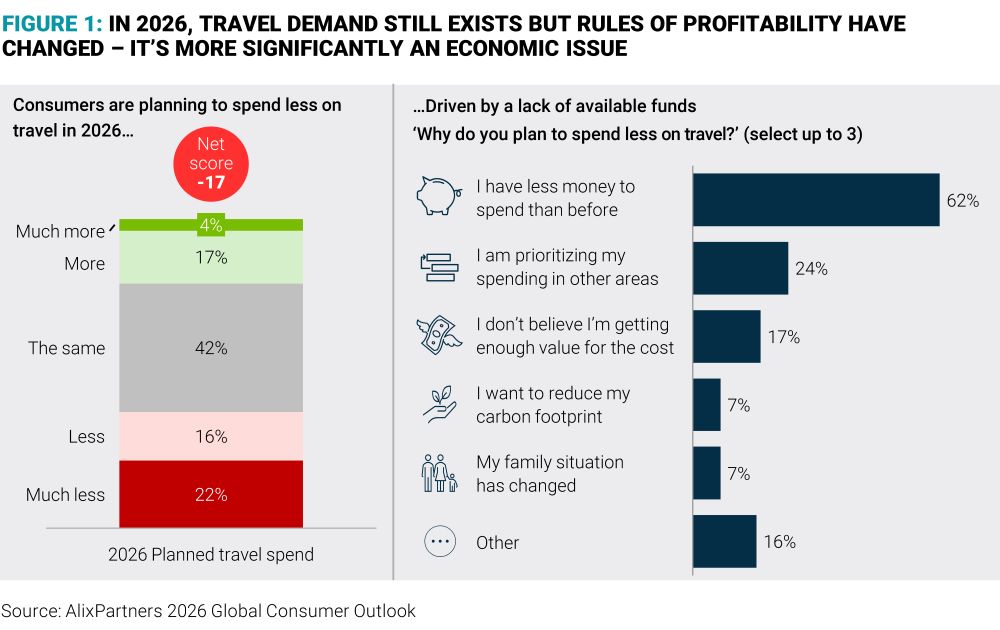

Growth opportunities have shifted from the broad post-pandemic boom to a more selective and value-disciplined market. Travel growth in the U.S. has lagged that of other major markets, and AlixPartners' survey shows that more consumers expect to spend less on travel in 2026 than the prior year, resulting in a negative net spend intention of 17 points for 2026.

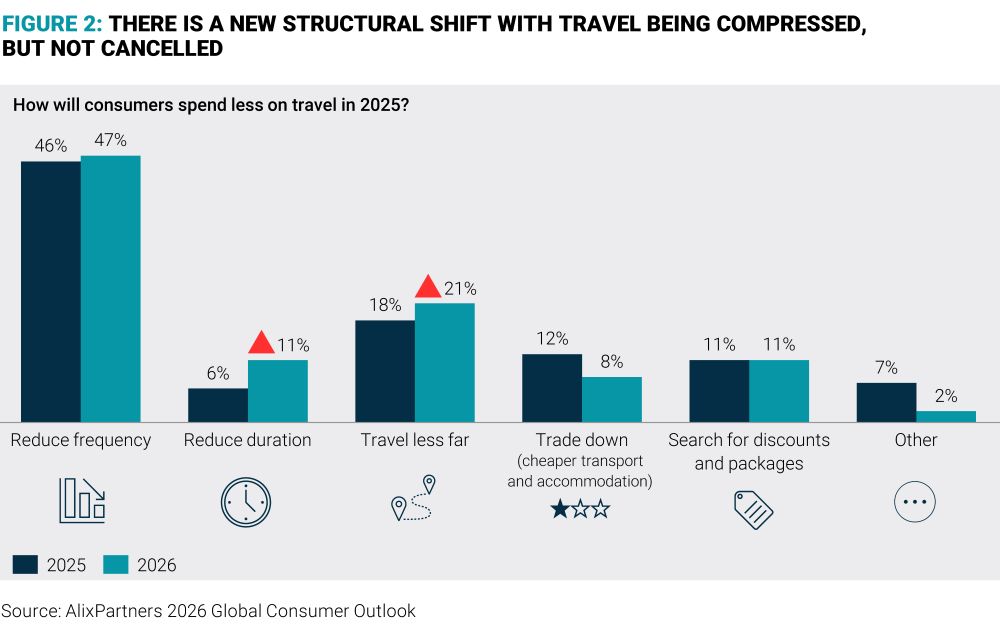

The primary driver of this lowered intention is economic, and while consumers still overwhelmingly say they will trim spend by reducing trip frequency, we are now seeing their behavior further compress with more planning to travel closer to home, take shorter trips. In particular, affluent travelers are increasingly seeking discounts, signaling a potential shift in the luxury market.

Consumer perception of affordability continues to override the reality of air fares that have fallen in real terms over the past three years – and down 1.1% in December 2025 - according to government data. Simply stated, the perceived erosion of value is rising faster than actual affordability pressures, mirroring trends in other discretionary categories such as eating out.

For operators, this moves differentiation away from headline rates alone toward transparency, packaging, and a clear value ladder across offerings.

The survey also highlights fresh drivers at play, notably an increased focus on safety and reassurance among younger travelers. Direct booking continues to gain share, especially among older and more affluent travelers, and it's becoming tougher to charge extra for sustainability-friendly features.

This raises the stakes on execution quality, reliability, and communication, especially during this time of heightened disruption. Travel leaders should:

- Localize growth. Prioritize regional, repeat, and short stay demand to stabilize volume and protect yield

- Rebuild value. Tackle affordability concerns with defensible offerings that avoid discounting and fee proliferation

- Streamline execution. Standardize services and processes to mesh lower labor intensity with improved consistency of delivery

- Monetize the relationship. Distribution and loyalty strategies built on acquisition cost, lifetime value, and margin contribution

- Declutter corporate spend. Eliminate low ROI programs and complexity to refocus spend on demand and margin drivers

Compression is the new reality. Bags are still being packed, just more economically and for shorter stays closer to home. Affluent behavior is converging on mass market consumers faster than expected, and inbound international travel remains depressed. All provide opportunities for operational excellence and execution.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.