- within Energy and Natural Resources topic(s)

- in United States

- with readers working within the Banking & Credit and Media & Information industries

- within Law Department Performance topic(s)

Introduction

2026 is shaping up to be a promising year for infrastructure. Macroeconomic conditions in Europe are stabilizing, with growth proving resilient, easing inflation, and central banks cautiously loosening monetary policy. This backdrop is placing downward pressure on longterm government bond yields and reinforcing the role of infrastructure investments as a source of stable, inflation-linked returns.

Investor appetite for the asset class continues to strengthen. Capital is increasingly rotating away from more volatile assets, particularly in the context of stretched equity valuations following the AI-driven rally. Infrastructure's lower volatility, predictable cash flows, and defensive characteristics are becoming more attractive by comparison.

On the demand side, structural drivers remain intact, led by the energy transition, AI-related investment in data centers and power networks, rising defense expenditure, and the need to reinvest in aging infrastructure. In additional to a substantial pipeline of new projects, schemes delayed in earlier years are being revisited.

Deal volumes have normalized following the post-COVID surge, supported by improving investor sentiment, easing monetary conditions, and interventionist fiscal policies. Capital remains ample, with high liquidity across private funds and banks.

However, deal execution for UK and European infrastructure continues to be constrained by regulatory complexity, planning delays, higher transaction costs, supply-chain disruptions, geopolitical risk, and pressures on cost of capital. Capacity shortages in skilled labor, weak project governance, and delayed investment decisions are further increasing delivery risk.

In this environment, asset quality and portfolio discipline become critical. A portion of the current pipeline reflects lower-quality or overly speculative investments originating during the 2020–2022 deal boom, many of which are now facing valuation pressure or underperformance. As a result, investors, lenders, and corporates are increasingly reassessing portfolios, divesting noncore or high-risk assets, and reallocating capital toward resilient, bankable projects with clearer risk-return profiles.

Capacity shortages in skilled labor, weak project governance, and delayed investment decisions are increasing delivery risk

Deal Activity in European Infrastructure

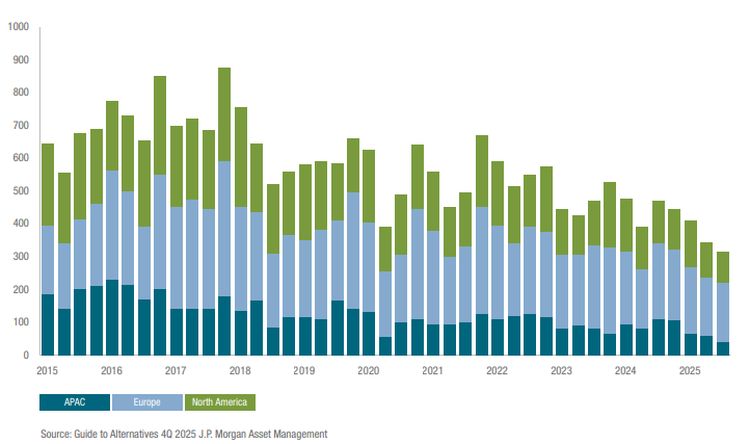

Europe has accounted for nearly half of total global infrastructure deal activity since 2014, consistently outpacing North America in recent years (Figure 1). The region, however, has not been immune to the broader slowdown in global transactions.

Figure 1 – Global infrastructure deals by region (quarterly)

Infrastructure deals in Europe declined to 698 in 2025, down from 764 in 2024 and 856 the year before (Figure 2).1 Although many European renewable independent power producers (IPP) projects came to market, several processes were ultimately withdrawn or scaled back.2 Defying the broader slowdown, 2025 also saw the landmark financing for UK nuclear power station Sizewell C approved, a £38 billion project financed by government and private investors, and the largest deal recorded globally, according to data provider Infralogic.

Europe's electricity consumption is forecast to rise by 1.5% in 2026

Since the pandemic, when fundraising peaked, the number and pace of projects have been affected by a new economic reality of higher interest rates and a rising cost of capital, geopolitical instability, stringent regulatory requirements, and outdated planning laws.

Looking ahead, we believe 2026 could mark a turning point. There is a healthy supply of upcoming projects in the market and a clear mandate for investment.

The energy sector alone exemplifies this momentum. With Europe's electricity consumption forecast to rise by 1.5% in 2026,4 grid constraints will need to be addressed. Across France, Spain, Italy, the UK, and the Netherlands, an estimated 800GW of renewable capacity is currently awaiting grid connection.5

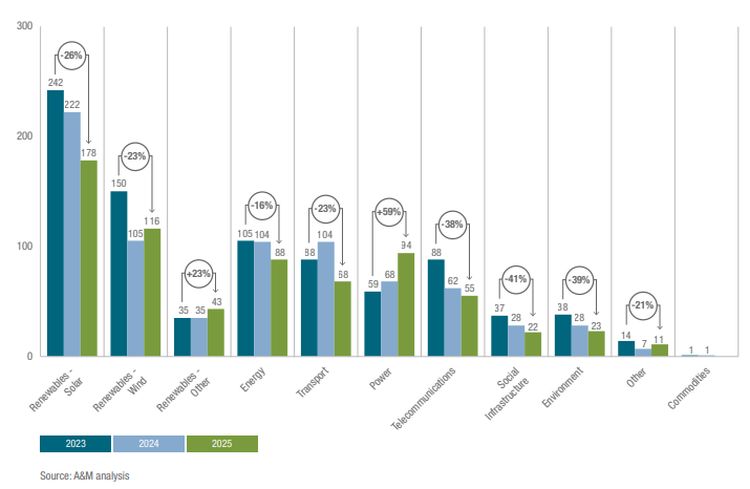

Figure 2 – Infrastructure deals by sector between 2023 and 20253

Recent updates from grid operators and policy reforms illustrate that demand

UK:

The National Energy System Operator (NESO) has introduced a new delivery pipeline, focusing on "ready-to-build" projects that could unlock 283GW of generation/storage capacity, along with 99GW of transmission demand.6 The UK is also expected to launch its competitively appointed transmission owner (CATO) regime, aimed at accelerating and reducing the cost of onshore grid infrastructure through competitive tendering.7 In parallel, the offshore transmission owner (OFTO) regime is evolving following a consultation last year, with Ofgem setting out changes to the existing tender process and addressing issues related to high voltage direct current (HVDC) availability.8

- OFTO reforms come just as the UK secures a record 8.4GW supply of offshore wind projects in an auction round in January 2026.9

Germany:

The utility association BDEW reports grid connection requests for battery storages with capacity of over 720GW are currently pending. Only 78GW has been approved to date, it says.10

Italy:

Requests from data centers seeking grid connection exceeded 300 projects, totaling more than 50GW by June 2025, compared to around 30GW in 2024, according to the national transmission system operator.11

Spain:

The saturation of connection nodes for generation and demand capacity is affecting more than 80% of substations according to a recent analysis.12 As a consequence, The Spanish Government has announced a significant increase in the official investment limit for the national electricity grid. The new plan considers an unprecedented €13.6 billion investment in the transmission and distribution network through 2030, a 62% increase over previous plan.

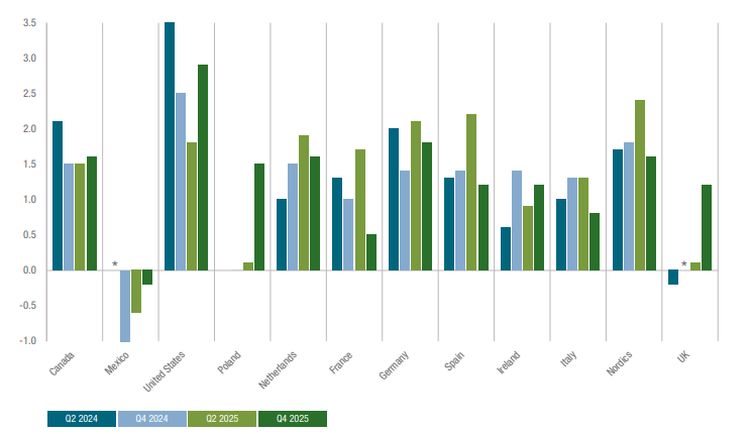

Figure 3 – Regions viewed as most attractive for future infrastructure investment

Legend: -5: extremely unfavorable, 0: neutral, 5: extremely favorable. * Mexico had a net sentiment of 0 based on survey responses for Q2 2024. The UK had a net sentiment of 0 based on survey responses for Q4 2024 Source: A&M, GIIA Infrastructure Pulse survey Q4 2025

Total investments in grid to achieve net zero targets are estimated at between €81 billion and €124 billion annually,13 whilst the broader European infrastructure market is projected to require $14.8 trillion between 2016 to 2040 (keeping 2016 prices constant), or 16% of global infrastructure investment needs.14

Footnotes

1. Alvarez & Marsal analysis. Observations and conclusions in this advisory reflect our professional expertise and ongoing study of the industry; analysis of reputable third party publications and data; insights from client engagements; market intelligence and benchmarking; and synthesis of regulatory, academic, and investor perspectives.

2 Stefano Berra et al., "Year ahead: EMEA power investment surge to continue," Ion Analytics, January 17, 2026.

3 Alvarez & Marsal analysis.

4. International Energy Agency, "Electricity Mid-Year Update 2025 Demand: Global electricity use to grow strongly in 2025 and 2026," July 30, 2025.

5. Aurora Energy Research, "The State of European Power Grids: A Meta-Analysis," December 2025.

6 "NESO implements electricity grid connection reforms to unlock investment in Great Britain," National Energy System Operator, December 8, 2025.

7. Ofgem, UK Government, "Onshore early competition in electricity transmission – Stakeholder update," December 2025.

8. Ofgem, UK Government, "Further evolution of the OFTO Regime," December 8, 2025.

9. UK Government, "Record breaking auction for offshore wind secured to take back control of Britain's energy," January 14, 2026.

10. Edgar Meza, "Flood of grid battery requests requires new connection rules, says German energy industry," Clean Energy Wire, November 27, 2025.

11. Terna Lightbox, "Data centres and the future: the energy challenge facing Italy," August 8, 2025.

12. Foro Industria y Energia, "La red eléctrica española pierde 2,8 GW en dos meses y alcanza un 85,7% de saturación - FIE" January 16, 2026.

13. urora Energy Research, "The State of European Power Grids: A Meta-Analysis."

Originally published 9 February 2026

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.