- within Energy and Natural Resources topic(s)

- with readers working within the Business & Consumer Services and Property industries

The Internal Revenue Service ("IRS") has released long-awaited guidance on the "prohibited foreign entities" or "FEOC" requirements for certain federal clean energy tax credits. The guidance, Notice 2026-15, primarily addresses how to calculate the "material assistance cost ratio" or "MACR" for purposes of claiming certain clean energy tax credits (the "MACR guidance"). The MACR is the ratio of clean energy facility equipment costs that can be attributed to prohibited foreign entities ("PFEs"), which must not exceed certain statutory thresholds, lest the facility lose access to energy tax credits to which the MACR requirements apply.

Despite clarifying how to calculate "material assistance" from a PFE, the MACR guidance is silent on many other critical aspects of the PFE requirements—issues that have prompted questions from energy industry stakeholders ever since the enactment of the "One Big Beautiful Bill Act" (the "OBBBA"). Most notably, the MACR guidance says little about how to determine whether an entity qualifies as a PFE in the first instance, including whether contractual arrangements granting "effective control" rights to "Specified Foreign Entities" (as defined in the OBBBA) could trigger PFE status.

The MACR guidance also does not elaborate on the 10-year recapture period for certain investment tax credit eligible facilities and avoids any substantial discussion of the "beginning of construction" requirements for PFE purposes, though it requests comment on that topic and others to inform potential future proposed regulations. Stakeholders will need to wait for those proposed regulations, and perhaps longer, to better understand many key aspects of the PFE requirements the MACR guidance omits, though they may make their voices heard on those issues now via written comments to IRS due by March 30, 2026.

This alert focuses on the MACR guidance for the Section 48E investment tax credit ("ITC") and Section 45Y production tax credit ("PTC") but not the Section 45X advanced manufacturing credit. We will address Section 45X in a future alert.

Key Takeaways:

- The MACR guidance sets out five steps for calculating the MACR for "qualified facilities" seeking the ITC or PTC and "energy storage technologies" seeking the ITC. It also establishes three "interim" safe harbors for MACR calculations—the Identification Safe Harbor, Cost Percentage Safe Harbor, and Certification Safe Harbor—based in part on previous guidance for the domestic content adder. The guidance also addresses MACR for purposes of the 80/20 rule for facility retrofits and for qualified interconnection property that can be included in the ITC basis if certain requirements are met.

- The MACR guidance does not address other critical PFE requirements, such as how to determine whether an entity is a PFE, what constitutes "effective control" for purposes of determining PFE status as a "Foreign-Influenced Entity," how to apply the 10-year recapture period for certain ITC eligible facilities, and others.

- The MACR guidance also does not address the "beginning of construction" for purposes of applying the PFE requirements, though it confirms that Notice 2025-42, guidance issued last year on beginning of construction for solar and wind facilities, does not apply to the PFE requirements. The MACR guidance nonetheless requests comment on "substantiation and documentation" that should be required to support "anti-circumvention" rules under the PFE requirements, including demonstrating "that beginning of construction" has occurred for purposes of the "PFE and material assistance rules."

- The guidance is framed as a prelude to "more comprehensive" proposed regulations "and other guidance." Treasury and IRS intend to issue proposed regulations on the PFE requirements and request stakeholder comments on several topics to be submitted by March 30. Thoughtful comments will be critical to developing workable PFE standards in any forthcoming regulations or further guidance.

I. Introduction

The One Big Beautiful Bill Act ("OBBBA"), passed last July, imposes new prohibited foreign entities ("PFE") requirements on clean energy and storage facilities seeking either the ITC or PTC, as applicable. They're often referred to as the "FEOC" or "foreign entity of concern" requirements.

A PFE is an entity with certain ties to China, Russia, Iran, or North Korea, though the statutory definition is broad and encompasses other entities and individuals as well. Developers claiming the ITC or PTC cannot themselves be PFEs. Nor can their facilities receive "material assistance" from PFEs above certain thresholds. The "material assistance" requirement applies only to facilities for which construction begins for tax purposes on or after January 1, 2026.

To comply with the "material assistance" requirement, developers must calculate a "material assistance cost ratio" ("MACR") for each of their "qualified facilities" for which they're seeking the ITC or PTC or each of their "energy storage technologies" for which they're seeking the ITC. The MACR is a percentage of certain facility costs attributed to non-PFE suppliers.

The intent is to deter developers from using equipment produced in certain foreign countries. Developers must keep their facilities' MACRs at or above thresholds set by law to remain eligible for the ITC or PTC. The threshold for solar, wind, and other "qualified facilities" is at least 40 percent for facilities for which construction begins for tax purposes in 2026. The 2026 threshold for storage facilities is 55 percent. The thresholds increase every year.

II. Calculating the MACR in Five Steps

The MACR is the percentage of non-PFE equipment costs incorporated into an eligible facility. It is calculated by adding up certain direct costs attributed to PFE equipment in a facility, subtracting those PFE costs from total direct equipment costs, and dividing by total direct equipment costs.

The "equipment" costs for MACR purposes are the direct costs of so-called "manufactured products" or "MPs" and their "manufactured product components" or "MPCs" that are incorporated into a facility upon completion of construction.

The MACR is calculated for each "qualified facility" or "energy storage technology" that can function independently from other facilities. A separate MACR is calculated for "qualified interconnection property" if that property can be included in a qualified facility's ITC basis—more on that below.

The MACR guidance sets out five steps for developers to calculate the MACR for their facilities.

A. Step 1: Identify MPs and MPCs

Developers must identify each of the MPs and MPCs in their facilities. Developers can refer to previous domestic content guidance in Notice 2023-38, which defines MPs and MPCs for purposes of the domestic content adder to the ITC and PTC, as well as certain tables in that notice and subsequent Notice 2024-41 and Notice 2025-08, which the MACR guidance refers to collectively as the "2023-2025 Safe Harbor Tables."

The generic MP and MPC definitions in the domestic content guidance are vague. The 2023-2025 Safe Harbor Tables more helpfully identify specific MPs and MPCs for solar, onshore wind, and battery energy storage systems, as well as MPs for hydroelectric, pumped hydropower storage facilities, and offshore wind facilities.

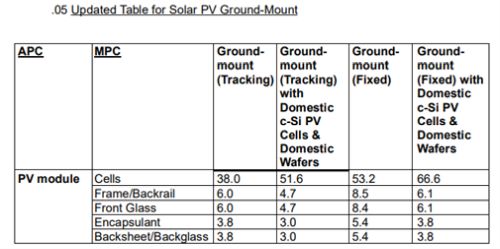

For example, Notice 2025-08 identifies PV Modules, PV Trackers, and Inverters as MPs for ground-mounted solar facilities. Notice 2025-08 then lists MPCs for each of those MPs. The MPCs for PV Modules, for example, are the cells, frame/backrail, front glass, encapsulant, backsheet/backglass, junction box, edge seals, pottants, bus ribbons, and bypass diodes, as shown in the excerpt below:

[table continues onto next page in Notice 2025-08]

IRS has not identified MPs or MPCs for other types of "qualified facilities" or "energy storage technologies," though it may do so in future guidance. For example, geothermal, nuclear, and storage facilities other than battery energy storage systems cannot rely on the 2023-2025 Safe Harbor Tables when calculating MACRs.

Certain iron and steel structural components of facilities identified in the domestic content guidance are excluded from the MACR calculation under the MACR guidance. For ground-mounted solar facilities, for example, developers may disregard steel PV module racking, steel pile or steel ground screws, and steel or iron reinforcing products in foundation when calculating MACRs.

To assist developers of certain facilities, the MACR guidance establishes the "Identification Safe Harbor," one of three new "interim" safe harbors in the MACR guidance. Developers of "Applicable Projects" listed in the 2023-2025 Safe Harbor Tables—meaning solar, wind, BESS, and certain hydro facilities—may use this safe harbor to identify MPs and MPCs for their MACR calculations.

Developers relying on the Identification Safe Harbor must use the MPs and MPCs listed in the 2023-2025 Safe Harbor Tables as the exclusive and exhaustive list of MPs and MPCs when calculating MACR, even if their facilities contain additional, unlisted MPs or MPCs. Those "unlisted but utilized" MPs or MPCs are disregarded in the MACR calculation. Additionally, if an MP or MPC is listed in the 2023-2025 Safe Harbor Tables but not utilized in the developer's project, it, too, is disregarded in the MACR calculation.

Developers relying on the 80/20 rule for retrofitted facilities may disregard used property in the facility from the MACR calculation. The MACR calculation for 80/20 facilities includes only the "new" property in those facilities—that is the property that must comprise at least 80 percent of the retrofitted facility costs under the 80/20 rule.

B. Step 2: Track MPs and MPCs

Developers must track each MP and MPC in the MACR calculation, as well as their direct costs and whether they were "mined, manufactured, or produced" by a PFE, to a specific qualified facility or energy storage technology.

The guidance sets out rules for "de minimis assignment-based tracking." Developers may assign MPs or MPCs of the same type to qualified facilities or energy storage technologies without individually tracking them to a particular project. However, developers may rely on this rule only if the total direct costs of the assigned MPs or MPCs are less than 10 percent of each facility's total direct costs.

Developers may rely on a separate averaging rule for tracking MPs and MPCs for energy storage technologies below 1MW in capacity.

C. Step 3: Determine Direct Costs

Developers must then sum the direct costs of each MP (including MPCs) incorporated into each qualified facility or energy storage technology.

Direct costs include direct material costs and direct labor costs if the developer has produced the MP. If the developer acquired the MP from a manufacturer or other supplier, however, the direct costs consist of the developer's "acquisition costs." Direct costs, including labor, for incorporating the MP into the facility do not count as direct costs for MPs.

The focus on "acquisition costs" is different from the domestic content guidance, which requires developers to calculate domestic content based on the supplier's costs. By contrast, the OBBBA—as confirmed in the MACR guidance—looks to the developer's costs for MACR purposes. This distinction could simplify compliance for developers, as suppliers are often reluctant to disclose cost information that may be commercially sensitive or confidential.

D. Step 4: Determine PFE Direct Costs

Developers must determine which of their MP and MPC direct costs are attributable to PFEs. This requires identifying all MPs and MPCs that are mined, manufactured, or produced by PFEs, and then totaling the direct costs of all those PFE MPs and MPCs.

Importantly, only the direct costs of PFE-produced MPs or MPCs need be included. If an MP is PFE-produced, but some of its MPCs are not, the PFE direct costs may exclude those non-PFE MPCs. Conversely, if an MP is not PFE-produced, but some of its MPCs are, then the direct costs of those PFE-produced MPCs must be included.

Determining whether an MP or MPC is PFE-produced may be easier said than done. The OBBBA defines PFE as one of three types of entities: Specified Foreign Entities, Foreign-Controlled Entities, and Foreign-Influenced Entities.

Specified Foreign Entities include a range of entities listed under various statutes, including foreign terrorist organizations, OFAC-listed entities and individuals, certain specified Chinese manufacturers, as well as entities or individuals suspected of committing certain national security crimes.

Specified Foreign Entities also include Foreign-Controlled Entities, which in general include certain government entities, individuals, and businesses from China, North Korea, Iran, or Russia as well as entities that are owned (by vote or value) at more than 50 percent by those foreign actors or entities.

Foreign-Influenced Entities are arguably the most difficult to identify. They include entities for which the following applies:

- A Specified Foreign Entity has the direct authority to appoint certain high-level corporate officers of such entity;

- A single Specified Foreign Entity owns at least 25 percent of such entity,

- One or more Specified Foreign Entities own in the aggregate at least 40 percent of such entity; or

- At least 15 percent of the debt of such entity has been issued, in the aggregate, to one or more Specified Foreign Entities.

Foreign-Influenced Entities can also be entities that make payments under contracts or other arrangements giving Specified Foreign Entities certain rights amounting to "effective control" over their ITC or PTC eligible facilities.

The MACR guidance does not elaborate further on PFE status. Questions regarding how the PFE definitions apply will be addressed in future proposed regulations or guidance. Developers must do their diligence when determining whether an MP or MPC has been produced by a PFE, guided only by the PFE definitions in the OBBBA.

E. Step 5: Calculate MACR

After determining a facility's PFE direct costs and total direct costs, the MACR can be calculated as follows:

[Total Direct Costs] - [PFE Direct Costs] / [Total Direct Costs] = MACR

Qualified Interconnection Property

Qualified interconnection property can be included in a qualified facility's ITC basis if it meets certain requirements. The MACR for qualified interconnection property is calculated separately from the MACR for the underlying facility.

Importantly, a qualified facility will not lose ITC eligibility simply because its qualified interconnection property fails to meet the applicable MACR threshold. However, any qualified interconnection property that falls below the threshold will be excluded from the qualified facility's ITC basis.

Calculating the MACR for qualified interconnection property may be difficult since the 2023-2025 Safe Harbors Tables do not identify MPs and MPCs for such property.

Although MACR is calculated separately for qualified interconnection property, interconnection property is not included in the ITC basis at all unless the underlying qualified facility is ITC eligible.

III. Interim Safe Harbors

The MACR guidance establishes three "interim" safe harbors for MACR calculations. Developers may rely on certain combinations of those safe harbors when calculating the MACR.

The Identification Safe Harbor was addressed above. This section addresses the Cost Percentage Safe Harbor and the Certification Safe Harbor.

A. Cost Percentage Safe Harbor

The Cost Percentage Safe Harbor allows developers to determine PFE and non-PFE direct costs using the percentages listed in the 2023-2025 Safe Harbor Tables without relying on actual direct costs. Developers can use Cost Percentage Safe Harbor only if they rely on the Identification Safe Harbor, described above, to identify their facility's MPs and MPCs.

Developers using the Cost Percentage Safe Harbor still follow the five steps described above. However, instead of determining actual MP and MPC direct costs, they can use the "Assigned Cost Percentages" for MPs and MPCs listed in the 2023-2025 Safe Harbor Tables.

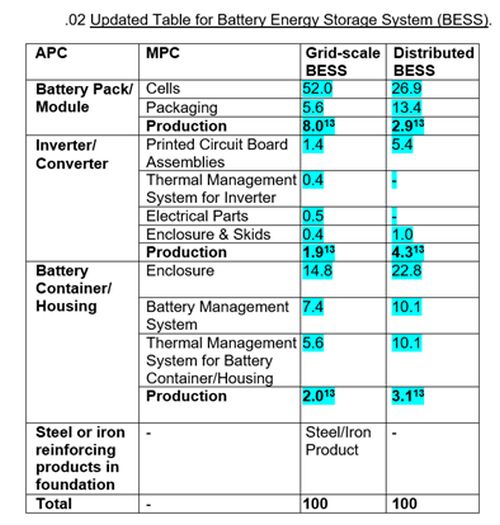

The Assigned Cost Percentages are those that appear in the applicable safe harbor tables in the domestic content guidance. Below is the Notice 2025-08 table for battery energy storage system ("BESS") tables, with the MPC Assigned Cost Percentages highlighted in blue.

The assigned percentage for "Production" above is included as PFE costs if the listed MP is PFE Produced.

Items in the 2023-2025 Safe Harbor Tables identified as "steel or iron" are disregarded and not included in the MACR calculation.

B. Certification Safe Harbor

Under the Certification Safe Harbor, developers may rely on the Identification Safe Harbor to identify MPs and MPCs or make MP or MPC determinations on their own. Then, they may obtain certifications from their direct suppliers regarding either (1) the total direct costs to the taxpayer or the total direct material costs paid or incurred by the taxpayer, as applicable, of an MP or MPC; or (2) that such MP or MPC was not produced by a PFE. Developers may then use those certifications when calculating the MACR.

The MACR guidance's certification requirements mirror those in the OBBBA. Certifications must include the supplier's employer ID number or similar number for foreign suppliers, be signed under penalties of perjury, and be retained by the supplier and taxpayer for not less than six years and be provided to Treasury/IRS on request.

Importantly, the Certification Safe Harbor appears to require certifications only from "direct" suppliers, which could mean MP suppliers, assuming the entity claiming the ITC or PTC is not producing the MPs themselves. This means MP suppliers will need to know enough about their MPC supply chain to certify under penalty of perjury which of their MPCs are produced by PFE and non-PFE entities. Developers cannot rely on certifications that they know or have reason to know are inaccurate and may face penalties for doing so.

C. MACR Guidance Examples

Let's say that a Grid-scale BESS developer's Battery/Pack Module is PFE-produced but contains "Cells" and "Packaging" produced by non-PFEs. Let's also say that the Inverter/Converter and Battery Container/Housing are non-PFE produced.

The MACR guidance allows the developer to use the Identification Safe Harbor to identify MPs and MPCs based on the lists in the 2023-2025 Safe Harbor Tables. Let's say the developer relies on the listed MPs and MPCs in the Notice 2025-08 BESS table copied above.

Under the Cost Percentage Safe Harbor, the developer will include just the number for Battery Pack/Module "Production" as the only PFE direct costs because the Battery Pack/Module was produced by a PFE. The rest of the MPs/MPCs consist of non-PFE direct costs.

The MACR calculation will be as follows: 100 (total PFE and non-PFE direct costs) minus 8 (PFE direct costs) divided by 100 (total PFE and non-PFE direct costs) for a MACR of around 92 percent, well above the 55 percent MACR threshold for energy storage technology for which construction begins for tax purposes in 2026.

Let's say the same BESS developer is building a different facility. It has the same features as the previous one, except that its Battery/Pack Module does not contain the "Packaging" MPC. The Packaging is a "listed but unutilized" MPC that is excluded from the MACR calculation, meaning that it is not included in the total percentage assigned to the facility's MPs and MPCs.

The MP/MPC cost percentage will be 100 minus 5.6 (for the missing Packaging) for a total of 94.4. The MACR will then be determined as follows: 94.4 minus 8 (for "Production" of the PFE Battery Pack/Module because it is PFE-produced, even though its MPCs are not PFE-produced) divided by 94.4 for a MACR of around 91.5 percent, still well above the 55 percent MACR threshold for 2026 energy storage technologies.

The BESS Developer could also rely on the Certification Safe Harbor and obtain certifications from the MP suppliers regarding either (1) the PFE and non-PFE direct costs to the developer; or (2) that certain MPs or MPCs are not produced by a PFE, provided those certifications meet the OBBBA and MACR guidance requirements.

IV. Forthcoming Proposed Regulations

The MACR guidance states that other PFE issues will be addressed in forthcoming proposed regulations. Those include how to apply the "Foreign-Influenced Entity Rules."

Those rules have generated some confusion in the industry, particularly since the OBBBA states that developers can become PFEs, and thus lose ITC and PTC eligibility, if they are a Foreign-Influenced Entity because they have made payments to Specified Foreign Entities under contracts giving those Specified Foreign Entities "effective control" over the developers' ITC/PTC facilities.

The MACR guidance sheds little light on the "effective control" rules, despite ambiguities in the OBBBA regarding how they apply. However, the MACR guidance does appear to confirm one of the more stringent seeming "effective control" factors. Under the OBBBA, "effective control" is determined by reference to thirteen factors. One of them is making a payment to a Specified Foreign Entity for the provision of intellectual property with respect to a qualified facility under a licensing agreement that was entered into or modified on or after July 4, 2025 (the date the OBBBA was enacted).

This factor could sweep broadly: many equipment supply contracts contain boilerplate provisions granting purchasers IP licenses for the equipment they acquire. While suppliers retain no meaningful "control" under such arrangements, the OBBBA's "effective control" factor does not expressly exempt them.

Additionally, forthcoming proposed regulations will address rules to prevent entities from evading, circumventing, or abusing the application of the PFE restrictions.

V. Next Steps – Comments Due by March 30

IRS is soliciting comments on a range of issues addressed in the MACR guidance and beyond. Written comments are due by March 30.

Importantly, IRS is requesting comments on what "substantiation and documentation" should be required to "support compliance with" anti-circumvention requirements around demonstrating that "beginning of construction" has occurred for PFE purposes.

Developers who began construction for tax purposes on their ITC or PTC eligible facilities before January 1, 2026 do not have to comply with the MACR requirements. Many developers advanced their "beginning of construction" timelines to avoid MACR in the absence of guidance.

The request for comment suggests forthcoming proposed regulations could set new documentation or substantiation requirements for "beginning of construction," even though the January 1, 2026 deadline has passed.

The beginning of construction requirements are relevant for other purposes, including determining the applicable MACR threshold. The OBBBA sets MACR threshold percentages that increase year-over-year and are based on the year in which the ITC or PTC eligible facility begins construction.

Typically, in the rulemaking process, another comment period follows the issuance of proposed regulations. Stakeholders may therefore have two opportunities to comment on the guidance—now and again after proposed regulations are issued.

Stakeholders seeking to influence the proposed regulations should take advantage of these comment periods. Under the Administrative Procedure Act, agencies must consider and respond to substantive comments when finalizing rules. If stakeholders fail to raise specific concerns now, Treasury and the IRS may proceed with regulations that prove unworkable or unduly burdensome.

Industry participation will be critical to ensuring a workable PFE framework for the ITC and PTC.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.