- within Strategy topic(s)

- in United States

- within Strategy topic(s)

- in United States

- with readers working within the Aerospace & Defence industries

- within Strategy, Government, Public Sector and Energy and Natural Resources topic(s)

FOREWORD

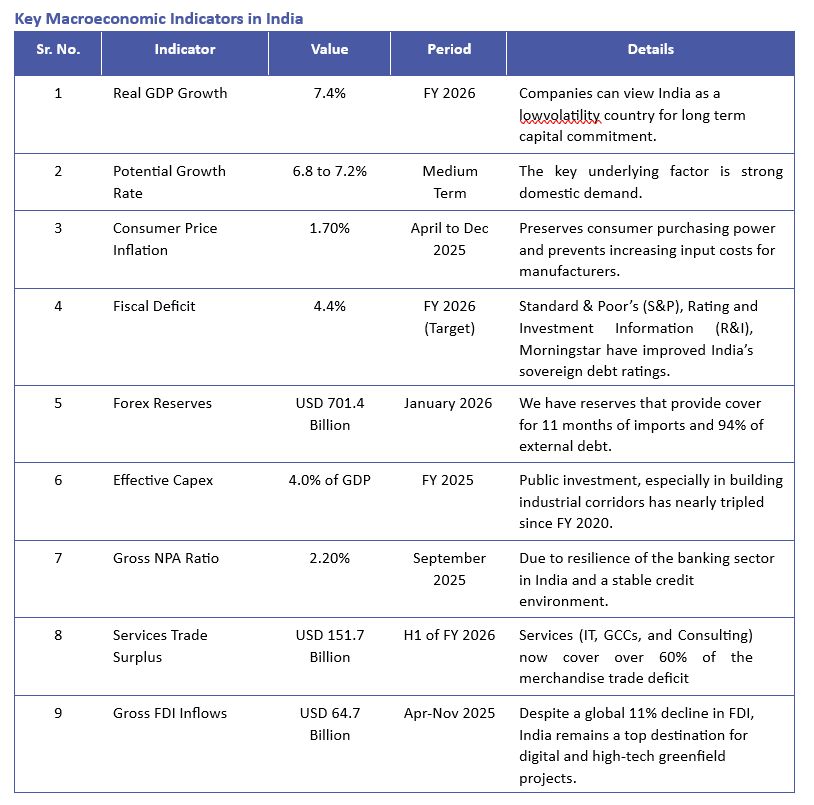

The Indian Economic Survey presents a detailed analysis of our economy's performance during FY 2025–26, reaffirming that India stands for stability in a world that is increasingly complex, volatile, and uncertain. The Survey projects a growth trajectory of 6.8% to 7.2% for FY 2027, anchored in a strategic shift from traditional 'Import Substitution' to 'Strategic Indispensability'.

A prominent theme in the Survey is the government's continued progress toward a data-driven taxation mechanism. India has advanced from an enforcement-led model to one centred on data-driven compliance, supported by NUDGE - Non-intrusive Usage of Data to Guide and Enable - which aims to influence taxpayer behaviour rather than rely on enforcement or litigation. This transition has led to a widening of the tax base, with income tax returns filed rising to 9.2 crore in FY 2025.

The Survey also highlights the continued success of the Goods and Services Tax ('GST'). Under GST 2.0, gross GST collections reached INR 17.4 lakh crore in the first nine months of FY 2025 - 26 alone, reflecting 6.7% growth, while the registered taxpayer base expanded to over 1.5 crore.

Another important insight is the recognition of a long-standing challenge for multinational companies - the disconnect between transfer pricing and customs valuation. The Survey calls for greater coordination between these two regimes to reduce transaction costs and enhance certainty for investors.

In terms of financing, the Survey notes a shift in credit generation patterns. While bank credit grew moderately, financing from non-bank sources increased notably by 29.3% during April 2025 to November 2025. Gujarat International Finance Tec-City (GIFT IFSC) has strengthened its position as a global financial hub, with 38 IFSC Banking Units and cumulative transactions exceeding USD 142.98 billion.

India's rising prominence in global services is also underscored. Services exports touched an all-time high of USD 387.5 billion in FY 2025, generating a surplus of USD 188.8 billion. This performance is significantly driven by the growth of Global Capability Centres (GCCs), whose estimated revenue stands at USD 64.6 billion with a CAGR of nearly 10%.

The maturation of India's Digital Public Infrastructure emerges as another defining feature. Tele-density has reached 86.76%, and 5G services are now available in 99.9% of districts across the country. Internet subscriptions have increased from 25.2 crore in 2014 to 101.78 crore by September 2025, while average monthly data consumption per wireless subscriber has surged from 61.66 MB in 2014 to 25.24 GB in 2025. The enormity and accessibility of this digital ecosystem create a clear competitive advantage for businesses operating in India. The Survey also acknowledges the external challenges faced during FY 2025–26, including significant tariff shocks, particularly those imposed by the United States on Indian goods in April 2025. Nevertheless, India's continued efforts to negotiate trade agreements with the UK, Oman, the European Union, and New Zealand have helped diversify trade partnerships and bolster the domestic economy.

Quoting that the Indian economy is "running a marathon and sprinting simultaneously," the Economic Survey 2025–26 signals a decisive move toward a trust-based compliance architecture, a shift that is vital for facilitating mergers and acquisitions as well as foreign investment. At Aurtus, we remain committed to supporting organisations as they navigate India's complex yet robust growth journey.

Global economic uncertainty remains high compared to historical trends. This is due to fragmentation in geopolitical relationships and lower visibility on policy continuity. - Vishal Gada Founder & CEO

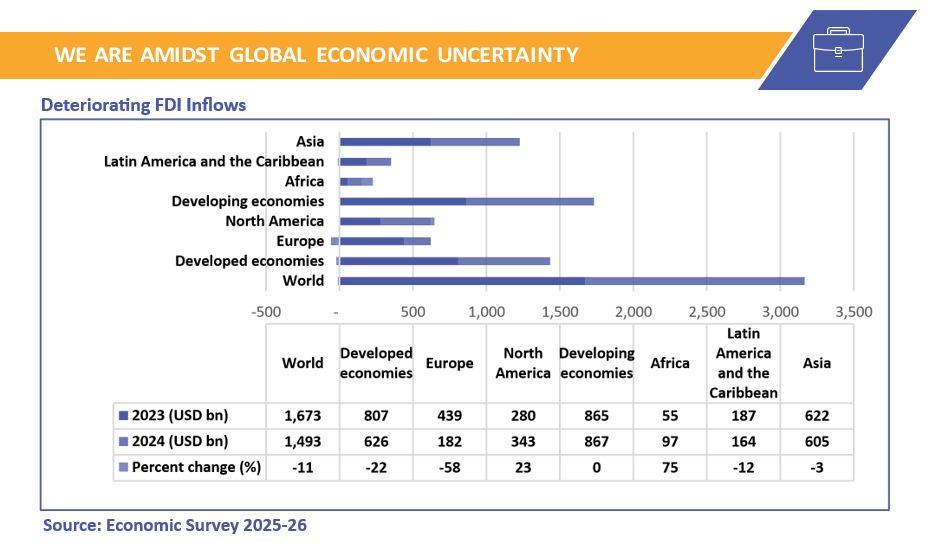

- Policy uncertainty is high and global FDI fell ~11% in 2024, with a weak outlook. See the graph below.

Economic Survey 2026

- The Survey predicted that there is a 10-20% chance of a systemic shock - that may cause a repeat of the 2008 financial crisis in 2026. Financial and technological geopolitical stresses will promote one another.

- Demand from some export markets can be patchy; clients need diversified markets and products to avoid single-market shocks.

- Hence, building 'Plan B' liquidity with internal buffers is crucial. Currency moves can be sudden when flows turn; hedging policies need to be clear and rule-based.

- Pushing market diversificationg. with ASEAN, Middle East, EU FTA channels. and shift mix to services where India is resilient could be beneficial.

India has decisively transitioned from post-pandemic recovery to a phase of 'Pushing the growth frontier'. This is on account of some of the parameters below:

The Survey highlights that while India's size is significant, in terms of demographics, the Lowy Institute's Power Gap Index (where India scores -4.0) indicates that India is still operating below its full strategic potential.

- Agriculture sector's significance for Inclusive Growth: Agriculture (estimated 1% growth) continues to show a stark divide: volatile crop growth versus the steady 5-6% expansion in Allied Sectors (livestock and fisheries). For FMCG and retail clients, the allied sectors provide rural demand stability, as they are less susceptible to the weather.

- Industry sector's need to become more competitive: The industrial sector is projected to grow at 2%. The manufacturing's share in real terms is stable at 17-18%. However, there are persistent margin squeezes for manufacturers, where intermediate consumption costs rise faster than the final pricing. For example, steel, coal and cement are key inputs in manufacturing. However, the Survey highlights that 'negotiated shelter' i.e. protectionism in these upstream sectors acts as a tax on downstream export competitiveness.

- Service Sector Continues to lead expansion: The Services sector remains the primary engine, estimated at 1% growth. The proliferation of Global Capability Centres (GCCs) has transformed the sector from cost-arbitrage to high-value innovation hubs.

- Currently, India's services sector contributes more than half of the Gross Value Added and serves as a major driver of exports and employment in the country. The sector has recorded average annual growth of around 7% - 8% year after year.

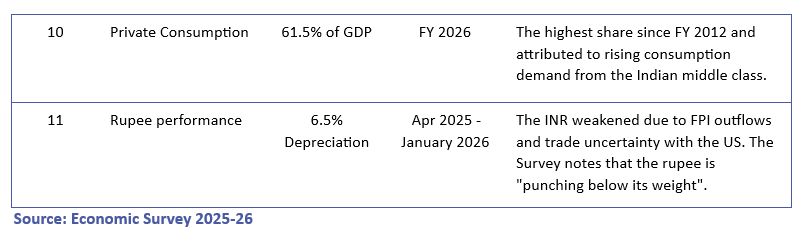

- In FY 2025, the services trade surplus increased to USD 188.8 billion, reaching the highest level ever recorded.

- Twin Engines of Rural and Urban Demand: Along with the services sector, domestic demand is a backbone, propelling the Indian Economy forward.

To view the full article please click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.