- within Energy and Natural Resources topic(s)

- in Canada

- within Energy and Natural Resources topic(s)

- within Wealth Management, Employment and HR and Technology topic(s)

- with Senior Company Executives, HR and Finance and Tax Executives

- with readers working within the Law Firm industries

As part of its commitment to decarbonising aviation and positioning the UK as a clean‑energy leader, the UK Department for Transport (DfT) has launched a consultation on the implementation of the revenue certainty mechanism (RCM) proposed under the Sustainable Aviation Fuel (SAF) Bill. A copy of the consultation paper can be accessed here and interested parties are encouraged to submit their responses before the consultation closes on 3 April 2026.

The RCM is designed to strengthen investor confidence and accelerate UK SAF production by providing long‑term revenue certainty for producers through a guaranteed strike‑price model. The consultation seeks feedback on two core elements of the RCM: (i) an indicative heads of terms that sets out the proposed commercial terms of the RCM; and (ii) the DfT's proposed approach to allocating the initial RCM contracts.

The government anticipates that the entire legislative package required for the RCM will be implemented by the end of 2026. The consultation provides another step towards completing the legal framework for enabling SAF projects in the UK. Set out below is our commentary on:

- the key commercial terms set out in the indicative heads of terms (see here);

- the proposed allocation process for the initial RCM contracts (see here); and

- the likely market impact if the proposals in the consultation are implemented by government (see here).

1. RCM key commercial terms

As part of the consultation on the RCM the DfT has published an indicative heads of terms that sets out the key commercial terms that are likely to feature in the first RCM contracts, with the consultation paper setting out the underlying rationale for the proposed terms. The indicative heads of terms can be accessed here. We comment below on the following key provisions:

- term and commencement (see here);

- pre-operational stage conditions and requirements (see here);

- termination (see here);

- payment mechanics (see here); and

- change in law (see here).

a. Term and commencement

A fixed 15-year contract term is proposed for all RCM contracts. The DfT considers this timeframe sufficient to provide revenue certainty for SAF projects and the term is consistent with other low-carbon business models that also rely on similar RCM contracts.

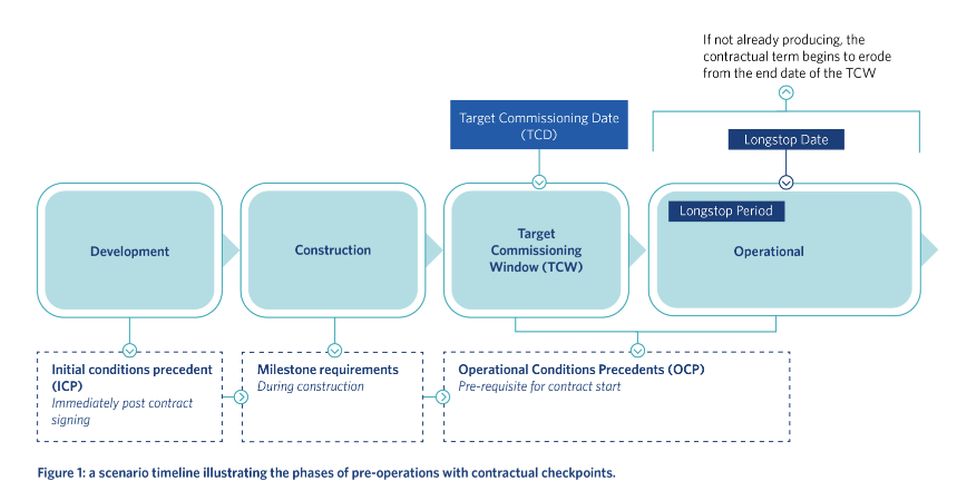

The contract term is proposed to begin on the earlier of the actual commissioning date or the final day of the Target Commissioning Window (but cannot start prior to the first day of the Target Commissioning Window). The SAF producer and the RCM counterparty will agree on when the Target Commissioning Window starts, but its duration is fixed at 12 months.

b. Pre-operational stage conditions and requirements

The DfT intends to structure the initial conditions precedent for the RCM contract to ensure that the SAF producer meets certain requirements, such as grid connection or land planning approval, immediately following the date of the agreement.

In addition to the initial conditions precedent, the SAF producer will be required to demonstrate that it is committed to delivering the project by having to comply with certain milestone requirements. The SAF producer will be required to provide evidence of either: (i) actual expenditure representing a specified proportion of total commissioning costs; or (ii) completion of defined project commitments.

Certain operational conditions precedent (OCPs) will also need to be satisfied before the contract becomes operational and payments commence. The OCPs will require the SAF producer to evidence that the SAF facility has been commissioned to the agreed installed capacity and meets all sustainability and metering requirements. If these are not satisfied by the end of the 12‑month Target Commissioning Window, the contract term will still commence but payments will not flow until compliance is achieved. Producers are granted limited relief (e.g. time extensions) for delays beyond their control, such as utility connection issues, consistent with contracts in DESNZ business models.

The figure below is based on the diagram in the consultation and illustrates the proposed timeline for the pre-operational stage requirements.

c. Termination

To protect the value of the scheme and prevent funding becoming indefinitely tied to projects with no realistic prospects of reaching expected levels of production, it is proposed that the counterparty has broad termination rights.

The counterparty would be entitled to terminate an RCM contract before the start date without liability or compensation if:

- a SAF producer default event occurs and is continuing;

- the initial conditions precedent are not met within the specified timeframe;

- any directors' certificate provided is materially false or misleading; or

- the operational conditions precedents are not satisfied by the longstop date (being 12 months after the end of the Target Commissioning Window).

The indicative heads of terms sets out a list of SAF producer breaches allowing the counterparty to terminate the agreement after the start date. These include insolvency, unremedied non-payment, fraud, credit support default, and violations of key obligations on SAF facility ownership, metering, monitoring, reporting, and SAF technology. It also covers loss of access to essential storage and transport infrastructure, failure to comply with audit rights, and breaches related to affiliate offtakers.

The list of producer events of default follows the approach in similar contracts, including the Low Carbon Hydrogen Agreement (LCHA). However, the DfT has indicated that it is considering whether there are other SAF-specific termination events that should be included in the RCM contract.

Respondents to the consultation are requested to comment on the indicative termination provisions and the principles which should govern calculation of termination amounts payable by the SAF producer to the counterparty.

d. Payment mechanics

- Difference Amount: The difference amount will be the amount (£ per litre) paid by or to the SAF producer to ensure the SAF producer earns the guaranteed strike price (Strike Price) for their SAF. The reference price is the benchmark price against which the Strike Price is compared to determine the size and direction of the difference amount (Reference Price). It is intended to reflect the market price for non‑hydroprocessed esters and fatty acids (non-HEFA) SAF. If the Reference Price falls below the Strike Price, the counterparty pays the difference amount to the SAF producer and if it exceeds the Strike Price, the SAF producer pays the difference amount to the counterparty.

- Reference Price and Floor Price: Because there

is currently no reliable market price for non-HEFA SAF, the

indicative heads of terms propose three options for establishing a

proxy Reference Price. These are:

- the higher of the achieved sales price and a Jet A‑1 fuel Price Floor;

- the higher of the achieved sales price and a HEFA SAF fuel Price Floor; and

- an indicative market price (being the Jet A-1 fuel price plus

UK SAF Mandate certificate price).

The floor price is intended to prevent sales below a defined threshold and limits counterparty exposure. The Jet Fuel Price is considered to be a feasible option for a floor price as SAF is fungible with conventional aviation fuel.

- Transition to Market-Based Reference Price: The

DfT aims to adopt a market‑based Reference Price as soon as

practicable to minimise market distortions and improve value for

money. Once a market price for non‑HEFA SAF is established

and a reliable index is published, the index will serve as the

Reference Price in subsequent RCM contracts. The DfT is also

assessing whether transitioning from a proxy to a

market‑based Reference Price would be feasible during the

first RCM contracts.

- Price Discovery Mechanism: To counteract

incentives for SAF producers to sell below market value, several

mechanisms are proposed, including revenue bonuses, limiting

supported volumes, mandating transparent sales channels, or

requiring arm's‑length pricing. These aim to accelerate

formation of a real market price and point to an inherent challenge

in the RCM / CfD model which is that if revenue payable to the SAF

producers is capped, then without other measures, there is a risk

of over-subsidy occurring if there is no incentive for SAF

producers to sell above the floor price.

- Strike Price: The Strike Price (£ per

litre) will be stipulated in the RCM contract. Certain costs of a

SAF project will be excluded from the calculation of the Strike

Price, which may include the costs of storing and transporting SAF

and producing co-products.

It is proposed that the full Strike Price will be indexed to CPI to protect SAF producers against inflationary erosion of margins. CPI‑based indexation mirrors other low‑carbon business models and is intended to preserve long‑term revenue stability. The DfT is also considering adjusting the Strike Price based on the greenhouse gas savings of the SAF, to ensure the policy behind the SAF Mandate is not undermined.

e. Change in law

The indicative heads of terms takes a similar approach to change in law provisions seen in other low carbon business models. It provides for a degree of cost and revenue protection for SAF producers in the event of various qualifying change in law scenarios, with compensation following the "no better, no worse" approach of the LCHA.

Change in law protection is important in an area such as this where future changes in regulation (such as in relation to the SAF Mandate or Renewable Transport Fuel Obligation) may occur. In respect of any changes to the SAF Mandate criteria, the government is currently considering two alternatives: (i) either grandfathering the current SAF Mandate requirements; or (ii) applying the same change in law regime as above.

2. Contract allocation

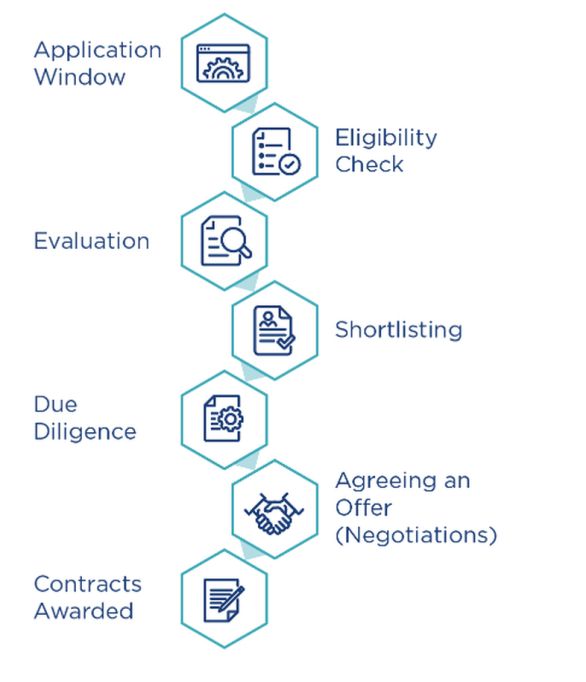

The consultation paper also invites engagement on the DfT's minded to positions for the design of the initial allocation round of RCM contracts (AR1), determining how RCM support will be distributed across producers over time.

a. Proposed allocation model

The DfT proposes a tendered bid process with bilateral negotiations for AR1, rejecting auctions and standardised pricing due to limited bidder pools and high cost‑uncertainty.

The government considers the tendered bid model to best support complex first of a kind projects while preserving competitive tension through structured evaluation and due diligence.

The proposed tendered bid process structure for AR1 is set out below (based on the flowchart in the consultation). Stakeholders are invited to share their feedback on the proposed allocation approach and proposed bid process structure for AR1.

b. Eligibility criteria

As part of the consultation the DfT is inviting responses to its proposed approach of assessing eligibility on a pass/fail basis and the relevant eligibility criteria which requires:

- SAF production plants to be based in the UK;

- Delivery within a set delivery year;

- Compliance of technology used to produce SAF with relevant international standards for aviation use;

- SAF production facilities to be new-build (this includes new capacity developed at existing sites where at least 20 ktpa of additional SAF production is constructed);

- Compliance of SAF produced with all SAF Mandate requirements;

- Evidence of written engagement with feedstock providers to supply feedstock over the project lifetime;

- Evidence of a grid connection offer / that the project will have access to a power supply by the Target Commissioning Date;

- Completed Front-End Loading (FEL) – one feasibility study; and

- Evidence of finance.

c. Evaluation criteria

Subject to stakeholder comments, the DfT proposes scoring projects on deliverability (50%), normalised strike price (40%), and economic benefits (10%). This framework emphasises timely deployment, cost‑effective carbon savings, and wider UK economic contribution while ensuring competitive differentiation among bidders.

d. Final stages

The government will shortlist deliverable, cost‑effective SAF projects based on evaluation scores and portfolio considerations, with the option to limit the number if oversubscribed. Shortlisted applicants then undergo due diligence, negotiate RCM support terms, and submit a best and final offer. The successful projects will then be awarded RCM contracts on the relevant agreed terms.

3. Market impact

The RCM consultation provides another step towards the ultimate end of creating the legal framework for enabling SAF projects and a viable SAF market in the UK.

The consultation and the indicative heads of terms are welcomed for setting out the DfT's current approach to the key areas of risk allocation under the RCM and in many respects this aligns with the approach taken in the "tried and tested" low carbon electricity CfD (banked many times in a renewables context) and other revenue support contracts based on the CfD model such as the LCHA.

While a challenge for low carbon hydrogen has been the lack of a ready downstream market, the coupling of the RCM with the SAF Mandate should help mitigate concerns regarding lack of aviation sector demand for SAF and create the commercial driver for offtakers to enter into long-term purchase contracts (assuming the buy-out price under the SAF Mandate remains well above non-HEFA SAF offtake prices).

There are key areas at the very heart of the RCM where the DfT is still explicitly considering its options, such as the choice of benchmark for the Reference Price mechanism, the price discovery mechanism and the interaction with the (potentially changing) requirements of the SAF Mandate. The industry will be watching closely where the DfT comes down on these points and what types of risk will need to be absorbed by project developers and which cannot be passed on to offtakers through the offtake contracts.

Given the RCM only applies in respect of SAF that is produced and sold in the UK, we expect that focal points of consideration for stakeholders will be on managing the technology risk of first of a kind SAF projects (at least on genuine commercial scale) and the interface risks with other key infrastructure required for SAF projects – many of these risks will remain with the project developers notwithstanding the RCM.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]