- within Technology topic(s)

- in Canada

- with readers working within the Banking & Credit, Business & Consumer Services and Property industries

- within Technology topic(s)

- in Canada

- with readers working within the Banking & Credit, Business & Consumer Services and Property industries

- within Technology, Insolvency/Bankruptcy/Re-Structuring and Criminal Law topic(s)

Introduction

On 2 February 2025, the Central Bank of Nigeria (CBN), published its Fintech Strategy Report, and even with frequent regulatory actions, this Report marks the first time the CBN has formally undertaken a wholesale regulatory review of the sector since it issued the Payment Systems Vision 2025 on 24 November 2022. The Report signals a policy shift towards more coordinated regulation, enhanced supervisory capacity, streamlined licensing processes and institutionalized engagement with the fintech ecosystem, all aimed at supporting responsible innovation while strengthening systemic stability and market integrity.

CBN's Policy Direction

Shaping the CBN's policy and regulatory direction for the fintech sector are three overarching objectives; innovation-friendly regulation, driving financial inclusion through digital finance, and deepening regional integration through regulatory harmonization. Based on this, the CBN highlighted a range of potential solution pathways to address the key challenges identified across the ecosystem. These are:

- Enhancing Regulatory Engagement and Responsiveness

- Building Foundational Infrastructure and Reducing Systemic Friction.

- Supporting Capital Access and Sustainable Business Models

- Advancing Interoperability and Inclusive Credit Infrastructure

- Positioning Nigeria as a Regional Fintech Leader

These solution pathways identified by the CBN essentially form the basis for its proposed sector reforms. These reforms are much needed because notwithstanding sustained growth in Nigeria's fintech ecosystem, fintech operators continue to face practical regulatory challenges, including ambiguity in compliance requirements, prolonged approval timelines, inconsistent application of rules and limited coordination among regulators. Structural constraints around digital identity, datasharing frameworks and payments system resilience also persist, alongside growing industry interest in regulatory passporting and clearer regulatory approaches to emerging areas such as artificial intelligence and digital assets.

These reforms are intended to address these persistent challenges and strengthen every segment of the sector.

CBN's Priority Reforms — What Will Change and How They'll Be Delivered

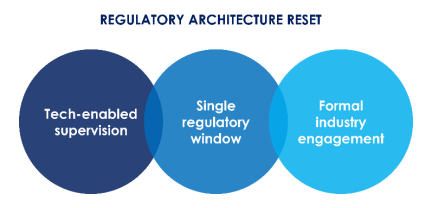

- Launch Standing Fintech Engagement Forum: The CBN intends to launch a permanent, structured forum for two way engagement, early feedback on policies, and co creation of pilots. This will be Implemented through a Standing Advisory Council and a CBN hosted Regulatory Engagement Platform running quarterly thematic sessions, with coordination and follow through by a Fintech Reform Delivery Secretariat.

- Single Regulatory Window for licensing and supervision: A unified interface to simplify multi agency onboarding, licensing and reporting, phased in via a shared digital portal, the Smart Licensing & Supervisory Gateway (SLSG). The SLSG will embed Supervisory Technology (SupTech) capabilities, standardised digital forms, workflow tracking, escalation protocols, user analytics and real time dashboards to support data driven, proactive oversight across agencies, overseen by the Reform Delivery Secretariat.

- Expanded Regulatory Sandbox ("Sandbox 2.0"): Wider participation and clearer pathways from testing to authorisation in areas such as AI, embedded finance, and cross border payments. This will be run as a live market pilots where appropriate, with codification of learnings into proportionate rules and playbooks; coordination across existing sandboxes to avoid duplication.

- Industry Government Digital Trust Charter: The CBN proposes a voluntary, publicly endorsed Fintech Trust & Safety Charter (FTSC) setting minimum expectations for data protection, AI, cybersecurity, fair competition and consumer redress to be operated as a reputational signal (public registry), potentially enabling fast-track access to pilots for participants. The FTSC is designed to complement formal regulation by encouraging industry-led alignment on consumer-protection and governance standards.

- Expand digital banking licenses to support inclusive financial services: Assess a consolidated digital-bank licence (rather than stretching Payment Service Banks (PSBs) permissions) to enable new entrants to safely delivered credit and savings services subject to appropriate safeguards. This will be achieved through structured consultation and prudential standards development, with possible convergence of overlapping licences and strong coordination with other sector regulators to preserve supervisory clarity. To depen deepen financial inclusion, the CBN is also considering revising PSB lending rules and improving low cost access channels such as USSD, enabling more effective reach into underserved and rural communities. In parallel, to support credit expansion to MSMEs, youth, and women led enterprises, the CBN proposes the Fintech Credit Guarantee Window (FCGW), a blended finance mechanism administered with development finance partners to de risk fintech lending portfolios and incentivise responsible expansion into priority segments.

- Accelerated Open Banking / Open Finance implementation: Full operationalisation of technical standards, governance and consumer safeguards to enable data portability and embedded finance. This will be through the use of Open Finance Lab (OFL) for supervised pilots; publish an implementation roadmap, dispute resolution mechanisms and consumer awareness plans.

- Cheaper, more reliable digital identity access: Reduce barriers to API based NIN/BVN verification and strengthen BVN–NIN interoperability by enforce minimum service levels, build redundancy/contingency arrangements, and improve commercial terms for regulated users to support inclusive onboarding and KYC.

- Strengthening data sharing and credit infrastructure: The CBN intends to improve integrity and interoperability Nigeria's data sharing and credit reporting ecosystem, including reforms to pricing, reciprocal data contribution, and expansion of the Global Standing Instructions framework. It also plans to deploy shared compliance utilities, including a Compliance as a Service (CaaS) model for regulated fintechs, to reduce duplicative compliance burdens and improve ecosystem wide supervisory visibility. These measures will be reinforced by the Shared Fraud Defence Framework (SFDF), which introduces near real time fraud intelligence sharing, unified reporting, a central repository of fraudulent accounts, and enhancements to NIBSS HAWK, BVN Watchlisting, and the Persons of Interest Portal, collectively forming the backbone of Nigeria's fraud defence and cybersecurity architecture for digital finance. In parallel, the CBN is considering a hybrid payments infrastructure model that keeps core clearing and settlement centrally while allowing certified private operators to build service and innovation layers through open APIs, thereby strengthening system resilience and reducing single points of failure.

- Regional regulatory harmonisation and passporting: Pilot mutual recognition of licences and supervisory expectations with priority markets to reduce friction for cross-border scale. This will begin with bilateral pilots (e.g., Ghana, Kenya, Senegal), then deepen alignment through ECOWAS/AU fora on KYC, consumer protection and payments interoperability.

- Position Nigeria as a hub for Responsible AI in finance: Adopt a "test-then-codify" model that converts sandbox learnings into tiered, outcome-based obligations for AI use in fraud, credit, onboarding and conduct-risk management. By establishing a Responsible-AI workstream (with regulators, industry and academia), publish guidance on explainability/fairness, and leverage OFL/Sandbox 2.0 for supervised trials.

Phased Implementation

As set out in the Report, the proposed policy reforms are slated to be implemented in phases as follows:

Phase 1: Immediate Priorities (0–3 months)

- Establish Fintech Engagement Forum under CBN leadership.

- Issue implementation roadmap for Open Banking and initiate industry sensitisation.

- Begin technical scoping for Single Regulatory Window and Smart Licensing Gateway.

- Coordinate cross-agency review of PSB lending restrictions and digital ID access - with a shift in emphasis towards Digital Bank authorisation frameworks over PSB expansion.

Phase 2: Near-Term Reforms (3–9 months)

- Launch pilot cohort for Regulatory Sandbox 2.0 including AI and RegTech use cases.

- Operationalise Fintech Credit Guarantee Window in collaboration with DFIs.

- Issue guidance on data portability and consumer protection under Open Finance.

- Initiate bilateral consultations on regulatory passporting (Ghana, Kenya, Senegal).

Phase 3: Institutionalisation and Scale (9–18 months)

- Formalise Fintech Advisory Council to oversee implementation and course correction.

- Launch Regulatory Engagement Platform and public calendar of consultations.

- Embed supervisory analytics and early-warning tools through SupTech pilots.

- Participate in ECOWAS and AU regulatory alignment fora to shape continental norms.

Sector Impact

The Nigerian fintech ecosystem is at a critical inflection point, where successful reforms can propel the sector into a period of sustained growth and impact in Nigeria and across Africa. With the CBN's Fintech Strategy indicating a shift towards more structured, technology-enabled and collaborative regulation, these reforms are poised to do just that, but successful delivery of the proposed reforms will depend on coordinated engagement across regulators, strengthened supervisory capacity, industry-led standards on interoperability and consumer protection, and effective alignment with development partners. The emerging delivery architecture, anchored on institutional mechanisms, shared regulatory platforms and digital infrastructure, reflects a clear intent to move from policy design to implementation.

Conclusion

For fintech operators, the immediate priority is to begin aligning internal compliance frameworks with anticipated regulatory tools, particularly around licensing, open finance, digital identity, supervisory reporting and cross-border operations. If executed effectively, these reforms position Nigeria to consolidate its role as a regional fintech pace-setter, balancing innovation, inclusion and systemic integrity.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.